$500/Month in Dividends: The Beginner Formula That Anyone Can Follow

A simple roadmap for beginners to reach consistent, meaningful dividend income faster than they think.

Most people start dividend investing because they want more control over their money. They want income that does not depend on their boss, their schedule, or the economy. The idea of collecting steady cash flow from a portfolio is exciting, but beginners often freeze at the first question that truly matters.

How much do I need to invest to make this real?

I still remember when my dividend income barely covered a cup of coffee. It felt slow and sometimes discouraging, but it kept growing. Month after month, year after year, the snowball began to form.

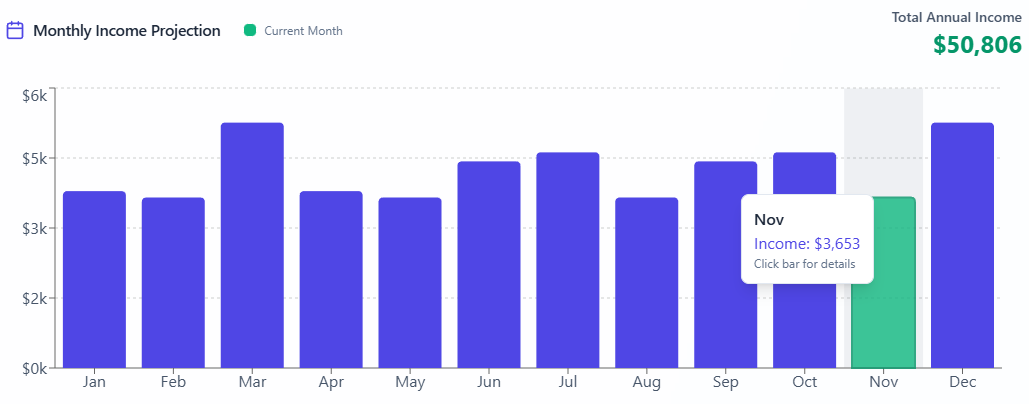

👉 Today, my portfolio is generating more than $50,000 a year in dividends.

It did not happen because I found a secret shortcut. It happened because I focused on one milestone at a time. The first meaningful target I ever set for myself was simple.

Reach five hundred dollars per month.

This is the point where everything changes. Five hundred dollars feels real. It pays bills. It creates confidence. It proves that your portfolio can produce income regardless of what happens at work or in the market. It turns abstract motivation into actual cash flow.

The best part is that you do not need a massive account to begin. You only need a clear plan, a workable structure, and consistency. In this article, I will show you exactly what it takes to reach five hundred dollars per month in dividends using realistic yields, real examples, and a simple system that beginners can follow. You will also see how to run your own numbers using the Yieldly dashboard so you can personalize the timeline based on your current situation.

Let’s build your plan.

The Math Behind $500 Per Month

Reaching $500 per month in dividends may sound overwhelming at first, but the math is simpler than most people expect. Dividend income is determined by three inputs:

How much you invest

The yield of your portfolio

How consistently you reinvest or add new capital.

$500 per month equals $6,000 per year in dividend income. From there, everything becomes a straightforward calculation.

Here is the formula:

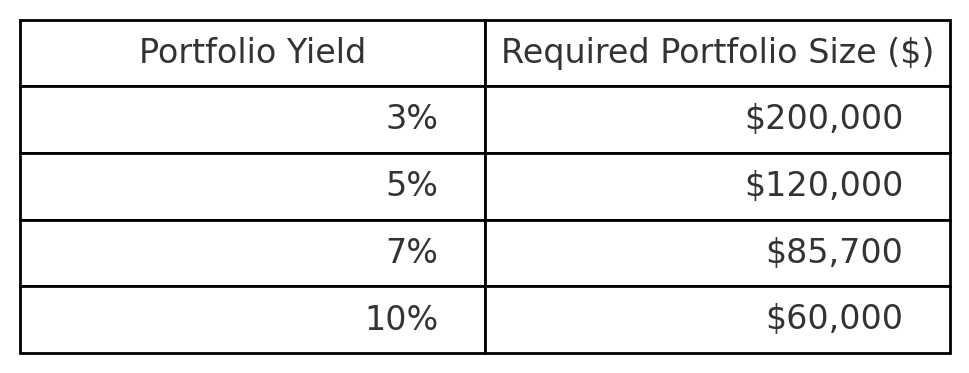

Required portfolio size = annual income goal divided by portfolio yield

Using that formula, we can calculate exactly how much capital you need at different yield levels.

For example:

At a 3% yield, you would need about $200,000 invested

At a 5% yield, you would need about $120,000

At a 7% yield, you would need about $85,700

At a 10% yield, you would need about $60,000

This is why a blended approach often works best. You can use stable blue chip holdings for the foundation and combine them with selective higher yield assets to raise your overall portfolio yield without taking reckless risks.

The key idea is simple. You do not have to reach the full $500 per month immediately. The goal is to place yourself on the path so the income grows steadily each month. Small contributions, paired with reinvestment, create powerful momentum.

Trust The Process.

What to Invest In: A Beginner’s Portfolio That Can Reach $500 Per Month

Now that you understand the math behind earning five hundred dollars per month, the next step is choosing the right investments. Beginners often make the mistake of swinging too far in one direction. Some buy only the safest blue chips and grow too slowly. Others chase high-yield assets and end up with inconsistent income.

The sweet spot is a simple two-layer structure built entirely from high-quality companies and funds. No speculative income ETFs. No risky accelerators. Just reliable assets that have proven they can pay and grow dividends through every kind of market.

This approach gives you three advantages:

It builds income that you can count on

It protects your capital during downturns

It creates dividend growth that compounds your cash flow year after year

Let’s break down the two groups.

Foundation: Durable Dividend Growers

This is the core of your portfolio. These companies and ETFs have long histories of paying and raising dividends, regardless of interest rates, recessions, or market conditions. If you subscribed, you would have received a list of high-quality dividend growers.

✅50+ Monthly Dividend Stocks provides a list of tickers that send income to your account every single month.

✅ETFs for Beginners breaks down income focused funds that simplify the investing process.

✅Dividend Legends highlights companies with long histories of increasing dividends through every type of market.

Here Are Some Examples:

Schwab U.S. Dividend Equity ETF - SCHD 0.00%↑ - A diversified ETF that contains tons of high-quality dividend companies. Low fees, reliable growth, and consistent performance. This is one of the EASIEST ways to get effortless dividend growth.

American Electric Power AEP 0.00%↑ - One of the most stable utility companies in the country. Regulated earnings, predictable cash flow, and 16 consecutive years of dividend increases.

Procter & Gamble PG 0.00%↑ - Makes consumer household goods in nearly every category. You likely purchase many of PG’s items on a monthly basis without even noticing.

For instance, here are just some of the brands that PG has in their portfolio.

Some other examples include companies like: JNJ 0.00%↑, PEP 0.00%↑, CL 0.00%↑, and WMT 0.00%↑ - These are Dividend aristocrats with decades of uninterrupted dividend increases. These companies thrive in good markets and survive in bad ones.

These are your “sleep well at night” holdings. They won’t produce explosive yield, but they raise their payouts year after year, which accelerates your long-term income growth.

👉 Beginners should make this layer roughly 60% to 70% of the portfolio for the ultimately safety.

Income Boosters: Higher Yield, Still High Quality

This is where your dividend income starts to climb. These companies and funds pay significantly higher yields than the foundation layer, while still keeping risk manageable. You are not reaching for yield here. You are selecting proven, income-efficient assets. These may not be investments that are well-known amongst investors, but I can assure you that these are great options to get a high dividend yield.

Ares Capital ARCC 0.00%↑ - The largest and most respected business development company. ARCC lends capital to other business and collects interest income in exchange. Instead of paying the credit interest, you are now receiving it. ARCC offers a 10% dividend yield. Historically stable payouts backed by strong credit quality and diversified lending.

Realty Income O 0.00%↑ - “The Monthly Dividend Company.” Decades of uninterrupted monthly payouts and built-in inflation protection through rental escalations. O lets you become a landlord without actually owning properties.

For example, here are all the tenants that O has under their umbrella. As an investor, you can collect rent from all of them!

These are just two examples that you can consider. These aren’t recommendations.

These are the positions that push your yield higher without compromising the strength of your portfolio. Combined with the foundation layer, they bring your overall blended yield into the six to eight percent range.

👉 Make this group 30% to 40% of your portfolio, depending on your risk tolerance.

How Long It Takes to Reach $500 Per Month

Now that you know what to invest in, the next question is how long this milestone actually takes. Many beginners assume they need decades, but the timeline depends on just two variables:

How much you contribute each month

Your portfolio’s blended yield

👉 With the high-quality structure we built, your blended yield will typically land between 5% and 7%. Using that range, we can map out realistic timeframes.

Here is a simplified way to think about it.

Scenario 1: You invest $250 per month

At a blended yield of 6 percent, your portfolio generates roughly $180 in new annual income every year from contributions alone. Add dividend reinvestment, and the income grows a little faster each quarter.

Timeline to reach $500 per month:

8 to 10 years

This is the most common path for beginners with limited capital. Progress starts slowly but compounds steadily.

Scenario 2: You invest $500 per month

Your annual new contributions add about $360 in dividend income at a six percent blended yield. Add organic dividend growth and reinvestments, and the timeline accelerates.

Timeline to reach $500 per month:

5 to 6 years

This is the sweet spot. Steady contributions produce meaningful income surprisingly quickly.

Scenario 3: You invest $1,000 per month

At this level, you are adding $720 in new annual dividend income each year from contributions alone. The snowball becomes noticeable within the first 12 to 18 months.

Timeline to reach $500 per month:

2.5 to 4 years

This is the path most accelerated-income investors take, especially those reallocating from low-yield assets, bonuses, or excess savings.

And Remember This

You do not need to reach the full $500 immediately. The key is momentum. Every month your income rises, even by a few dollars, you inch closer to full autonomy.

The Yieldly dashboard becomes extremely valuable here because it lets you:

Track month-by-month dividend progress

Forecast your future income

Measure how contributions change your timeline

See which holdings drive your growth

You gain visibility into the snowball that you used to only hope was growing.

While you can drastically reduce your timeline by including higher risk assets, I want to emphasize that investors should focus on sustainability and low risk factors when beginning.

Low-Risk 10% Dividend Yield From One Of The Best Option ETFs

Over the past few years, option-income ETFs have exploded in popularity. Some are designed purely for yield, others for growth, and a few attempt to deliver both. Only a handful manage to balance the two without sacrificing long-term returns.

Don’t forget about muni’s, lower yields but not taxable.

Can you please give us an idea of the rough size of the portfolio needed to generate your $50K dividend yield?