3 Dividend Growth Stocks That Can Pay Your Rent in 2026

Here's the positions I am accumulating now and why they will continue to grow my dividend income.

For most people, rent is the single biggest bill they pay each month. Imagine if you didn’t need your paycheck to cover it. Imagine if instead, a few dividend checks rolled in to take care of that expense automatically. Dividend investing turns your portfolio into a source of real-world income that covers real-world needs.

I often frame my investing goals this way: Which expenses can I make disappear with dividends? For some, it is groceries. For others, it is a car payment. But rent is the big one. In 2025, it is very possible to build a portfolio that throws off enough income to cover $1,500, $2,000, or even $3,000 a month.

The key is selecting dividend stocks that do not just pay well today, but are positioned to keep paying tomorrow. That is where the combination of stability, growth, and resilience comes in.

I’ve been able to accumulate $1M in assets at 30 years old. Most of this growth has come from buying high-quality assets that appreciate in value. Unlike traditional advice, I didn’t choose to focus primarily on ETFs. Instead, I chose dividend stocks that continue to compound my passive income over time.

Here’s an example: My portfolio is outpacing the US stock market over the last twelve months.

My Portfolio: 32.31%

US Stocks: 19.38%

Even with this outperformance, I still manage to put an emphasis on dividend income within my portfolio. This is passive income that I do not need to actively work for. This is income that pays me regardless of which direction the market is going or what’s happening in the economy.

👉Get a discounted rate forever. Deal ends September 30th.

👉Buy the latest high-yield option ETF Guide and get 3 months of paid access. If you’re serious about building steady, predictable cash flow from dividends, this guide is the best place to start.

👉Book a portfolio review and earn a lifetime paid membership.

Pick #1 - Kroger KR 0.00%↑

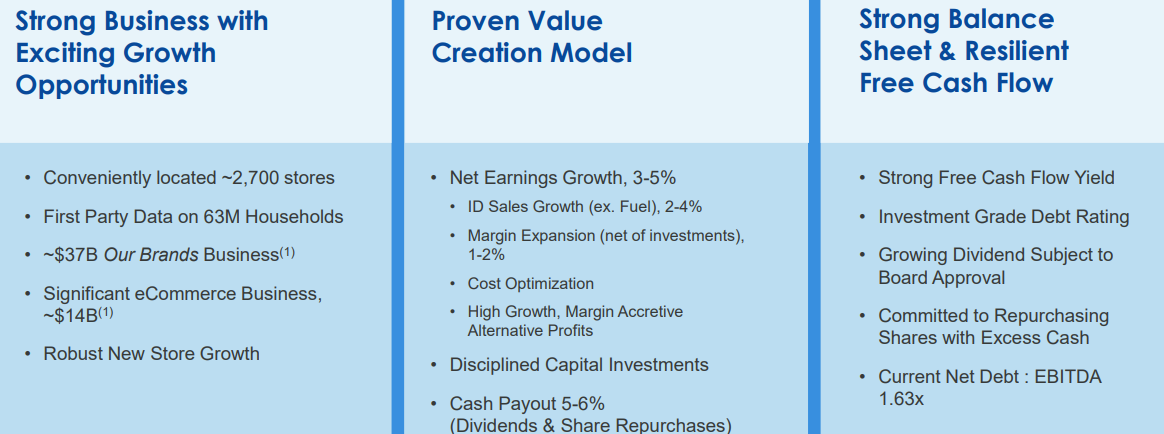

Depending on where you’re located in the US, there’s a chance you’ve never seen a Kroger. Actually, there’s a chance you’ve probably never even heard of Kroger. When it comes to covering rent with dividends, the first quality I look for is stability. Grocery chains are not flashy, but they are reliable. People need food in good times and bad, which gives companies like Kroger the kind of steady cash flow that dividend investors love.

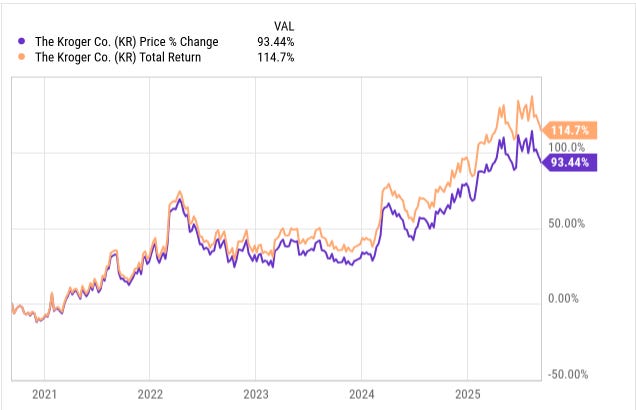

When including all dividends paid, Kroger has provided more than a 114% return over the last five years. And the growth may not be done.

Kroger just delivered another strong quarter with identical sales growth of 3.4%, led by pharmacy, e-commerce, and fresh categories. What stands out to me is how management is leaning into both efficiency and growth. They closed about 60 unprofitable stores and cut nearly 1,000 corporate roles to reduce costs, while at the same time planning a 30% increase in store openings for 2026. That balance of trimming fat and expanding strategically is a big part of why Kroger has been able to consistently reward shareholders.

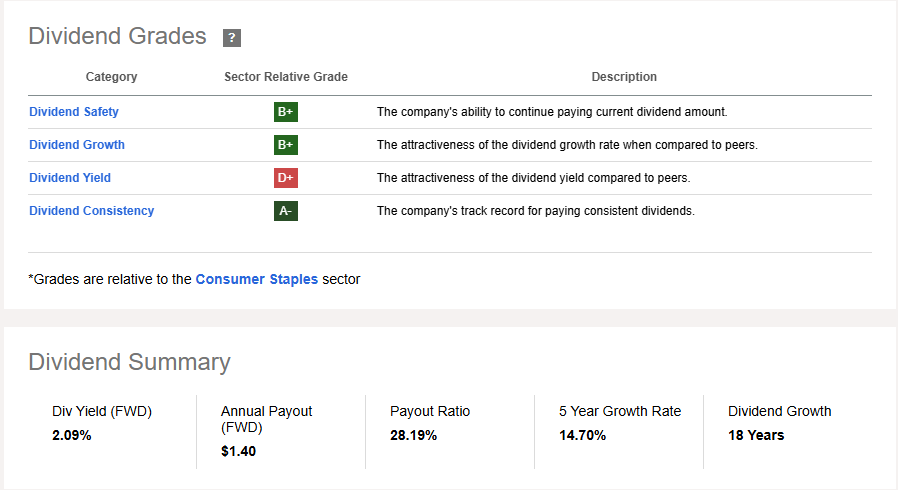

From a dividend perspective, Kroger has done an excellent job at rewarding investors with higher payouts as they increase revenue. Although the dividend yield is relatively low at 2%, the magic is in the dividend raises and safety of the dividends. Kroger has paid out and raised dividends for 18 consecutive years without interruption.

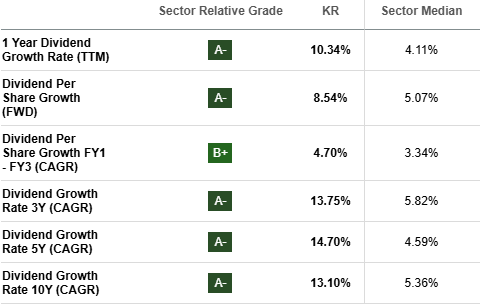

Looking at the dividend data below, Kroger has provided investors with an average annual dividend raise of 13.1% over the last ten years. Imagine getting a 13.1% raise every single year at your job for TEN YEARS STRAIGHT.

E-commerce continues to be a real growth engine, up 16% in the latest quarter, with delivery orders now surpassing pickup for the first time. The company is using stores as fulfillment hubs, which improves margins and makes online sales more scalable.

Financially, Kroger raised its full-year guidance, reporting $1.1 billion in adjusted FIFO operating profit and 12 percent earnings per share growth compared to last year. Most importantly for income investors, the dividend was raised by 9% this quarter. That kind of steady dividend growth means Kroger is not only paying income today, but also working to ensure that income grows over time.

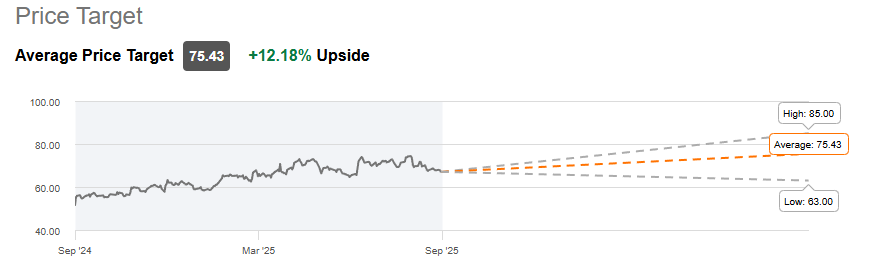

Kroger has an average price target of $75.4 per share, but I anticipate that the the new store openings and boosted revenues next year will take KR over $85 per share at some point. Therefore, I will continue to add shares to my existing KR position.

Pick #2 - Microsoft MSFT 0.00%↑

If Kroger represents the steady, defensive side of dividend income, Microsoft is the opposite side of the coin. It is a global growth engine with one of the strongest moats in the world, and it still rewards shareholders with reliable and growing dividends.

Microsoft just closed out a record year with over $281 billion in revenue, up 15% year-over-year, and more than $128 billion in operating income. Microsoft Cloud alone surpassed $168 billion, growing 23%, with Azure contributing $75 billion at 34% growth. These numbers are not only massive in scale, they highlight the company’s dominance in cloud infrastructure, which has become as critical to the economy today as utilities were in the past.

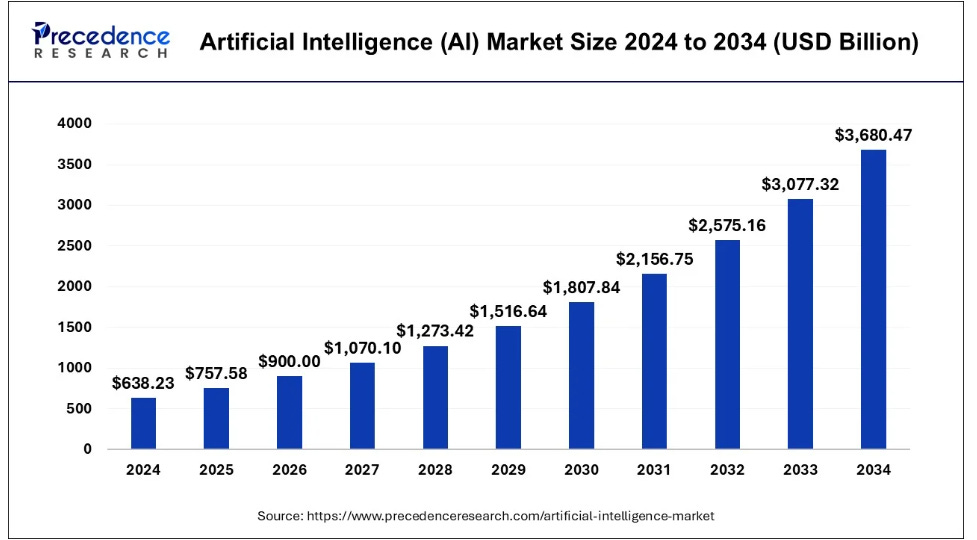

The growth of the AI market is estimate to grow at a CAGR (compound annual growth rate) of 19.20% through 2034. I believe that Microsoft is one of the only companies in the world that is well-suited to continue capturing the growth of AI, with the least amount of risk and volatility.

Beyond the cloud, Microsoft has diversified growth streams across productivity software, gaming, and new AI applications. Microsoft 365 Copilot added its largest quarter of new seats since launch, GitHub Copilot reached 20 million users, and Copilot apps overall now have more than 100 million monthly active users. Fabric, the company’s data platform, grew 55 percent year-over-year, making it the fastest-growing database product in history. Even legacy areas like Windows and Xbox services are contributing to growth.

What ties all these revenue streams together is Microsoft’s moat. Its products are deeply embedded in enterprise workflows, governments, and consumers. Replacing them is nearly impossible without disrupting critical operations. That stickiness is what keeps margins high and revenue streams recurring.

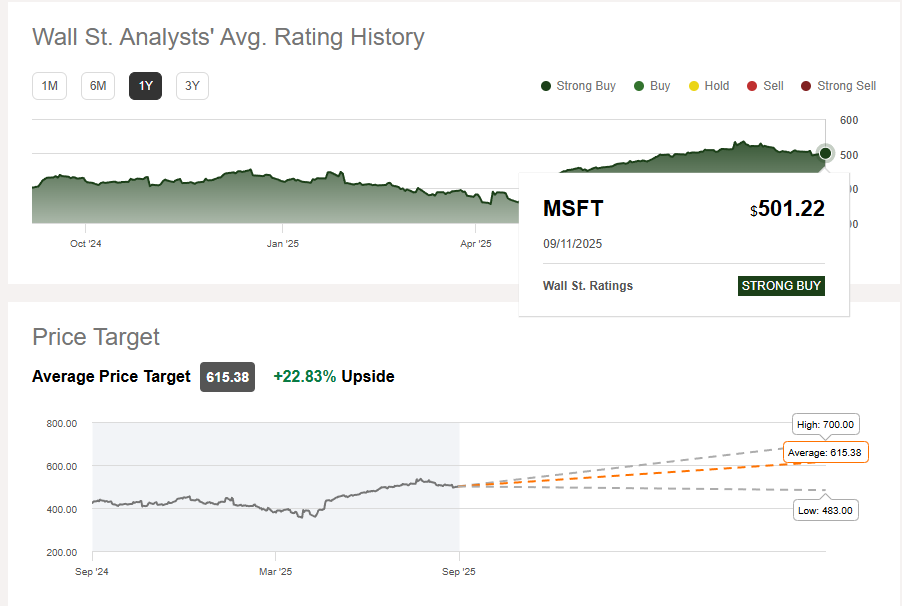

Wall Street analysts still rate MSFT as a strong buy with the highest price target at $700 per share.

For dividend investors, Microsoft’s current yield is modest compared to high-yield funds, but the story here is dividend growth. With free cash flow exceeding $25 billion in a single quarter, the company has both the ability and the history of rewarding shareholders. Over the years, it has consistently raised its payout, turning a small yield today into a meaningful stream tomorrow.

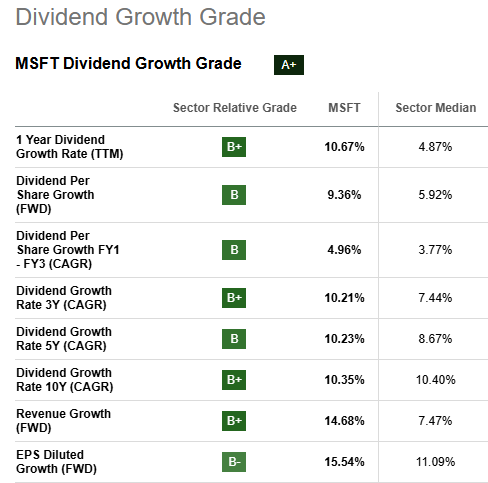

Looking at the dividend growth metrics below, MSFT continues to be strong buy for me. MSFT is still my largest individual position.

This makes Microsoft an ideal complement to income-heavy holdings like ARCC or YMAX YMAX 0.00%↑ . While it may not pay your rent in 2025 on its own, its growing dividends and unmatched stability make it the type of anchor that lets you confidently chase higher yields elsewhere.

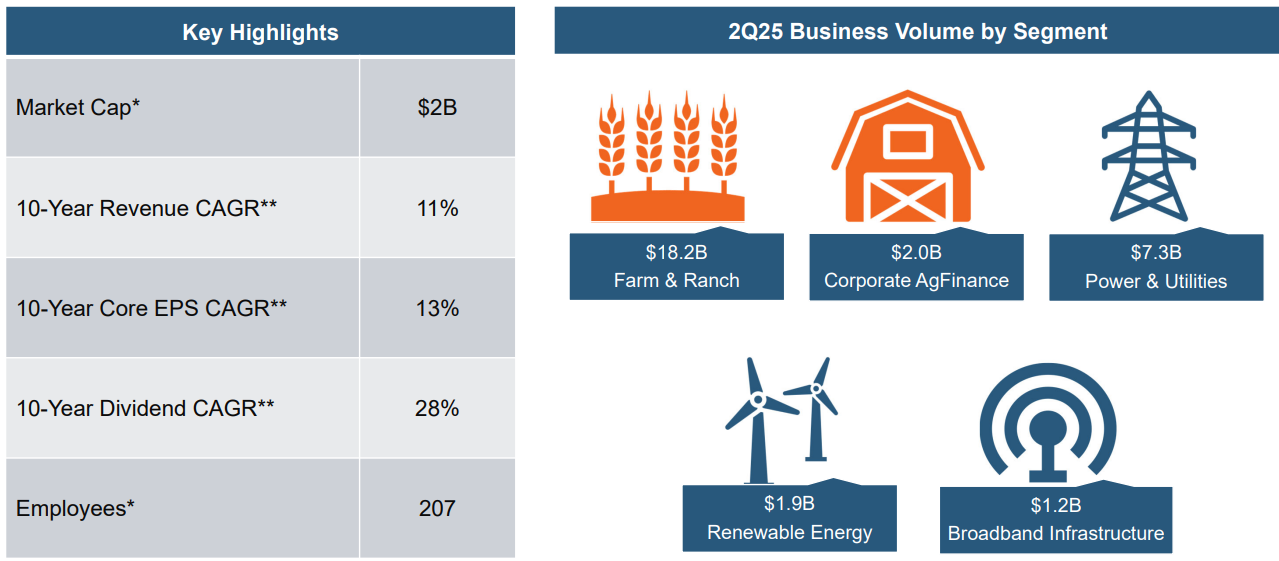

Pick # 3 - Federal Agriculture Mortgage Corp AGM 0.00%↑

This isn’t a popular choice amongst investors and I believe it doesn’t get the attention it deserves. At its core, AGM provides financing solutions to farmers, ranchers, and rural infrastructure projects. Over the last several years, management has strategically diversified into renewable energy, broadband infrastructure, and corporate agribusiness, creating a business model that thrives across different market cycles.

The results speak for themselves. AGM recently reported record core earnings of $47.4 million and surpassed $30 billion in outstanding business volume for the first time. Even more importantly for dividend investors, the company’s dividend profile is remarkably healthy.

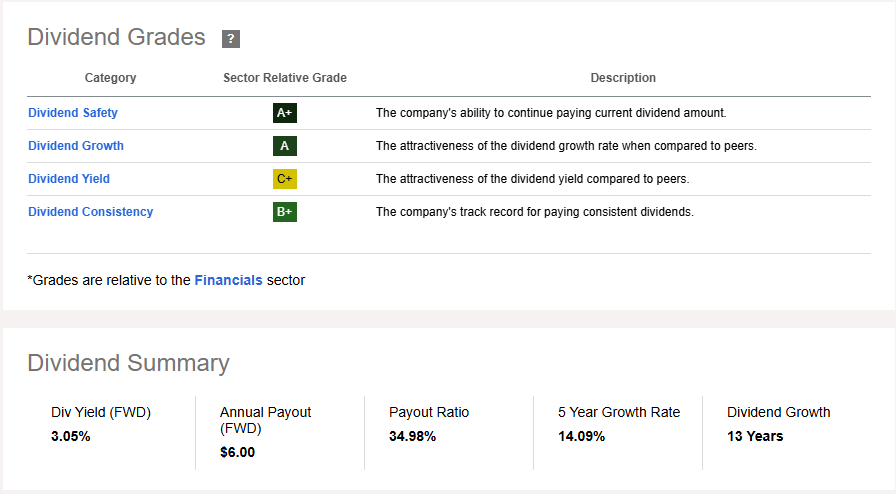

Forward dividend yield sits at just over 3 percent.

Payout ratio is below 35%, which leaves plenty of room for growth.

Dividend growth rate has averaged more than 14% annually over the past five years.

The company has raised its dividend for 13 consecutive years.

These are the types of metrics income investors dream about. A low payout ratio combined with consistent double-digit dividend growth signals sustainability and safety. While some high-yield names deliver income today at the expense of tomorrow, AGM has balanced growth, income, and risk management.

Management’s confidence is clear. Alongside record financials, the board recently expanded the company’s share repurchase program from under $10 million to $50 million through 2027, a move that underscores its commitment to returning capital to shareholders.

For investors, AGM represents a different angle on dividend investing. It may not offer the eye-popping yields of an option-writing ETF, but it delivers something arguably more valuable: steady dividend compounding. In a portfolio that blends high yield and growth, AGM sits firmly in the “quality growth” bucket, gradually building income while preserving capital.

Reminder, I share dividend income reports every single month for readers.

August 2025 Dividend Report

For the month of August, my dividend portfolio paid me $3,991.11 in dividend income. On a year-to-date basis, I’ve now collected over $28,000 in passive income with dividends. I aim to accumulate $100,000 annually in dividends and I want you to join me on the journey. This is money that I didn’t have to actively work for and doesn’t include capital earned through other business ventures.

Nice article!! I wonder what your thoughts are on tariffs and US trade and immigration policy impacts on AGM. Farmers are complaining of no workers, no customers, and that will lead to farm foreclosures. Does that make AGM on the riskier side?

Interesting picks. But framing it as “covering rent” feels a little too neat. Rent goes up every year — Kroger, Microsoft, and AGM might raise dividends, but there’s no guarantee those raises will keep pace with housing inflation. Dividend growth is powerful, but relying on it for fixed expenses can turn into a mismatch pretty fast.