3 High-Yield Funds That Pay Out Tax-Efficient Dividends

These Funds Pay Massive Dividends With Almost No Tax Impact For Investors

Most people think about investing in terms of returns, meaning what percentage they can earn on their money. But what really matters is what you actually keep after taxes.

A paycheck is taxed as ordinary income, meaning you are often giving up 20 to 30 percent of it right off the top depending on your bracket. Dividends, however, can be taxed more favorably.

There are two main types of dividends.

Ordinary dividends are taxed just like your paycheck, at your normal income rate. These often come from REITs, BDCs, and certain funds.

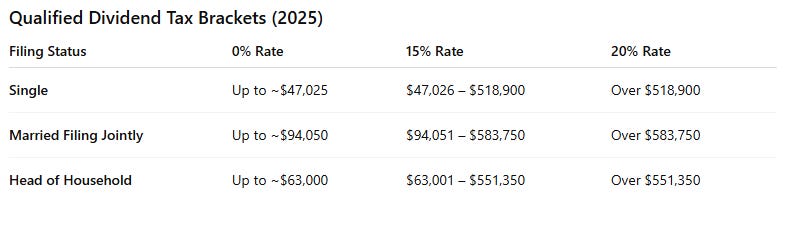

Qualified dividends are taxed at the long-term capital gains rate, which can be as low as zero percent and caps out at twenty percent. Many blue-chip companies, ETFs, and CEFs pay these.

There is also a third layer called Return of Capital, or ROC. Instead of being taxed right away, ROC lowers your cost basis and defers the tax until you sell. This can make a huge difference for high-yield investors.

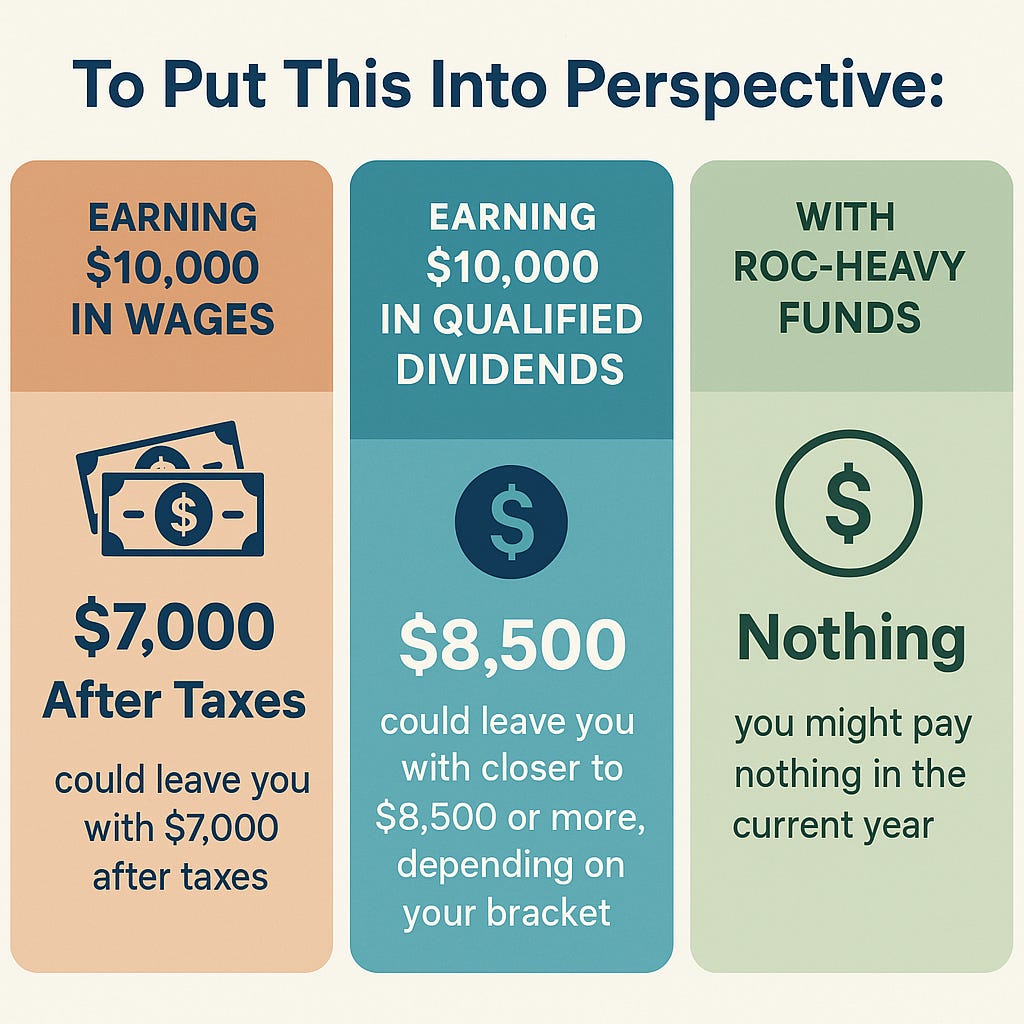

To put this into perspective:

Earning $10,000 in wages could leave you with $7,000 after taxes.

Earning $10,000 in qualified dividends could leave you with closer to $8,500 or more, depending on your bracket.

With ROC-heavy funds, you might pay nothing in the current year.

This is why the quality of dividends matters just as much as the yield. A six percent qualified dividend can actually leave you richer than a ten percent ordinary dividend once Uncle Sam takes his cut. Additionally, qualified dividends can actually result in no taxes depending on your tax bracket and income levels. The breakdown is as follows:

So I wanted to share 3 funds that offer massive dividend yields and offer tax-free dividends using a healthy Return Of Capital classification.

How Return Of Capital Works

Let’s imagine that you buy a stock at $10 per share and it pays out a $1 dividend using return of capital. Once the dividend of $1 is paid, your cost basis would be reduced to $9 per share and you wouldn’t owe taxes on the dividend received.

Since your cost basis is reduced, this essentially allows taxes to be deferred until the time of sale. So if you were to sell your position while your cost basis is $9 per share, you would pay taxes on the ‘capital gain’.

But what if you never sell your position?

Well, it’s technically possible to hold a long-term position long enough for your cost basis to reach $0 per share, if the fund continuously pays out using Return Of Capital year after year. At this point, all distributions received would be classified as long-term capital gains, which are qualified dividends and are still tax-efficient.

Pick #1: IYRI – Real Estate Sector Option Income ETF

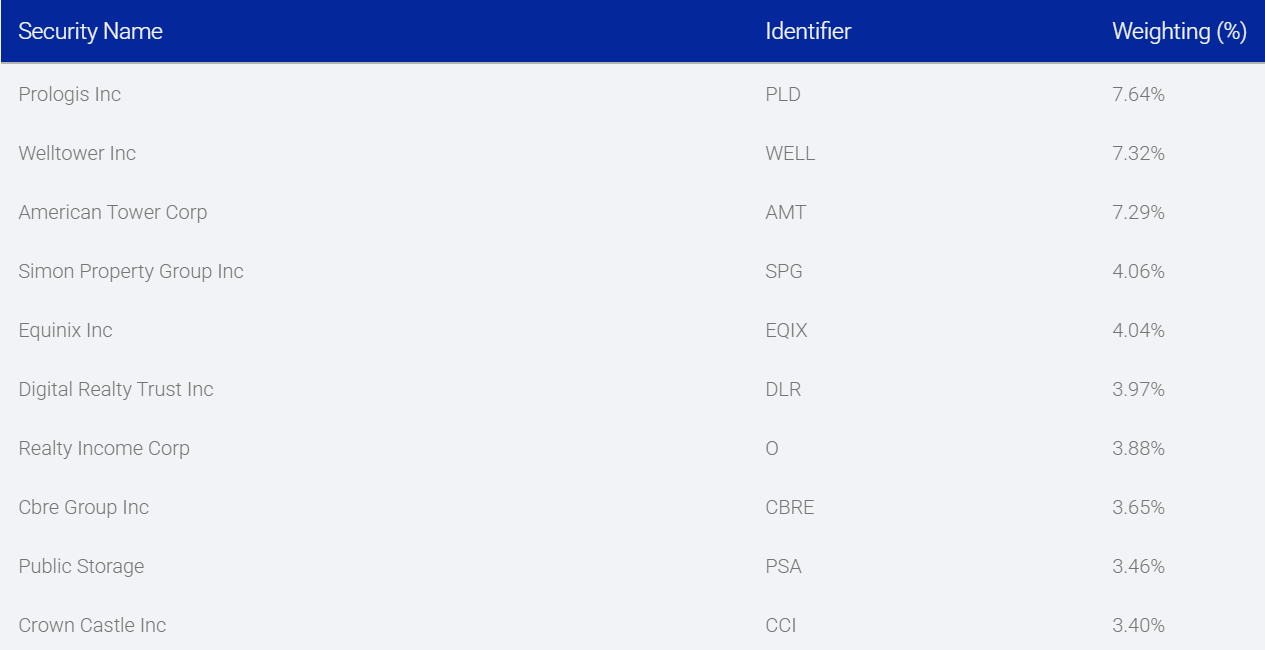

IYRI targets the U.S. real estate sector, providing investors a way to earn high income from a traditionally dividend-friendly space. Rather than owning individual REITs directly, IYRI holds a portfolio of derivatives that track the real estate index, then sells covered calls against that exposure. This option overlay generates the bulk of the income distributed to shareholders.

Prologis PLD 0.00%↑

Welltower WELL 0.00%↑

American Tower AMT 0.00%↑

Simon Property Group SPG 0.00%↑

Equinix EQIX 0.00%↑

Digital Realty DLR 0.00%↑

Realty Income O 0.00%↑

Much like other option-income ETFs, IYRI distributions are often classified as Return of Capital. That means the income isn’t fully taxable in the current year and this is a significant benefit since many REIT dividends are normally taxed as ordinary income. By converting REIT exposure into ROC-heavy distributions, IYRI helps real estate investors keep more of what they earn.

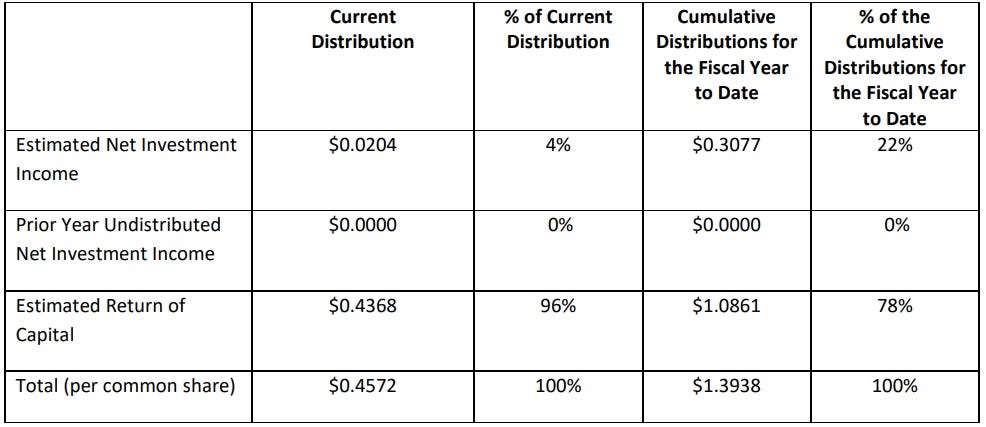

The current estimated dividend yield sits around 10.8%. Since the ETF's operating history is so short, it's too soon to speak on the consistency of the dividend payouts. Looking at the most recent distribution breakdown, IYRI’s dividend’s paid YTD were fueled mostly by Return of Capital.

Let’s use the numbers from the % of Cumulative Distributions for the Fiscal Year to Date column in the Section 19(a) notice:

22% = Net Investment Income (taxable as ordinary income)

0% = Prior Year Undistributed NII

78% = Return of Capital (not taxed currently)

👉 If you receive $10,000 in dividends:

$2,200 (22% of $10,000) = taxable as ordinary income.

$7,800 (78% of $10,000) = ROC → no current tax.

👉Tax burden estimate (example at 24% bracket):

$2,200 × 24% = $528 owed in federal tax.

So under the cumulative breakdown, your tax burden would be about $528 on $10,000 of distributions. This is AMAZINGLY TAX-EFFICIENT.

There are almost no other scenarios where you can receive $10,000 in passive income and only pay ~$528 in taxes for the year.

👉Do you want more high-yields like this with minimal tax consequences? Consider upgrading to a paid membership to unlock the rest of the article. I’ve put together a few special offers running until September 30th:

The 2nd pick here is 100% tax-free.

Discounted Annual Plan

✅ 10% off forever, even through future price increases – Lock in a discounted subscription rate. Exclusive access to all articles, buy & sell alerts, dividend income reports, occasional portfolio updates, and more.

3-Month Access + High-Yield Guide

✅ High-Yield Option ETF Guide + 3 months paid access – Your starting point for building predictable monthly income. 30+ different high-yield funds included.