America’s Housing Problem Could Be Your Dividend Advantage

How rising costs are fueling rental demand and creating dividend opportunities for investors

I have always been fascinated by the idea of collecting real estate income through the stock market. Real Estate Investment Trusts, or REITs, allow investors to gain exposure to portfolios of properties without ever buying a building or managing a single tenant. Instead of dealing with the headaches of being a landlord, you can sit back and collect steady rent checks while waiting for market conditions to improve.

If you’re serious about building steady, predictable cash flow from dividends, this guide is the best place to start.

I’ve put together a curated, research-backed list of WEEKLY & MONTHLY paying option ETFs, designed to help you create reliable income every single month:

✅ ETFs that actually pay WEEKLY and monthly, not quarterly

✅ Estimated yields commonly above 30%. Dividend yields can be as high as 100%.

✅ My top picks for consistent income engines

✅ Includes newer, high-yield option income funds from the YieldMax suite, Roundhill, NEOS, Kurv, and Goldman Sachs

The REIT I am looking at today specializes in multifamily apartment communities across the United States. Over the past year, its share price has fallen by nearly 11%, weighed down by broad weakness in the real estate sector. Even after accounting for dividends, investors have still faced a negative total return of about 7.7%. As a result of this decline, the stock now offers a starting dividend yield of nearly 4%.

I continue to believe that the company’s data-driven strategy positions it to benefit from demographic trends and population migration into more affordable housing markets. In the sections that follow, I will take a closer look at the financials, portfolio strategy, dividend coverage, and valuation. Then, for paid subscribers, I will reveal the name and ticker of this REIT and explain why I believe it is well positioned to reward patient investors.

Financials

In its most recent quarter, this REIT reported funds from operations of $0.28 per share, a slight improvement from the prior quarter’s $0.27. That growth was modest, but it came from the right places: revenue inched higher while operating expenses moved lower. Occupancy also improved, holding essentially flat at a very high level and confirming that tenant demand across its communities remains stable.

Management also updated full year 2025 guidance. Same store revenue growth is now expected to come in between 1.5% and 1.9%, which reflects a softer leasing backdrop but still points to modest expansion. Earnings per share are projected between $1.165 and $1.185, giving investors a clearer and more realistic view of what to expect. The willingness to refine expectations rather than overpromise adds credibility to management’s approach.

On the balance sheet side, there are encouraging signs. Total debt declined to $2.24 billion, while the interest coverage ratio improved to 4.7 times, showing that the REIT is generating more than enough cash flow to meet its obligations. Cash on hand did fall to $19.4 million, but restricted cash rose slightly to $23 million, balancing out liquidity. At the same time, total gross assets grew to $6.87 billion, confirming that portfolio growth has not stalled.

Looking at the earnings, can see that net operating income slightly decreased to $100.9M, from the prior quarter's net operating income of $101.6M. However, the adjusted EBITDA remained basically flat for the quarter, now amounting to $87.55M. Despite this, total gross assets has slightly increased up to $6.87B over the last quarter, indicating overall growth of the portfolio. The REIT collects a monthly rent per unit of $1.58M, while maintaining a similar occupancy across its operating properties.

The balance sheet remains solid but the cash and equivalents have declined to $19.4M, from the prior quarter's cash and equivalents of $29M. However, the level of restricted cash has slightly increased to $23M, up from the prior quarter's restricted cash balance of $19.2M. On a more positive note, the total debt level has decreased down to $2.24B over the last quarter and the REIT still has an improved interest overage ratio of 4.7x.

Portfolio Strategy

One of the most important ways to judge a REIT is by looking at its portfolio: what types of properties it owns, where they are located, and how management is creating value over time. This REIT takes a very intentional, data-driven approach to its property mix. It invests heavily in markets that are benefiting from long-term demographic shifts, while also reinvesting in existing properties to steadily raise rents and improve profitability. The result is a portfolio that is not only resilient in the present but also positioned to grow over the next decade.

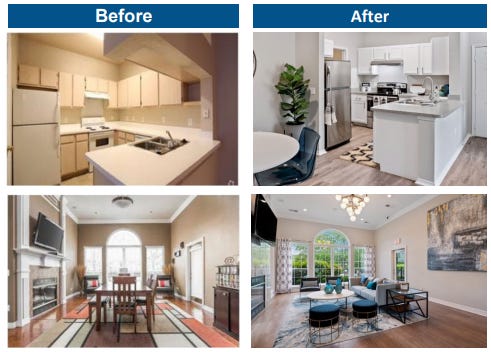

Here are some of the photos from properties within the REIT’s portfolio.

As of the latest quarter, the REIT’s portfolio consists of $6.87 billion in gross assets spread across 113 properties, representing more than 33,000 apartment units. Most of these communities are concentrated in the Sunbelt region, which continues to benefit from population growth and inbound migration. Occupancy remains consistently strong across the portfolio. The biggest driver of growth will be the population migration away from expensive regions of the country, to these more affordable areas.

Management has also made steady progress with its value-add renovation program. In the most recent quarter, 275 renovations were completed with an impressive return on investment of 16.2%. The pipeline remains substantial, with more than 5,000 additional units identified for upgrades that are expected to deliver annualized returns of roughly 16%. These improvements have already paid off at select properties: one case study from Columbus, Ohio showed revenue climbing by nearly 60% after renovations, with net operating income more than doubling since the property’s acquisition in 2018.

👉 Upgrade to a paid subscription to unlock the full report and get access to all of my high-yield income picks.

If you are ready to take these principles and build a real plan for your finances, I have two ways to help.

My Book — The Dividend Income Blueprint

This is my step-by-step guide for building a portfolio that pays you consistent monthly income for the rest of your life. It walks you through exactly how to find, buy, and manage income-producing assets so you can create financial freedom without gambling or guessing. Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

One-on-One Consulting

If you want personal guidance tailored to your situation, I offer private consulting sessions where we map out your income goals, investment strategy, and the exact steps you can take right now to start building wealth.

IRT implements a data-driven approach to its portfolio, so it continues to make investments in areas that will reward shareholders over time. According to the future pipeline of renovations, IRT has approximately 5,280 additional units that can add value once these efforts are completed. Renovation costs are estimated to be between $18,000 to $19,000 per unit and management estimates that these will have an annual return around 16.6%, based on its historical performance.

Recent acquisitions also align with the strategy of targeting high-growth regions. Notable additions include Highland Ridge in Charlotte, Serenza at Ocoee Village in Orlando, and Autumn Breeze in Indianapolis. These are markets where homeownership is becoming increasingly expensive compared to renting, which supports long-term demand for multifamily housing.

Here’s some of the results of their value-add renovations:

IRT focuses on areas that will see population increases over the next decade, due to Gen X approaching retirement age and an overall shift to the Sunbelt area as people migrate to more affordable areas. Some of its recent acquisitions include:

Highland Ridge, Charlotte, North Carolina

Serenza at Ocoee Village, Orlando, Florida

Autumn Breeze, Indianapolis, Indiana

Additionally, owning a home is becoming much more of a challenge for younger folks. Therefore, IRT is estimating that this will lead to a significant increase in people choosing to rent. Based on the median home value across the top ten markets in the US, it is 90% more expensive to own a home than it is to rent from one of IRT's properties.

Strong Dividend Coverage

One of the main appeals of investing in a REIT is the ability to earn steady rental income without ever owning a building yourself. Think about the difference. If you bought a rental property, you would need to put down a large amount of capital, take on debt, and handle all of the headaches of being a landlord, everything from maintenance calls to vacancies. With a REIT, those responsibilities disappear. You still get exposure to the same rental income, but in the form of dividends that are deposited into your account every quarter. It is one of the simplest ways to collect passive income from real estate.

As of the latest declared quarterly distribution of $0.17 per share, the current dividend yield sits around 3.9% following the continuous decline. This latest declaration also represented a dividend raise of 6.3% over its prior payout amount. As previously mentioned, FFO amounted to $0.28 per share for the quarter, which indicates that earnings support the distribution at a coverage rate of 165%. Therefore, I have no concerns about the overall sustainability of the distributions going forward.

It is worth remembering that this REIT did cut its dividend back in 2020 during the pandemic, a move that some investors may still view as a blemish. I actually see it as a sign of prudent management. Rather than risking long-term damage, the cut was made as a protective measure during a period of extreme uncertainty. Since then, the payout has been raised again, and coverage remains strong.

Investors should also be aware that dividends from REITs are typically classified as ordinary income, which means they can be taxed at higher rates than qualified dividends. For most investors the impact will be modest unless you are investing significant capital, but placing shares inside a tax-advantaged account can help mute the burden.

Attractive Valuation

Real estate has always had a close relationship with interest rates. When rates fall, property values tend to rise as borrowing becomes cheaper and investors flock to income-producing assets. When rates climb, the opposite happens: financing costs rise, valuations compress, and share prices often suffer even if the underlying properties are still performing well. This cycle is exactly what we have seen play out over the last several years. For income investors, the challenge is separating temporary headwinds caused by rates from deeper, long-term risks in the business itself.

This REIT carries $2.24 billion of total debt, which is manageable relative to its $6.87 billion asset base. The maturity schedule is favorable, with the largest single tranche not coming due until 2028. The weighted average interest rate on debt sits at 4.2%, and the company maintains an interest coverage ratio of 4.7 times, a strong signal that cash flows comfortably support obligations.

Like most real estate stocks, the share price has been sensitive to rate moves. During 2020 and 2021, when rates were cut aggressively, the stock surged. Since 2022, as rates climbed to decade highs, the shares have given back much of those gains. Importantly, this weakness appears tied more to macro conditions than to company-specific problems. The REIT currently trades at a trailing twelve-month price-to-AFFO multiple of 16.7x. This is a little higher than the sector median, but still reasonable in light of the quality of the portfolio and balance sheet. Analysts on Wall Street have an average price target of $21.39 per share, which implies potential upside of roughly 23% from current levels if market conditions improve. A rate cut from the Federal Reserve later this year could provide exactly the kind of catalyst needed to unlock that value.

The risks to keep in mind are the same ones facing the entire sector: prolonged high interest rates, elevated debt levels, and the possibility of slowing rental demand. That said, this REIT’s financial discipline, high occupancy, and long-term exposure to growing markets suggest that it is well equipped to navigate those risks better than many peers.

Conclusion

The real estate sector has been weighed down by higher interest rates, but not all REITs are created equal. The one I have covered here combines a resilient portfolio, strong financial discipline, and exposure to regions that are set to benefit from long-term demographic shifts. For income investors, it offers a way to collect steady rental income without the hassle of property ownership, while also positioning for upside once conditions improve.