3 Safe High-Yield Investments That Can Pay You for Life

How to build dependable passive income without chasing risky yields.

When I first started chasing dividend income, I thought I had struck gold. The logic seemed simple enough: find the highest yield and enjoy bigger paychecks every month. I bought into funds promising 60%, 75%, even 100% yields. At the time, it felt like I had discovered a shortcut to financial freedom. & Yes, I am telling the truth, these funds do exist.

Of course, I wasn’t the first to fall for this illusion. History is full of investors who learned the hard way that sky-high payouts often come with hidden risks. In the roaring 1920s, for example, plenty of companies lured investors with extravagant dividends, only to see them vanish when the Great Depression hit. The same story has repeated itself in every generation: yields that look too good to be true usually are.

It didn’t take long for me to realize the same lesson firsthand. A few dividend cuts later, not only had my income evaporated, but my portfolio’s value had been stagnant in the process. What I thought was a fast track to financial independence turned out to be a dangerous detour.

That’s when I began to shift my approach. Instead of chasing the biggest number, I started asking a different question: what kinds of investments can actually keep paying for decades? Over time, that mindset led me to focus on just three areas of the market. These are the safest sources of high yield I’ve found, and they’re the ones I believe can realistically provide an investor with income for life.

1. VICI Properties (VICI 0.00%↑) - REITs

Real estate has always been a cornerstone of wealth building, but buying and managing property directly is expensive and time-consuming. REITs offer a way for investors to capture the income and appreciation of real estate without the headaches of tenants, maintenance, or massive upfront costs. Most people don’t even know that you can maintain exposure to real estate through the stock market.

One of the best examples is VICI Properties. VICI owns some of the most iconic casino and entertainment venues in Las Vegas, including Caesars Palace and the Venetian, along with properties across the country leased to major operators like MGM Resorts and Bowlero. These are “experiential properties,” places where people go to spend money on gaming, entertainment, and leisure, and they are notoriously difficult to replicate. That scarcity gives VICI unique pricing power and long-term stability.

What makes VICI especially attractive is how it structures its leases. Nearly all of its portfolio operates under triple net leases, which means tenants are responsible for taxes, insurance, and maintenance. This structure passes most of the unpredictable costs back to tenants and gives VICI steady, predictable cash flow. On top of that, most of VICI’s leases are protected by parent guarantees and master lease agreements, ensuring that rent continues to flow even if individual properties or tenants face challenges. This has allowed VICI to maintain an uninterrupted record of full rent collection, even through periods like the pandemic when much of the entertainment industry was shut down.

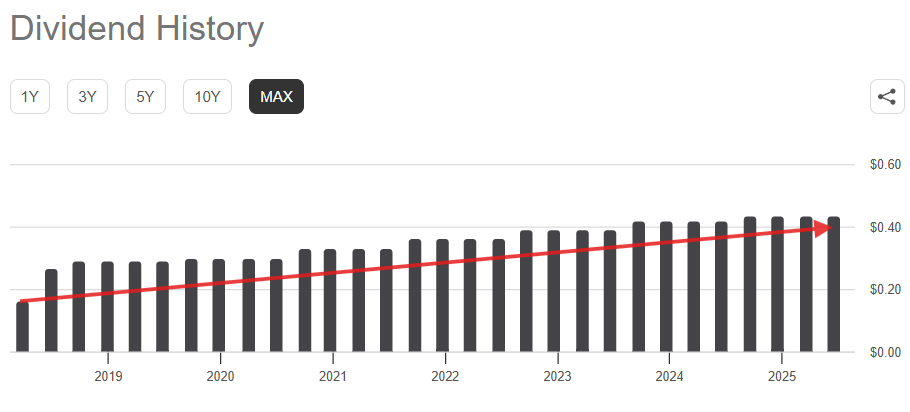

From an income perspective, VICI currently pays a dividend yield a little above five percent, comfortably supported by funds from operations. Unlike many high-yield names that stretch to sustain payouts, VICI’s dividend is both well covered and steadily growing. Since its public debut in 2017, the company has already raised its dividend significantly, building a strong track record of rewarding shareholders.

If you choose the correct investment, the dividend will be increased over time. This means your passive income will continuously increase without any effort on your front.

The potential does not end with stability. VICI is expanding beyond gaming into other experiential categories like waterparks, wellness resorts, and live entertainment venues. It has approached this carefully, often starting with loans or minority stakes that allow it to test the waters before committing fully. This strategy positions VICI for long-term growth without taking on reckless risk.

In short, VICI combines the best of both worlds: the reliable income of a high-quality REIT with the growth potential of a company that continues to expand its reach. For income-focused investors, it is one of the rare high-yield opportunities that can be called both generous and safe.

2. Ares Capital (ARCC 0.00%↑) - Business Development Company

Another powerful source of reliable high-yield income comes from Business Development Companies, better known as BDCs. These firms were created by Congress in 1980 to channel capital into small and mid-sized American businesses that often cannot access funding through traditional banks. In return for providing this financing, BDCs collect interest and fees, then pass much of that income along to shareholders as dividends.

So as the name ‘business development company’ implies, these are firms that lend capital to help developing businesses. A BDC puts you on the receiving end of interest payments.

The appeal for income investors is obvious. BDCs are required by law to distribute at least 90 percent of their taxable income to shareholders, which results in dividend yields that are often far higher than those found in the broader market. The key, however, is choosing the right BDC because while some take on excessive risk, others have built decades-long track records of consistent performance.

One name that stands out to me is Ares Capital Corporation, better known by its ticker ARCC. It is the largest BDC in the United States, and that scale gives it unique advantages. ARCC lends to hundreds of different companies across a wide variety of industries, which means that its income stream is highly diversified. The company is also managed by Ares Management, one of the world’s leading alternative asset managers, giving it access to deep expertise and resources that many smaller BDCs cannot match.

In other words, ARCC combines the high yields that investors look for in this space with a level of discipline and stability that makes it one of the safer options.

If you are ready to take these principles and build a real plan for your finances, I have two ways to help.

My Book — The Dividend Income Blueprint

This is my step-by-step guide for building a portfolio that pays you consistent monthly income for the rest of your life. It walks you through exactly how to find, buy, and manage income-producing assets so you can create financial freedom without gambling or guessing. Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

One-on-One Consulting

If you want personal guidance tailored to your situation, I offer private consulting sessions where we map out your income goals, investment strategy, and the exact steps you can take right now to start building wealth.

ARCC’s portfolio is anchored in senior secured loans. Roughly two thirds of its investments sit in first or second lien positions at the top of the capital structure. This means that if a borrower defaults, ARCC has the first claim on assets. That protection is critical in an environment where borrowing costs have risen and weaker companies can struggle to refinance.

The underwriting quality here is also best in class. ARCC consistently keeps its non accruals, which are loans that stop paying interest, at extremely low levels well below many of its peers. For investors, this is a direct indicator that the dividend is built on real, dependable cash flow rather than risky bets.

Speaking of dividends, ARCC’s yield currently sits around 9 percent, and it is well supported by net investment income. Management has not cut the base payout since 2009, which is a rare feat in this sector. Over time, ARCC has even delivered supplemental dividends when results were especially strong, further rewarding shareholders. The company also holds taxable spillover income, giving additional visibility that distributions can remain stable going forward.

3. Covered Call ETFs - +25% Yields

One of the fastest growing categories in the income investing world is covered call ETFs. These funds use a simple strategy: they buy a basket of stocks, usually tied to an index, and then sell call options on those holdings. The option premiums collected are passed on to investors as income, which is why covered call ETFs often pay yields far higher than the underlying index.

For many investors, the appeal is clear. These funds provide exposure to large, familiar benchmarks while layering on additional income. Instead of simply owning an index like the S&P 500 or Nasdaq 100 and waiting for price appreciation, you get regular cash flow from the option premiums. The trade off is that your upside is capped if the market surges, but for income focused portfolios, that is often a fair exchange.

What makes the new wave of index tracking covered call ETFs particularly attractive is their discipline and transparency. Rather than using a manager’s discretion, they follow a rules based approach tied to well known indexes. That means investors know exactly what they are getting. If the Nasdaq 100 is up, you still participate in that growth, but with the added benefit of enhanced income. If the market is flat or choppy, the income stream from option premiums can still make holding worthwhile.

If you are a free reader, this is where I have to stop. Paid subscribers get access to my full breakdowns, specific allocations, and the exact way I combine these holdings to create reliable monthly income.

👉 Upgrade to a paid subscription to see my full portfolio strategy and receive new high-yield ideas as I add them.