4 Undervalued Dividend Stocks In An Overvalued Market

These 4 stocks remain undervalued and offer double-digit upside potential.

Even with the market trading near record highs, there are still opportunities hiding in plain sight. Many investors assume that all quality dividend stocks are already overvalued, but that is not the case. Certain companies continue to trade at attractive valuations relative to their long-term growth potential, giving patient investors a chance to accumulate shares at fair prices.

By identifying these undervalued gems, we can outperform market indexes with ease.

👉 Over The Last 12-Months:

👉 My portfolio: 26.55%

👉 US Stocks: 17.74%

In this article, I will highlight four companies that I believe are undervalued based on current market conditions and future growth prospects. Each one operates in a different sector, yet they share a similar foundation of strong cash flow, disciplined management, and consistent dividend growth. Together, they represent a diversified mix of technology, healthcare, retail, and consumer staples.

👉 If you need help identifying these opportunities, the Yieldly Dashboard can help!

👉 Lock in a discount rate on Yieldly access forever!

Pick #1: Meta Platforms META 0.00%↑

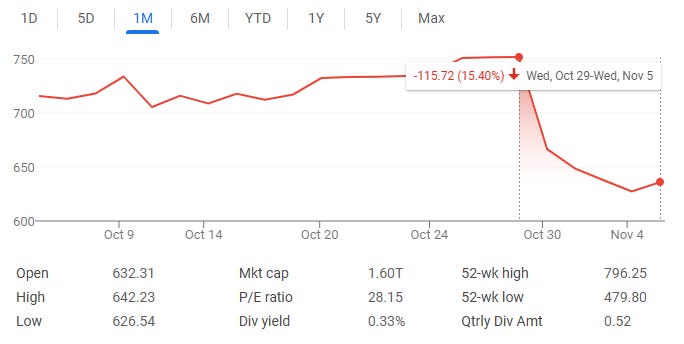

Meta continues to be one of the most misunderstood companies in the market. Despite its enormous scale and proven profitability, many investors still view it as an expensive growth story rather than a disciplined cash-flow machine. After its recent earnings report, the price experienced a large pullback of more than 15%. Remember, pullbacks are where we can build wealth and initiate a starter position.

So what’s the reason for the pullback?

Meta said it will “spend aggressively” next year, warning its capital expenditures will be “notably larger” in 2026 and total expenses will grow at a “significantly faster percentage rate.”

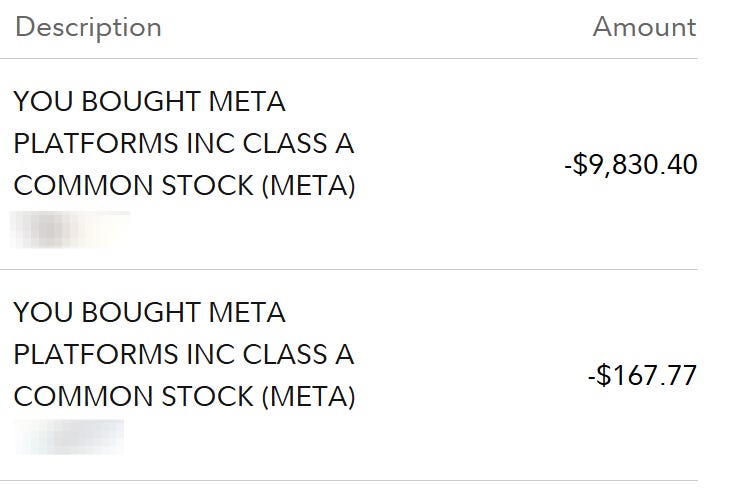

👉 Full Disclosure, I initiated my starter position in Meta this week.

So what. Zuckerberg believes that it makes the most sense to front load these investments in the AI space. The sector has rewarded those who get the early movers advantage and I believe that META is positioned to remain a leader in the space.

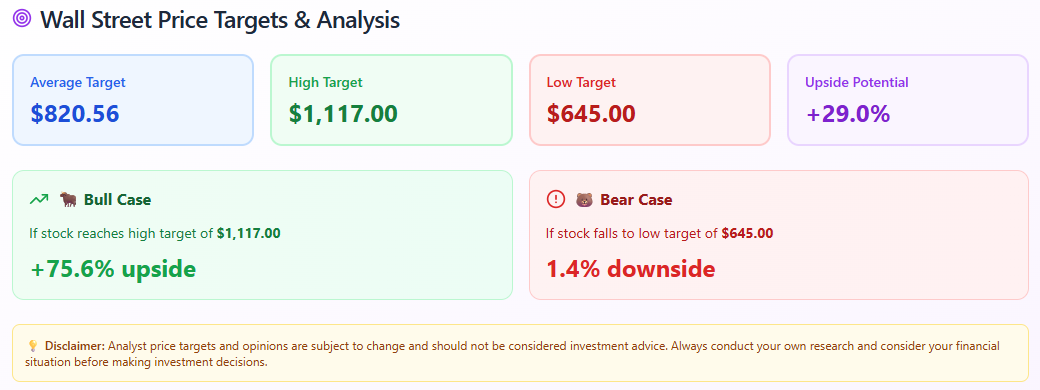

According to Yieldly, analyst projections suggest that the stock remains undervalued even after a strong run. Wall Street currently places the average price target near $820 per share, implying an upside potential of about 29% from recent levels. In a more optimistic scenario, analysts see the possibility of a move toward $1,117, which would represent an upside of more than 75%.

Why it appears undervalued:

Strong free cash flow that supports dividend expansion and buybacks

Large cash reserve exceeding fifty billion dollars with minimal debt

Continued user engagement growth across core platforms

Leadership position in AI infrastructure and monetization opportunities

For dividend investors, Meta provides a rare combination of growth, income, and balance sheet strength. It offers exposure to long-term innovation while providing a new and growing dividend stream that is well covered by cash flow.

✅Learn how to structure your dividend portfolio. I bundled together some of the most useful tools to get you started on your journey.

✅ Earn 3-months of access when purchasing the bundle!

Pick #2: Target TGT 0.00%↑

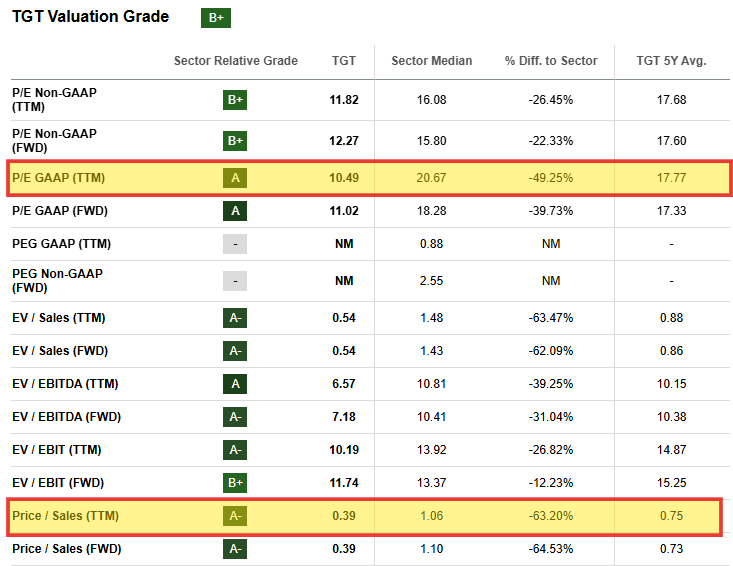

Target remains one of the most attractively valued dividend payers in the retail sector. Despite short-term challenges in consumer spending, the company continues to demonstrate solid fundamentals and disciplined financial management. Shares currently trade around $92, which is well below the company’s historical valuation range and the broader retail sector averages.

From a valuation standpoint, Target’s metrics continue to stand out. The company trades at a forward price-to-earnings ratio of 12.3, compared to a sector median above 15. Its EV to EBITDA ratio is also about 30% below the sector average, indicating that investors are not fully pricing in a recovery in margins and same-store sales.

Dividend Appeal:

Target has raised its dividend for over 50 consecutive years, placing it among the small group of companies recognized as Dividend Kings. The stock currently offers a yield of roughly 3%, supported by consistent free cash flow and a payout ratio that leaves room for future growth.

Why it appears undervalued:

Strong brand loyalty and nationwide scale

Trading at a discount to both its five-year average and sector median valuations

Ongoing improvements in logistics and cost management

Reliable dividend history and shareholder-friendly policies

Target may not deliver explosive growth, but it offers something more valuable for long-term investors — stability, income, and a clear path to sustainable recovery as the retail environment normalizes.

👉Upgrade to a paid membership to view the full list. There is an attached Seeking Alpha Analysis at the end of this article for pick #4.

Not ready to upgrade? That’s fine! When you become a free subscriber today, you will gain access to the following:

✅50+ Monthly Dividend Stocks provides a list of tickers that send income to your account every single month.

✅ETFs for Beginners breaks down income focused funds that simplify the investing process.

✅Dividend Legends highlights companies with long histories of increasing dividends through every type of market.

These are tools that will help you get your dividend journey started!

Pick #3: The Kroger Co. KR 0.00%↑

Kroger continues to demonstrate how a traditional retailer can adapt successfully to modern consumer habits. The company has made meaningful progress by expanding its online presence, strengthening its private-label offerings, and improving operating efficiency. Management recently outlined plans for a 30 percent increase in store openings by 2026, which highlights Kroger’s confidence in both its customer base and long-term strategy.

In its most recent earnings update, management reported that identical sales without fuel grew by 3.4%, marking the company’s sixth consecutive quarter of positive growth. This performance was driven by strength in pharmacy, e-commerce, and fresh food categories. At the same time, Kroger continues to close underperforming stores and streamline operations, helping preserve margins in a competitive environment.

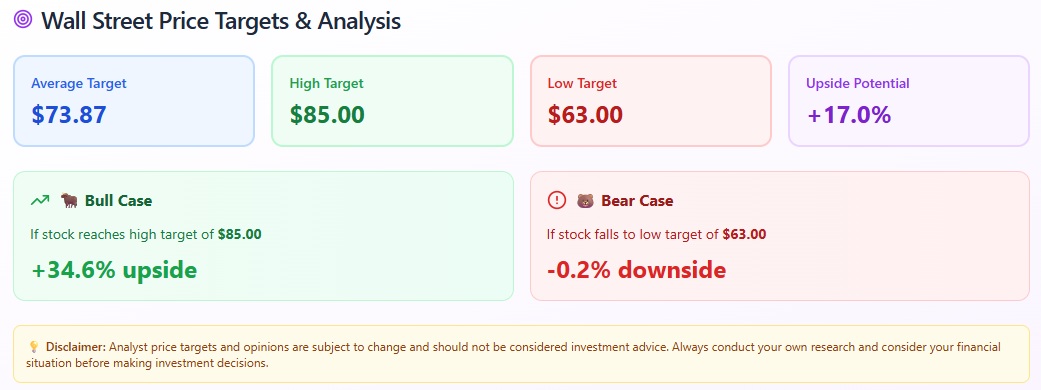

From a valuation perspective, Kroger remains attractively priced relative to peers. The current average analyst price target sits near $74 per share, which represents an upside potential of around 17%, with a high-end target of $85 per share. These estimates suggest that the market may still be underestimating Kroger’s long-term earnings power as it continues to grow digital and delivery channels.

👉 Dividend Appeal

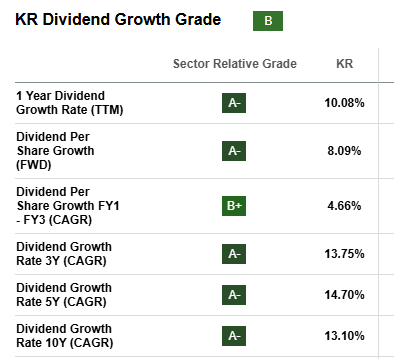

Kroger offers a stable dividend yield near 2.3% and has consistently raised its payout for more than 15 consecutive years. The company’s focus on cost control and consistent free cash flow supports continued dividend growth, while periodic share repurchases add another layer of shareholder return.

Pick #4: Amgen AMGN 0.00%↑

Amgen remains one of the most resilient companies in the healthcare sector, supported by a diversified product lineup and a strong pipeline of next-generation therapies. While many biotech stocks have struggled to maintain momentum, Amgen has continued to deliver consistent results.

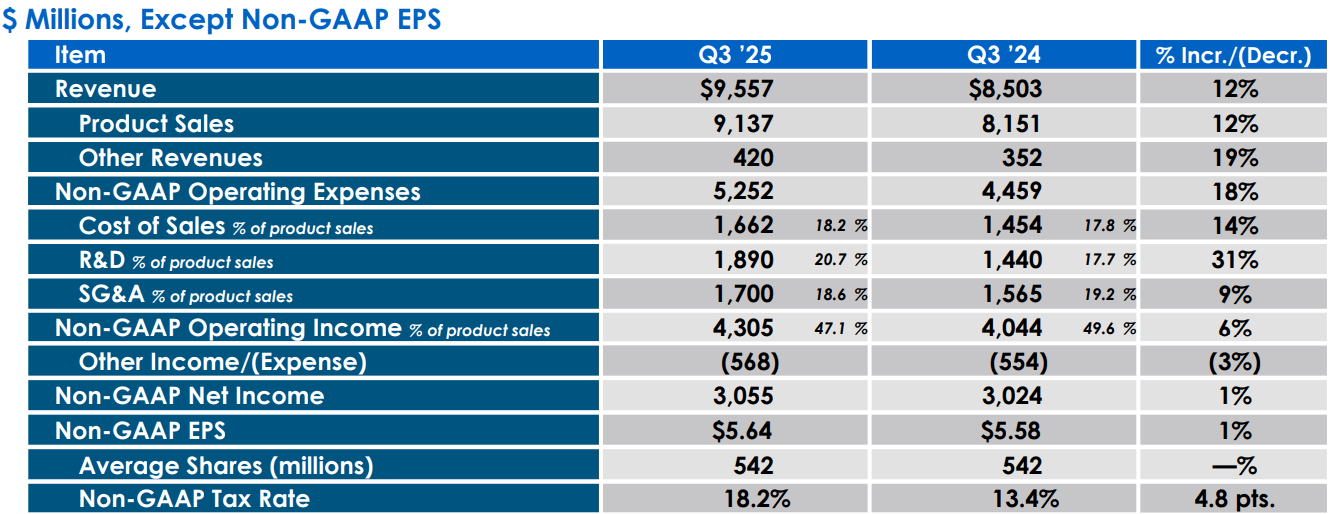

Recent quarterly results highlight this stability. Revenue grew 12 percent year-over-year, supported by strong performances across general medicine, oncology, and rare disease categories. Earnings per share also came in ahead of expectations, reflecting the company’s continued ability to manage costs and improve margins.

The company combines consistent profitability with one of the largest research and development budgets in the entire biotech industry. In 2024, Amgen invested approximately $5.1B into R&D, representing about fifteen percent of total revenue. This level of reinvestment highlights management’s focus on expanding the company’s drug pipeline and sustaining growth well into the next decade.

I wrote a more dedicated piece on AMGN! You can read that for free below -