4 Undervalued Tech Companies That I'm Buying With My Dividends

Turning passive income into long-term growth through four innovative companies that remain underpriced.

For years, I’ve been building my portfolio around one simple goal: creating cash flow that buys me freedom. But lately, I’ve started doing something different with that cash.

Instead of spending my dividends or letting them sit idle, I’ve been quietly redirecting them into a handful of growth positions that I believe can multiply in value over the next several years.

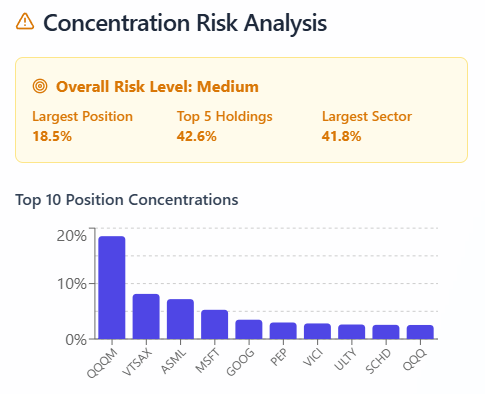

As we can see below, my largest position is actually the Invesco NASDAQ 100 ETF QQQM 0.00%↑, which contains stocks like:

Nvidia NVDA 0.00%↑

Apple AAPL 0.00%↑

Broadcom AVGO 0.00%↑

Amazon AMZN 0.00%↑

Tesla TSLA 0.00%↑

Meta META 0.00%↑

Alphabet GOOG 0.00%↑

As those dividends grow, I can funnel more into a select group of companies that I believe the market is still mispricing. These are companies that quietly dominate their industries yet continue to trade as if their best days are behind them.

Not ready to upgrade to a paid subscription? That’s fine! When you subscribe as a free member, you still get access to these FREE Downloads!

✅ Dividend Growth Legends - Companies with over 50+ years of dividend raises.

✅List of ETFs For Beginners

✅50+ Monthly Paying Dividend Stocks

Self-Funded Portfolio Growth

What I’ve learned is that dividends do more than build income. They build momentum. Every payout I receive represents fresh capital that I didn’t have to earn through work. When I redirect those dividends into new positions, the portfolio begins to sustain itself.

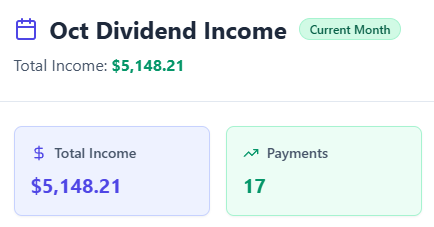

👉For instance, Yieldly estimates that I will collect more than $5K in dividends for October. How long would it take you to go to work, save cash, cut back on expenses, and then invest $5K a month? This is what I mean by self-sustaining.

Margin used to buy income ETF → Dividend received → dividend reinvested into growth position.

This strategy has allowed me to outperform market indexes over the last twelve months.

Over time, this approach does more than increase income. The goal is not to chase speculation or time the market. It is to let the cash flow from stable income holdings quietly finance exposure to future innovators and the companies that will shape the next decade of progress.

Pick #1: ASML Holdings ASML 0.00%↑

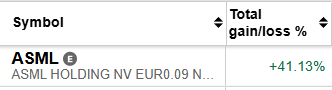

I started originally accumulating ASML back in January of 2025. Since then, the stock took off and I am now up more than 41% on my position. ASML is one of those rare companies that most investors have heard of but few truly understand. It is not a chipmaker. It is the company that makes advanced chipmaking possible.

Its lithography machines are the most complex manufacturing systems on earth, used by every major semiconductor foundry to produce next-generation chips. Without ASML, companies like Nvidia, TSMC, and Intel would struggle to produce the processors that power everything from smartphones to AI data centers.

If you have no clue what ASML does, I recommend watching the video below.

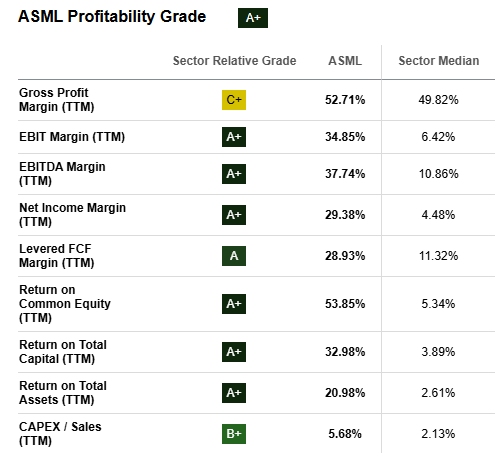

In the third quarter of 2025, ASML reported strong results with more than five billion euros in new system bookings and steady gross margins above fifty percent. The company continues to benefit from record levels of capital expenditure in the semiconductor industry as hyperscalers and AI developers race to expand their data center capacity.

While revenue growth was modest, profitability and order flow remain strong. Free cash flow was positive, and the company reaffirmed its outlook for fifteen percent full-year growth. Management also acknowledged potential headwinds from China-related export restrictions, but those risks appear largely priced in.

ASML is currently worth about $400B.

I believe this is a trillion dollar company.

Which means that the price can still 2.5x from its current level.

For me, ASML represents the kind of company worth owning indefinitely. Its machines will remain essential to AI hardware for years to come, and its business model provides both resilience and scalability.

As an added bonus, ASML offers excellent dividend growth -

👉Get 10% off an annual place FOREVER. Offer ending on October 30th. You will automatically get access to the Yieldly Dashboard, which comes with the subscription.

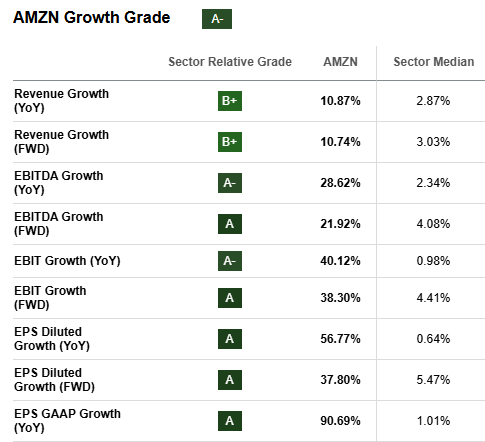

Pick #2: Amazon AMZN 0.00%↑

Amazon remains one of the few large-cap tech companies that still feels undervalued relative to its long-term potential. While most of the market’s attention has shifted to names like Nvidia and Microsoft, Amazon has quietly built the infrastructure that makes the modern digital economy possible.

The company’s strength lies in its three growth engines:

e-Commerce

Advertising

AWS - Amazon Web Services.

Each segment operates at massive scale, and together they create a diversified ecosystem that can withstand almost any market cycle.

Right now, Amazon is in the middle of a heavy investment phase. It is expanding data centers, automating fulfillment, and building its own AI infrastructure. These investments have temporarily compressed margins, but they are setting the foundation for significant future profitability.

What the market often overlooks is how much leverage Amazon has in its business model. Cloud services and advertising are both high-margin segments that are growing faster than retail. As these continue to scale, the company’s overall operating margin should steadily rise. I believe consolidated margins could expand from around twelve percent today to over twenty percent within the next five years.

Amazon also benefits from something that many pure AI companies lack: durable cash flow. It earns consistent revenue from AWS and advertising regardless of market sentiment. This means that it can self-fund its AI ambitions rather than rely on outside capital or hype-driven valuations.

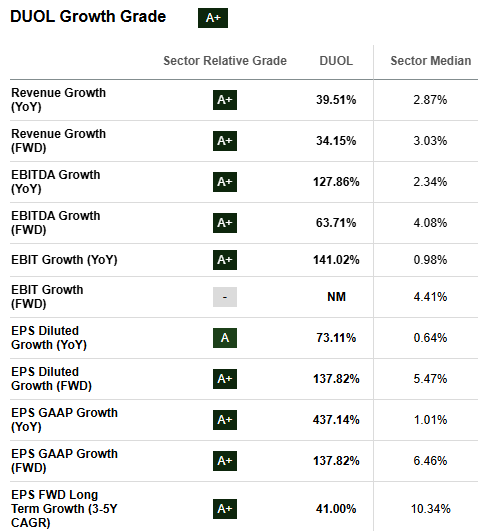

Pick #3: Duolingo DUOL 0.00%↑

Duolingo has quietly become one of the most fascinating tech stories in the market. While many investors are focused on the large, obvious AI names, Duolingo is using artificial intelligence in a way that feels far more personal. It is turning education into a scalable, data-driven experience that millions of people interact with every single day.

The stock is now down over 42% from its highs over 6 months ago. I believe this is a massive buying opportunity.

The company now has more than 47M daily active users, a number that continues to grow at a double-digit rate year after year. Over ten million of those users are paying subscribers, and that base keeps expanding as Duolingo introduces new premium features. Subscription revenue already accounts for more than eighty percent of total sales, giving the company predictable, recurring cash flow that resembles a software-as-a-service model more than a traditional app.

What makes Duolingo unique is how it uses AI to personalize learning. Its Duolingo Max tier allows users to practice conversations with an AI character that can correct mistakes in real time. The more people use the platform, the smarter it becomes. Each interaction adds to an enormous data set that no competitor can match, creating a feedback loop that continually improves both engagement and retention.

Despite its growth, the valuation still leaves room for upside. Analysts expect revenue to increase more than thirty percent in the coming year, with steady margin expansion as more users upgrade to paid plans. Based on current projections, Duolingo could deliver returns between seventy and one hundred fifty percent over the next few years as the business scales.

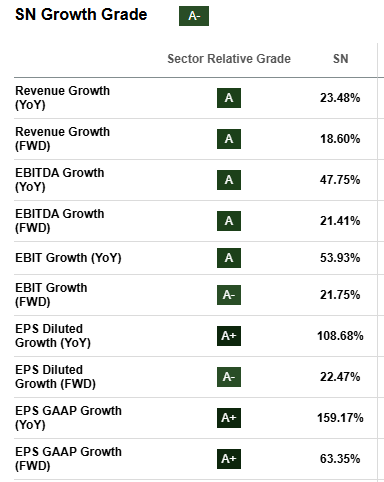

Pick #4: SharkNinja SN 0.00%↑

SharkNinja is a consumer technology company that often flies under the radar, but its execution and growth story deserve much more attention. While many tech names depend on digital ecosystems, SharkNinja thrives in the physical world by building products people use every single day.

The company has established itself as a category leader in home appliances through constant innovation and disciplined growth. In its most recent quarter, SharkNinja reported sixteen percent revenue growth, a thirty-three percent increase in EBITDA, and a gross margin approaching forty-nine percent. These results show the strength of its product lineup and the efficiency of its operations.

What makes SharkNinja stand out is its ability to combine growth with profitability. The company consistently expands into new product categories while maintaining strong margins, something that few consumer brands manage to achieve. It currently operates across cooking, cleaning, food preparation, and home environment products, each of which continues to gain market share.

SharkNinja’s growth strategy revolves around three pillars:

expanding into adjacent product categories

increasing market share in existing segments

scaling internationally.

It has already seen strong success in markets such as France, Germany, and the Benelux region, and it continues to target further expansion in Europe and Latin America.

The company’s financial outlook remains healthy. Management expects earnings per share to grow between sixteen and eighteen percent annually through 2026, supported by consistent revenue growth and improving efficiency. At around nineteen times forward earnings, the stock trades at a reasonable valuation relative to its growth profile.

2 Weekly Paying ETFs With Dividend Yields Above 30%

There’s something powerful about getting paid every week.