Dividend Investing for Beginners: How to Get the Snowball Rolling

Learn how to start your dividend snowball, reinvest smarter, and grow small payouts into lasting monthly income.

With a bunch of new subscribers joining recently, I figured it would be great to take it back to the basics. The US government is on shut down, market indexes are trading near all time highs, and interest rates are starting to get cut. So what can you do to start building your dividends and how should you invest?

The dividend snowball is one of the most powerful forces in personal finance. At first, it feels slow and even frustrating. You might only collect a few dollars in dividends and wonder if it is even worth the effort. But just like rolling a snowball down a hill, what starts small can eventually build unstoppable momentum. The key is understanding how to get the snowball moving, how to keep it rolling, and how to make it bigger with every turn.

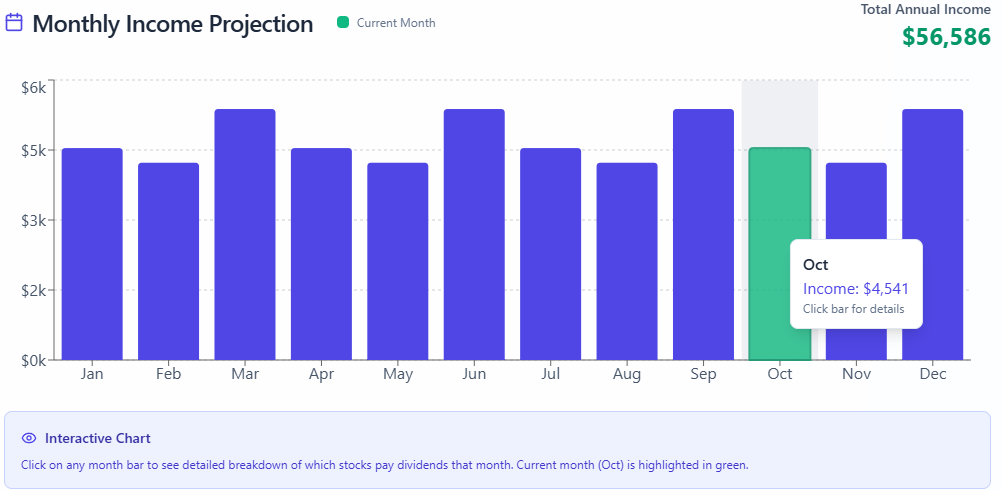

It took me 5 years to build a sizeable dividend income.

👉 My 2020 Dividend Income: $1,632.94

👉 My Estimated 2026 Dividend Income: ~$56,000

(Estimate according to Yieldly)

Why the First Dividends Matter

The early stages are the hardest because the income looks tiny. Your first dividend payment may only be $10 or $20. For many people, this does not feel life changing. But what matters is not the size of the check; it is the realization that your money is working without you.

Imagine holding shares of Coca-Cola KO 0.00%↑. You drink a Coke on a hot day, and at the same time, the company is sending you a portion of its profits. Or think about owning Realty Income O 0.00%↑, a REIT that calls itself “The Monthly Dividend Company.” Every month, like clockwork, that dividend arrives whether the market is up, down, or sideways. That moment, when you realize dividends show up regardless of your daily work, is the spark that starts the snowball.

When I hit $100 per month in dividends, something clicked for me. It no longer felt like a hobby or an abstract idea. It felt real. That $100 could pay my phone bill or cover my groceries. From there, it was easy to imagine $200, $500, or $1,000 per month. The snowball had started rolling.

Here’s The Portfolio Structure To Create Rapid Growth

The snowball grows fastest when you stop thinking of your portfolio as a random collection of tickers and start seeing it as an income engine. Every position has a role to play. At the base, you need stable holdings that you can count on through any market cycle.

Do me a favor. Look around you. Observe what products you have scattered throughout your home. What sort of device are you reaching this article on?

I bet that you have some of the following companies around you at this very moment:

Procter & Gamble PG 0.00%↑

Johnson & Johnson JNJ 0.00%↑

Walmart WMT 0.00%↑

Apple AAPL 0.00%↑

Microsoft MSFT 0.00%↑

Colgate CL 0.00%↑

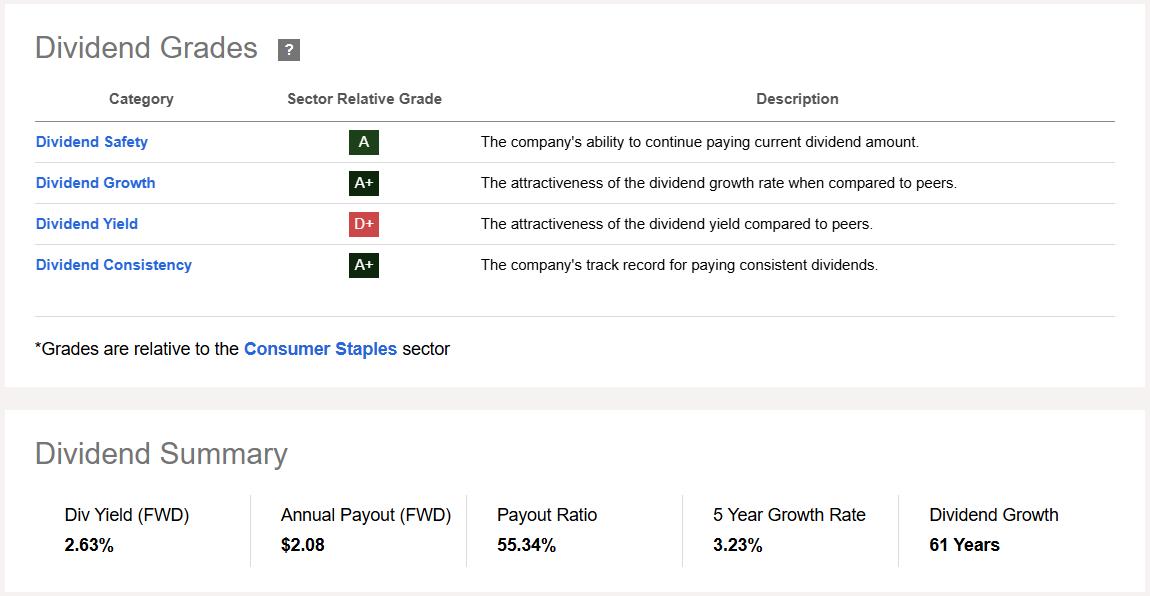

These investments do not have the highest yields, but they build the reliable foundation of cash flow. These sort of investments will be your foundation. These are the positions to hold forever with no intention of selling. These are companies that have a history of providing dividend raises over time.

For example, Colgate has a history of raising dividends for 61 consecutive years without interruption. How many consecutive annual raises has your job given you? So while you are only collect a 2.6% yield from Colgate, you are letting the company contribute to your growing dividend snowball through raises.

After The Foundation

On top of that, you can add holdings that provide more yield but come with a little more risk. Business Development Companies such as Ares Capital ARCC 0.00%↑ or Blackstone Secured Lending BXSL 0.00%↑ regularly yield 9% to 11% and pay monthly or quarterly. They boost your overall income, but they also require more attention to coverage ratios and credit quality.

These are companies that lend capital to business and collect equity or interest in return.

These sort of assets puts you on the other side of the cash register. Instead of paying the interest and being the borrower, you are now collecting the interest and acting as the lender.

These are powerful because they enable investors to collect a large amount of annual income with less capital invested. For instance, My $10,000 investment in ARCC is paying me more than $1,000 annually.

👉 Get a 10% pre-launch discount on the Yieldly dashboard, forever! Offer ends on October 15th. Yieldly is launching on October 30th.

The Amplifiers

Finally, you can layer in tactical enhancers. These include option-income ETFs like JPMorgan Equity Premium Income JEPI 0.00%↑ or funds like Global X NASDAQ 100 Covered Call QYLD 0.00%↑. These positions can increase monthly income significantly, but they also cap your long-term growth. Used selectively, they give you the extra horsepower that speeds up the snowball.

When these three layers are working together, you are not just collecting dividends randomly. You are operating a well-tuned machine designed to produce more cash flow every year.

Warning: building this portion of your portfolio too early can lead to underperformance. These higher yielding assets typically erode in value over time.

There's A New Weekly Paying ETF With A 48% Dividend Yield

Most investors underestimate just how important the timing of cash flow really is.

Reinvestment Is the Accelerator

Once the dividends start flowing, the question is what you do with them. If you spend them all immediately, the snowball rolls slowly. If you reinvest them, the effect compounds. Remember we are building the snow ball. We can’t build that snowball if you are spending the dividends right away.

In the beginning, automatic dividend reinvestment plans (DRIPs) are a good tool because they keep the process simple and consistent. Over time, however, you will want to take a more active role.

For example, if PepsiCo PEP 0.00%↑ is trading near all-time highs while Intel INTC 0.00%↑ is undervalued, why would you automatically reinvest into Pepsi at a premium? A better move is to manually direct your dividends into Intel or another holding where the valuation is attractive and the yield is higher. By doing this, every dollar you reinvest is working harder, and the snowball gains more size with each turn.

This strategy is even more powerful when combined with consistent new contributions. Imagine investing $500 a month while also reinvesting $200 in dividends. In a year, you are adding $8,400 in fresh capital.

$500 x 12 months = $6,000

$200 x 12 months = $2,400

Total $8,000

If that portfolio yields 6%, you are now generating an additional $500 in annual income without even considering dividend growth or reinvestment gains. That is how the snowball accelerates.

Treat the Portfolio Like a Business

Many investors fail to see progress because they do not track their results. If you ran a small business, you would know your revenue, expenses, and profits. Treat your dividend portfolio the same way. Track exactly how much income you are generating each month and which holdings are contributing the most.

When I began doing this, I realized some holdings were pulling far more weight than others. My investment in Main Street Capital MAIN 0.00%↑, for example, contributed more monthly income than several of my lower-yielding stocks combined. That told me where to allocate future capital. Tracking also helped me spot risks early. If a fund’s net asset value (NAV) kept eroding, I knew I needed to reconsider my position.

Your goal is not to beat the S&P 500. Your goal is to beat your bills. Measuring success in monthly income, not in account size, keeps you focused on building cash flow that matters in your daily life.

This is exactly why I designed Yieldly for investors that want to track their dividends closely.

Discounted Annual Plan

✅ 10% off forever, even through future price increases – Lock in a discounted subscription rate. Exclusive access to all articles, buy & sell alerts, dividend income reports, occasional portfolio updates, and more.

3-Month Access + High-Yield Guide

✅ High-Yield Option ETF Guide + 3 months paid access – Your starting point for building predictable monthly income. 30+ different high-yield funds included.

Staying Disciplined Through Temptation

The dividend snowball is built on consistency, not hype. There will always be distractions. During the GameStop frenzy, people doubled their money overnight. During crypto booms, coins that started as jokes were up 1,000%. If you are serious about dividend investing, you have to block out that noise. The snowball only grows if you keep rolling it. That means staying invested, reinvesting consistently, and resisting the urge to gamble on the next hot trade.

It also means accepting that progress feels slow at first. Going from $50 to $100 in monthly dividends takes time. But the jump from $1,000 to $2,000 happens faster because of compounding. The investors who stick to the plan and stay disciplined are the ones who eventually reach financial independence.

Real Dividend Snowball Case Studies

The theory is one thing, but the most powerful way to understand the dividend snowball is by seeing how it works in real-world examples. Below are three case studies that show how the snowball grows depending on your starting point, contributions, and time horizon.

I will now present three different case studies for three different investors at different ages.

Case Study 1: Brianna — Starting With $5,000

Brianna is 28 years old and works in healthcare. She makes $58,000 a year and is able to invest $300 per month. Her initial goal is to build enough dividend income to cover her $125 monthly student loan payment.

She begins with $5,000 invested and targets a blended yield of about 6.5%. Her portfolio is anchored by the Schwab U.S. Dividend Equity ETF (SCHD), which provides stability and dividend growth. She also owns Realty Income (O), which pays monthly distributions backed by real estate. To boost her yield further, she adds Blackstone Secured Lending (BXSL), a business development company, and Global X NASDAQ 100 Covered Call (QYLD), which generates cash flow through option premiums.

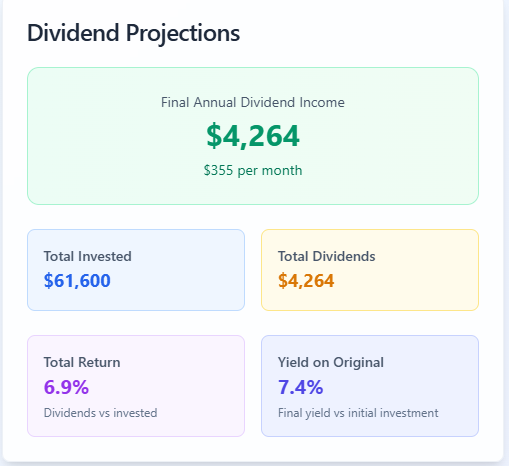

After her first year, Brianna is collecting around $100 per month in dividends. By month 16, her portfolio produces enough income to completely cover her student loan bill. The money is meaningful, but the real win is psychological. Her portfolio has turned into an engine that pays actual bills.

Using Yieldly’s built in calculator shows us the following snapshot:

Case Study 2: Mike — Scaling a $50,000 Portfolio

Mike is 45 years old and works in the tech industry, earning $150,000 annually. He starts with $50,000 invested and adds $1,000 each month. His goal is to generate $1,500 in monthly dividend income within five years so he can scale back from his W-2 job.

Mike’s portfolio has three layers. The core is made up of SCHD, JPMorgan Equity Premium Income ETF (JEPI), and BXSL, which provide steady income and resilience. The second layer includes yield boosters such as QYLD, Cohen & Steers REIT and Preferred Income Fund (RNP), and Annaly Capital (NLY). Finally, Mike uses tactical enhancements by selling covered calls on SCHD and cash-secured puts on Microsoft (MSFT) to add premium income.

After two years, Mike’s portfolio is producing about $400 per month. By year four, his income grows to $1,100. At the five-year mark, he passes his $1,500 goal, enough to meaningfully offset his living expenses and give him the freedom to reduce his hours at work.

Case Study 3: Lisa — The Late Starter With $100K

Lisa is 58 and was recently laid off. She has $100,000 in savings and needs to create income right away to supplement Social Security. Her target is $800 per month.

She invests 30% of her capital into JEPI for consistent monthly income and 20% into Realty Income (O) for dependable REIT exposure. Another 20% goes into BXSL to add high-yield floating-rate lending. To diversify further, she invests 15% in RNP, which provides exposure to real assets through a closed-end fund. The remaining 15% she holds in cash, where she sells 30-day cash-secured puts on ETFs she is comfortable owning.

Within ten months, Lisa is consistently generating between $750 and $780 each month. By reinvesting part of her excess income and trimming one underperforming fund, she crosses the $800 monthly income mark within her first year.

Key Takeaway

Whether you are starting with $5,000 or $100,000, the dividend snowball works the same way. The speed of growth is different, but the principle is identical: consistent contributions, reinvestment of dividends, and a portfolio structured to generate cash flow.

The earlier you begin, the more powerful compounding becomes. But even late starters can build meaningful results quickly when they focus on income first.

Thanks for the case studies!

Great post, Gaming!!