Buy Alert: 2 Undervalued Growth Stocks for 2026 ($NFLX & $BE)

Why I'm betting on the "Merger Arbitrage" in Netflix and the "AI Power" gap in Bloom Energy. My top contrarian picks for the new year

I know what you are thinking. “Why is the income investor buying a streaming giant and a volatile clean energy stock?”

It is a fair question. My strategy is built on cash flow. But I have learned that a portfolio blinded by yield is a portfolio destined to lose against inflation or capital erosion. To keep our passive income growing for decades, we need an engine that runs hotter than just a high yield. We need Capital Appreciation to do the heavy lifting so our Dividends can do the steady lifting.

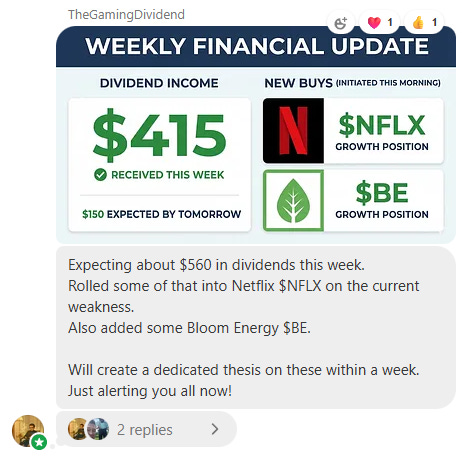

This week, I deployed significant capital into two “contrarian” positions:

Netflix ($NFLX): A household name Wall Street has labeled “dead money.”

Bloom Energy ($BE): A volatile energy player tackling the AI power crisis.

On the surface, they look like risks. Under the hood, they are mispriced opportunities.

Paid Subscribers are instantly alerted to my buys and sells.

You can join now with a limited time discount.

1. Netflix NFLX 0.00%↑: The Merger Arbitrage & Game Theory Play

Current Price: ~$95

Drawdown: ~30% from Highs

The narrative on Netflix has shifted overnight. Following the uncertainty of its potential merger with Warner Brothers Discovery WBD 0.00%↑ and a looming hostile counter-bid from Paramount, the stock has shed 30%. The markets call this “uncertainty.”

I call it a perfect setup for accumulation.

The Thesis: Heads I Win, Tails You Lose

When you map out the probabilities of this M&A drama, Netflix sits in a position of extreme strength in almost every scenario.

Scenario A: The Acquisition Closes (The “Content King” Outcome)

If Netflix secures WBD, they acquire the crown jewels of prestige TV (HBO, Game of Thrones, Succession, DC Universe, Harry Potter, etc.). This creates a perfect “Barbell Content Strategy”: Netflix dominates volume, HBO dominates prestige.

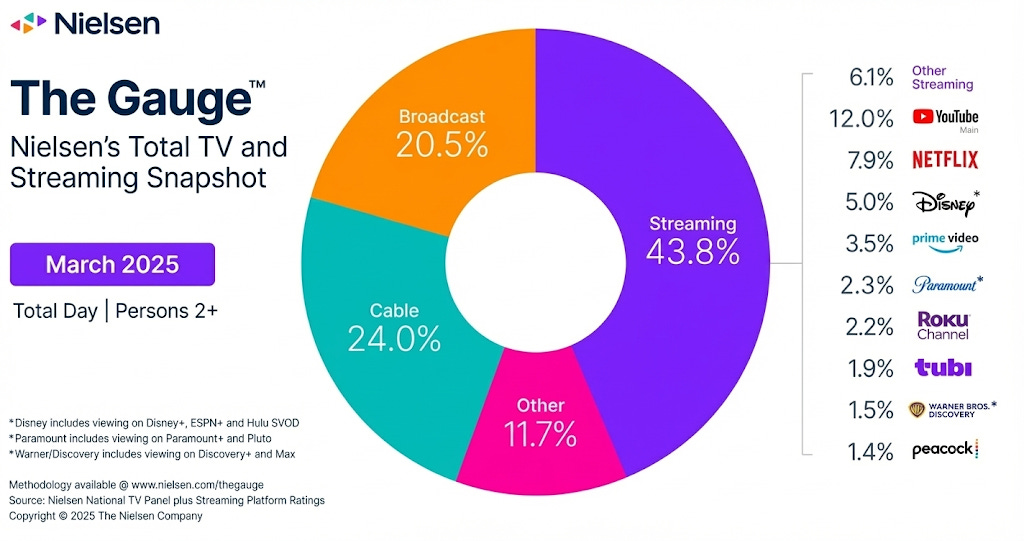

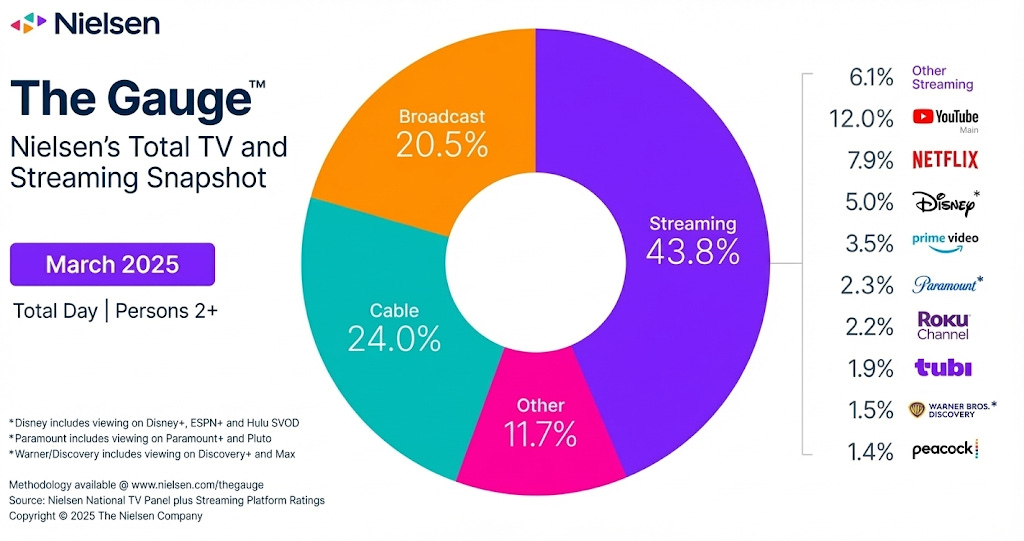

The “Monopoly” Defense: Bears claim regulators will block this. However, data shows that even combined, Netflix + WBD would trail YouTube in total TV watch time (approx. 9% vs 13%). It is hard to block a merger when the combined entity is fighting for second place.

Scenario B: The “Kill Fee” Payout (The Cash Injection) If Paramount—backed by deep-pocketed external funding—swoops in to “steal” WBD, they trigger a massive “no-shop” breakup fee.

The Math: WBD would likely owe Netflix an estimated $2.8 billion. In this scenario, a competitor writes Netflix a check for nearly $3 billion to go away. Netflix strengthens its balance sheet for free, while a rival over-leverages themselves to win a trophy asset.

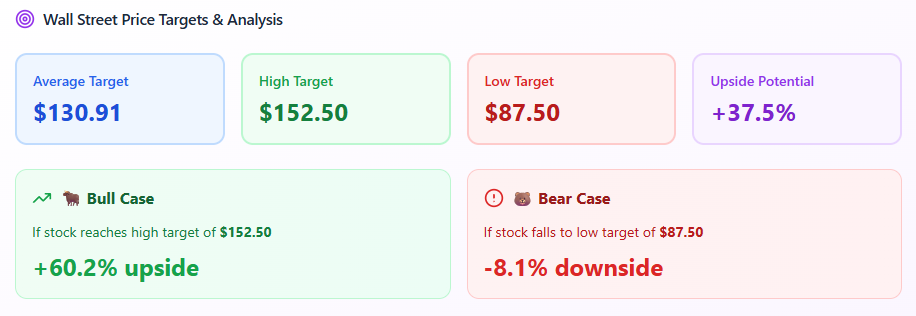

My Verdict: Buying a cash-flow machine like Netflix at a 30% discount—where the “worst case” is a multi-billion dollar breakup fee—is a risk I am willing to take. As we can see below, the Yieldly Dashboard estimates that NFLX has a potential upside of more than 60% from its current level.

2. Bloom Energy BE 0.00%↑: The “Time-to-Power” AI Play

Sector: Clean Energy / AI Infrastructure

The Hook: The Physical Bottleneck of AI

If Netflix is the strategic play, Bloom Energy is the Macro Play. We talk about AI chips NVDA 0.00%↑ and software MSFT 0.00%↑, but we ignore the physical bottleneck threatening the industry: Electricity.

The Thesis: The Grid is Broken

Data centers are voracious energy hogs. Goldman Sachs estimates AI could consume 8-12% of total US power by 2030.

The problem? The US power grid operates on a timeline of decades. You cannot just “plug in” a gigawatt-scale data center today.

Bloom Energy solves the one variable Big Tech cares about most: Time.

The “Time-to-Power” Moat: Bloom’s solid oxide fuel cells act as on-site power plants. They allow data centers to bypass the utility grid entirely and generate their own clean electricity now, not in 5 years.

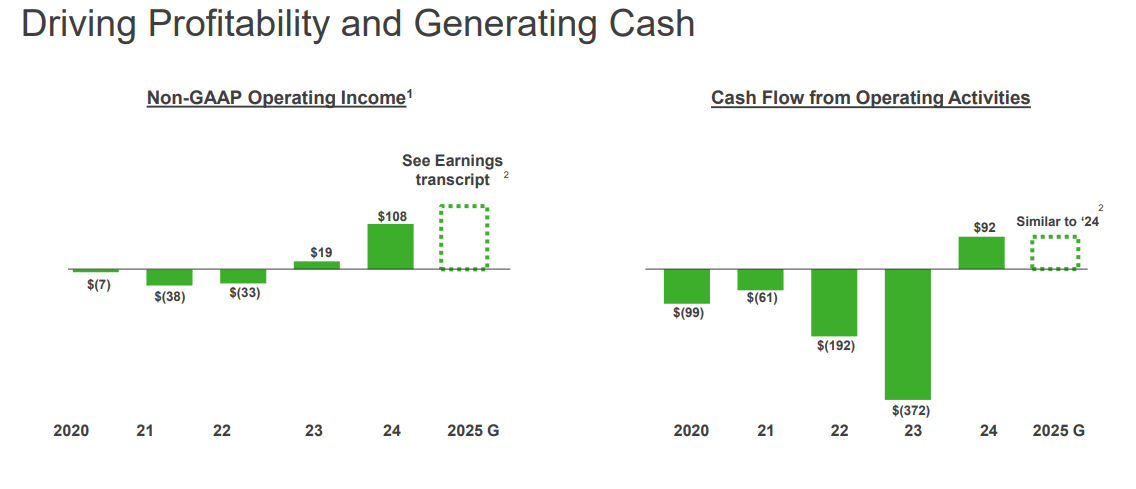

The Pivot to Profit: For years, Bloom was a “growth at all costs” cash burner. That has flipped. In the most recent quarter, they grew revenue by 57% YoY and swung to positive operating income. The business is maturing exactly as demand explodes.

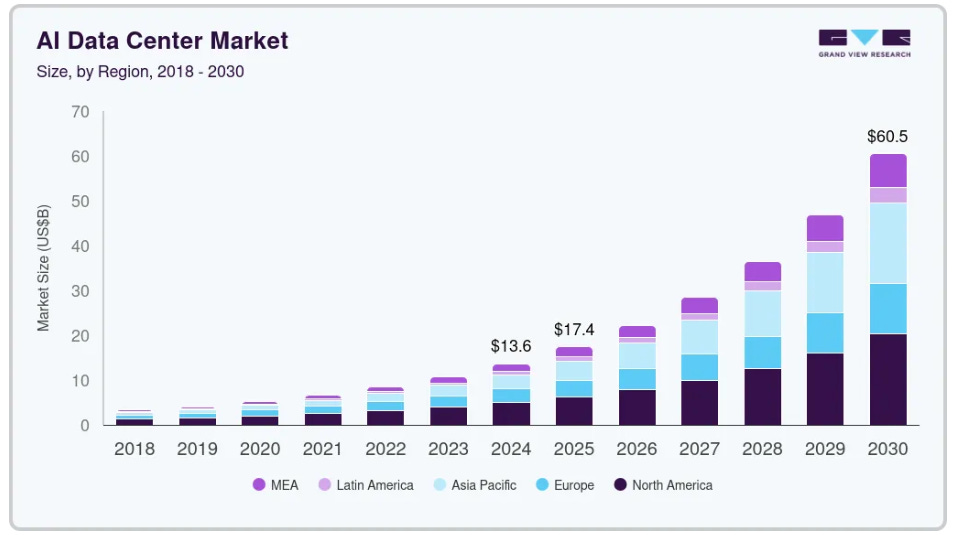

Additionally, the size of the AI Data Center market is estimated to increase at a CAGR (compound annual growth rate) of 28.3% through 2030. I think that Bloom Energy is perfectly aligned to benefit from this growth.

My Verdict: This is a high-beta (volatile) stock. But it serves a specific role: massive growth potential.

Summary

I am not abandoning dividends—I am strictly protecting them.

By using the steady cash flow from my dividend payers to fund high-conviction growth plays like Netflix and Bloom Energy, I am strictly adhering to a “Barbell Strategy”:

Left Side (Income): High-yield Dividend stocks covering daily bills and creating cash flow within the portfolio.

Right Side (Growth): High-conviction compounders ($NFLX, $BE) fighting inflation.

I will be tracking these positions closely in the coming months. If you need help choosing high quality income positions, I laid out the structure and 3 picks in the linked article below.

Or, you can get the dividend starter bundle so that you can skip the mistakes that I made.

👉 Here is what’s included:

✅ The Dividend Blueprint (PDF)

A step-by-step guide showing how I structure my portfolio, grow monthly cash flow, and reinvest for long-term income.✅ Monthly Dividend Map

50+ hand-picked tickers that pay monthly so you can ladder your income all year long.✅ Dividend Tracker (Google Sheet)

The exact spreadsheet I use to track yield, forward income, reinvestment, and portfolio growth.✅ Dividend Growth Legends: 50+ Stocks - Free eGuide

50 stocks that have an established history of dividend increases.✅ List of ETFs for Beginners To Start With

How to Build a $1,000/Month "Forever Paycheck" (Without Yield Traps)

In the hunt for passive income, it is easy to get seduced by triple-digit yields. But as we head into 2026, the market environment is shifting, and a 50% yield is meaningless if your principal is eroding by 40%.

Interesting to read the thoughts of other folks discovering Bloom. If anyone is interested in a deeper dive about them from someone who has followed them for a while as an amateur -

https://outspokengeek.substack.com/p/the-implausible-bloom-of-an-energy