Deep Dive: Microsoft Is Extremely Undervalued

Why Microsoft’s massive CapEx spend is actually the ultimate growth moat.

The financial media is currently paralyzed by the “SaaSpocalypse.” Headlines are dominated by the fear that autonomous AI agents, like Anthropic’s Claude Cowork and OpenClaw, will completely upend traditional enterprise software. The narrative suggests that legacy SaaS moats are dead, sparking a brutal sector-wide sell-off that has dragged the undisputed king of software down with it.

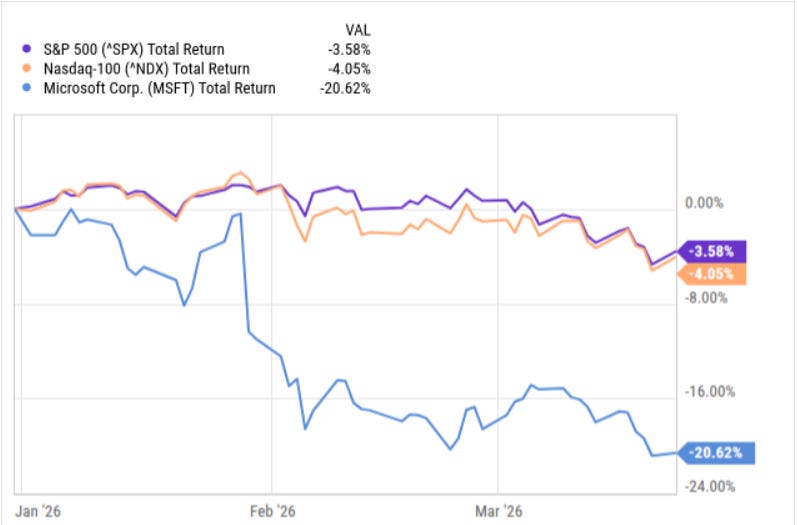

On a YTD basis, both the S&P 500 SPY 0.00%↑ and the Nasdaq-100 QQQ 0.00%↑ are down. However, Microsoft MSFT 0.00%↑ is down more than 20%.

But panic creates profound mispricing.

While the market hyper-focuses on short-term margin compression and infrastructure costs, they are completely misjudging Microsoft’s aggressive transition into the agentic AI era. Microsoft is not being disrupted by artificial intelligence; it is building the foundational compute layer that will power it.

Here is the deep-dive, fundamental analysis into why Microsoft is currently the most compelling growth equity in the market today, offering double-digit top-line expansion at a highly compressed valuation.

Disclaimer: This should not be interpreted as investment advice. I am sharing the results of my analysis.

The Growth Engine: Monetizing the “Agentic” Shift

The core bear argument against Microsoft right now centers on “ROI Compression”, which is the fear that the company is accelerating its capital expenditures without seeing a corresponding, immediate uplift in Azure revenue. Analysts are terrified that the shift toward autonomous AI agents will disrupt Microsoft’s legacy, seat-based subscription model.

Just for reference, here is how much capital the tech leaders are allocating towards capex spend through 2026:

Amazon AMZN 0.00%↑: $200B

Alphabet GOOG 0.00%↑: $175B - $185B

Microsoft: $140B

Meta Platforms META 0.00%↑: $115B-$135B

However, the data proves the exact opposite. Microsoft is actively monetizing this shift through unparalleled pricing power and deep enterprise penetration.

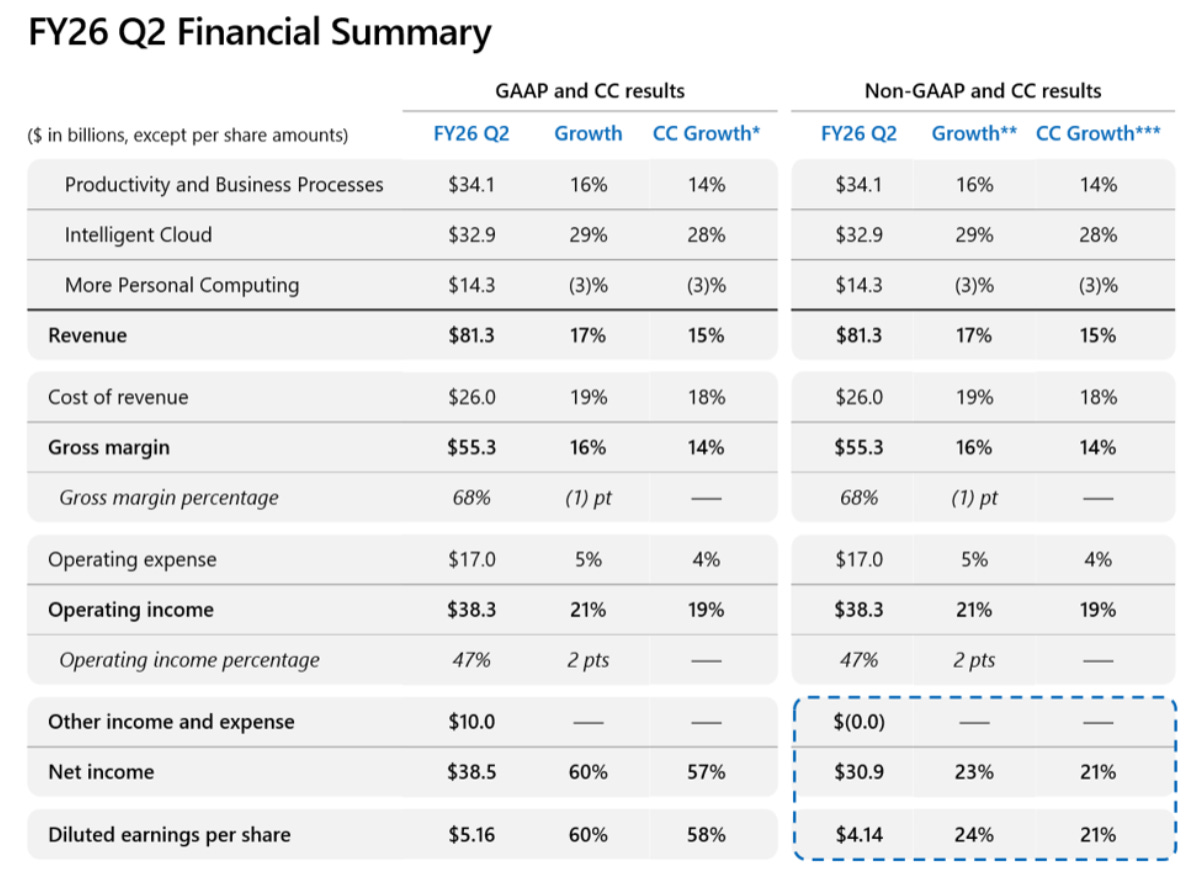

During the FY26 Q2 earnings update, Microsoft reported $81.3 billion in revenue, a 17% year-over-year increase, and an astounding $38.3 billion in operating income. The true growth vector lies in their ability to upsell their captive audience:

The Massive M365 Runway: Microsoft currently boasts over 450 million paid commercial seats for Microsoft 365.

The Copilot Conversion: As of Q2, paid Copilot seats reached just 15 million. While that represents a massive 160% year-over-year growth, it means Copilot has only penetrated 3.3% of their existing M365 user base. The runway for internal upselling is staggering. Furthermore, massive enterprise deployments of more than 35,000 Copilot seats tripled year-over-year, proving that adoption is accelerating at the institutional level.’

The ultimate proof of Microsoft’s growth trajectory arrives this May with the rollout of the M365 “E7” tier, dubbed The Frontier Suite. By bundling Copilot, Agent 365, and premium E5 security features, Microsoft is pricing this new tier at $99 per user, per month.

This is a massive 65% pricing step-up from the mission-critical E5 tier. CEO Satya Nadella is explicitly rejecting the unpredictable pure consumption model in favor of a highly predictable, hybrid seat-based model that secures massive, recurring revenue expansion.

The $37.5 Billion Reality: CapEx Is The Ultimate Moat

To accurately value Microsoft’s growth potential, we must directly address the bear case. Microsoft’s Q2 CapEx hit $37.5 billion, a nearly 50% year-over-year increase, driven heavily by GPU/CPU procurement and data center construction. Memory price hikes for NAND flash and LPDDR added an estimated $1.8 billion per one-gigawatt data center deployment.