Buy Alert: AST SpaceMobile's 100% Upside Potential

The tech is validated, the funding is secured, and the launch is days away. Here is my path to $180/share.

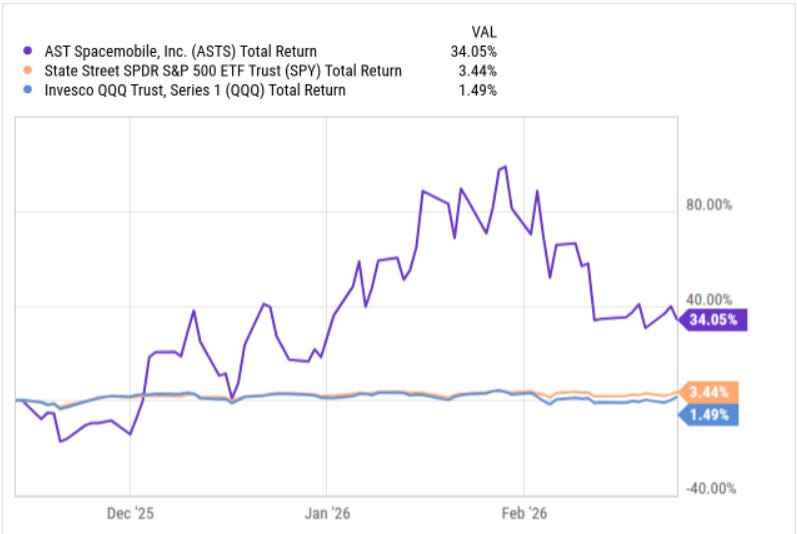

In November, I issued a buy alert for AST SpaceMobile ASTS 0.00%↑. At the time, the thesis was simple: the technology works, and the market is underpricing the monopoly potential.

Since that alert, the stock is up 34% and beating the S&P 500 and Nasdaq.

Now, I know what you are thinking: “Wait, aren’t you the dividend guy?” Yes. My core strategy is, and always will be, generating safe, growing cash flow from high-quality dividend stocks. However, a healthy portfolio needs a “Growth Engine.”

I started a small position (~$4K) and will be doubling my existing position after the release of this article. Yieldly provides us with the below summary of some bull and bear cases for the stock.

I use high-conviction growth plays like ASTS to rapidly expand my Net Liquidation Value. By driving up my total account equity, these growth positions give me significantly more margin power. This increased equity buffer allows me to execute larger income trades, like selling puts or leveraging reliable dividend payers, with a higher safety margin.

AST SpaceMobile is just a part of that engine. And right now, it is sitting on the verge of a commercial breakthrough that could fundamentally reshape the global telecommunications landscape.

What Does AST SpaceMobile Do?

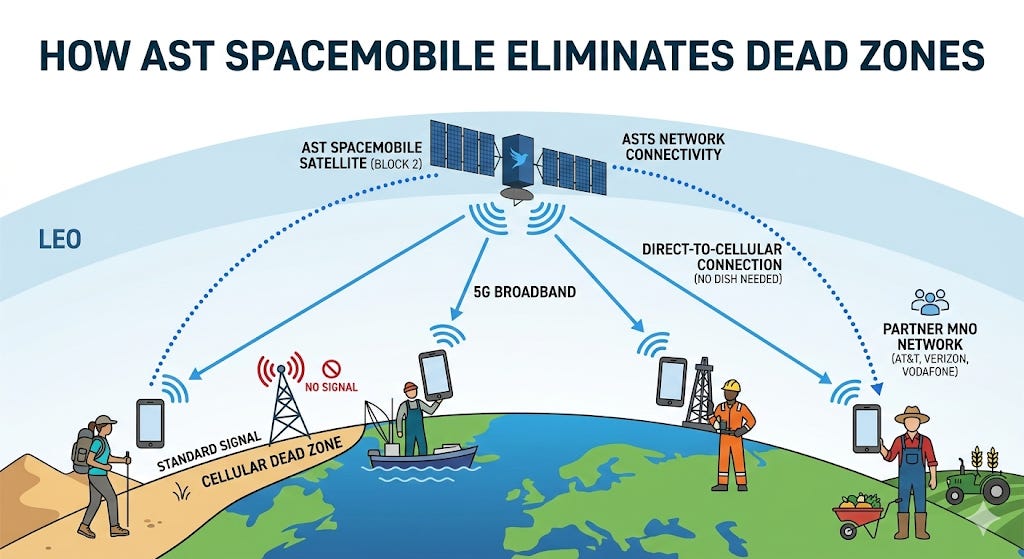

In short: AST SpaceMobile (ASTS) is building the world’s first space-based cellular broadband network that connects directly to standard smartphones.

Think of their satellites not as traditional “space hardware,” but as cell towers floating in Low Earth Orbit (LEO).

Here is the breakdown of why this is revolutionary:

No New Hardware Needed: Unlike legacy satellite phones (which require bulky antennas) or Starlink’s current residential internet (which requires a dish), AST’s network connects to the phone already in your pocket.

True Broadband Speeds: While competitors are focused on basic SOS texting, AST is building a network capable of 4G/5G speeds, meaning you can make voice calls, stream video, and browse the web from the middle of the ocean or a desert.

The Business Model (B2B2C): AST does not sell plans directly to you. Instead, they partner with major carriers like AT&T T 0.00%↑, Verizon VZ 0.00%↑, and Vodafone. I believe that these carriers will eventually offer “SpaceMobile” as a premium add-on or an automatic “roaming” feature when you leave terrestrial coverage.

The Gap Filler: Their goal is to eliminate dead zones entirely. If you lose signal from a ground tower, your phone seamlessly switches to a satellite signal, keeping you connected everywhere.

Why it matters right now: They have validated the technology (making the first 5G call from space) and are currently launching their commercial “BlueBird” satellites to turn this concept into a globally available service.

The Core Thesis: The “Dead Zone” Killer

The reason I am bullish on ASTS comes down to one thing: It just works.

Right now, if you want satellite internet from Starlink, you have to buy a $500 dish and lug it around. If you want satellite texting from Apple, you need the newest iPhone, and it only works for SOS emergencies.

AST SpaceMobile is different. It connects directly to the standard smartphone already in your pocket. No special apps, no hardware upgrades, no satellite dishes. Your phone just thinks it is connecting to a regular cell tower—except that tower happens to be floating 300 miles above your head.

The Business Model is Genius Most space startups fail because acquiring customers is expensive. ASTS skipped that problem entirely.

They aren’t trying to compete with AT&T or Verizon; they are partnering with them.

By operating as a B2B2C partner, ASTS instantly gains access to the 3 billion customers these telecom giants already have. The deal is simple: AT&T and Verizon handle the customer service and billing, ASTS provides the space signal, and they split the revenue 50/50.

It’s a high-margin model with zero customer acquisition costs. They don’t have to convince you to sign up; they just have to keep the signal on.

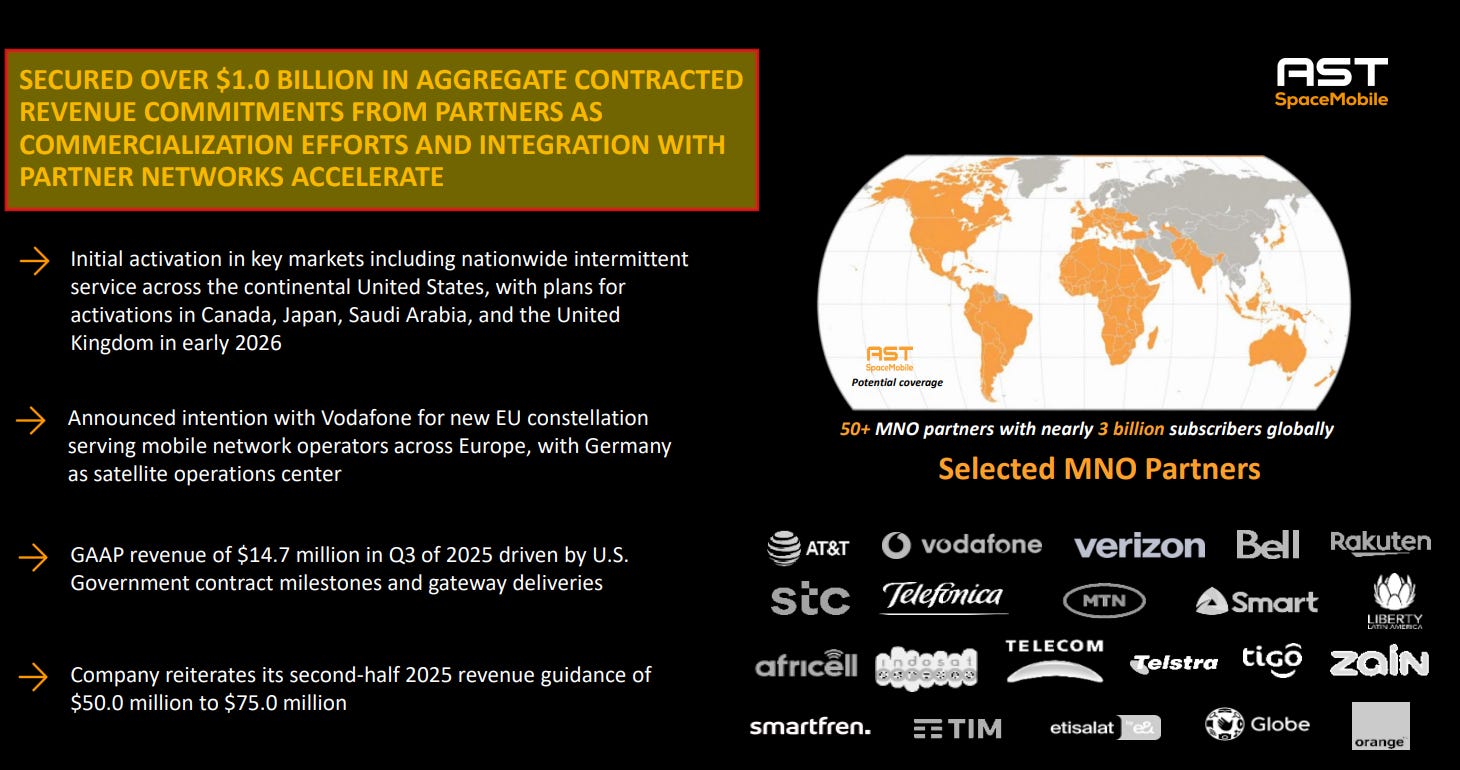

The commercial validation here is undeniable. As seen above, they have already secured over $1 billion in contracted revenue commitments, including significant prepayments that fuel their growth without diluting shareholders unnecessarily.

👉 Upgrade To A Paid Membership To Get Access To The Entire Analysis.

Valuation: I Think It’s Worth $180 (100% Upside)

Valuing a pre-revenue disruptor is difficult, but the unit economics allow for a clear “napkin math” projection for the end of the decade.

There are millions of people in the U.S. alone who are stuck in digital darkness. According to the FCC, roughly 12% of the rural population has internet speeds so slow they can barely load a webpage. And this is only in the US - when you think about it on a global scale, there is so much potential.

The Bull Case Model: