Everyone Is Wrong About Amazon (And The Tariffs)

Here is why I am buying the "Capex Fear" dip and the hidden $100B asset on Amazon's balance sheet.

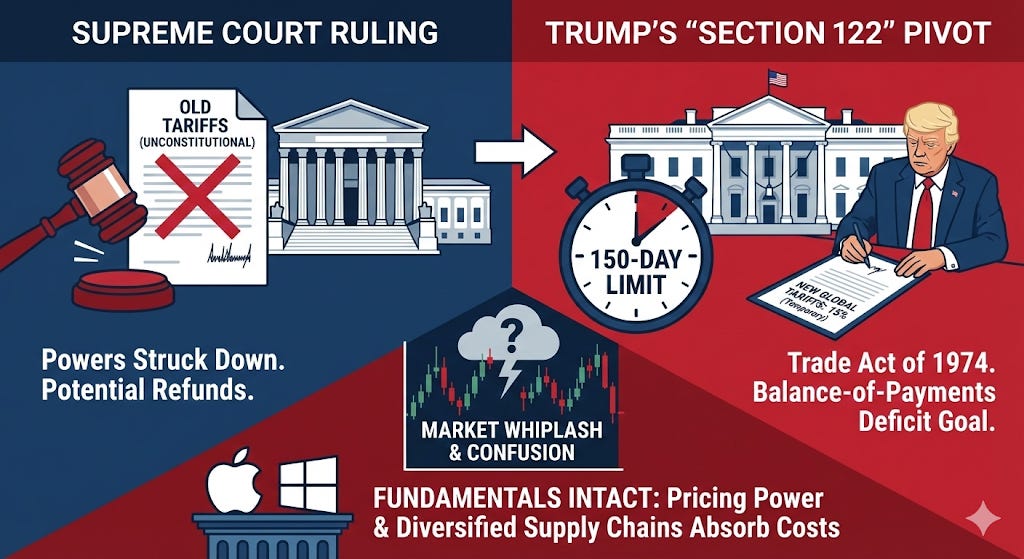

Uncertainty is back on Wall Street. Following a Supreme Court ruling that struck down previous tariff measures, President Trump has doubled down, announcing an intensified 15% global tariff strategy that has rattled equity and crypto markets alike.

As the political landscape shifts, the divergence between companies that can generate cash and those spending it all on AI infrastructure is becoming the most critical metric for investors.

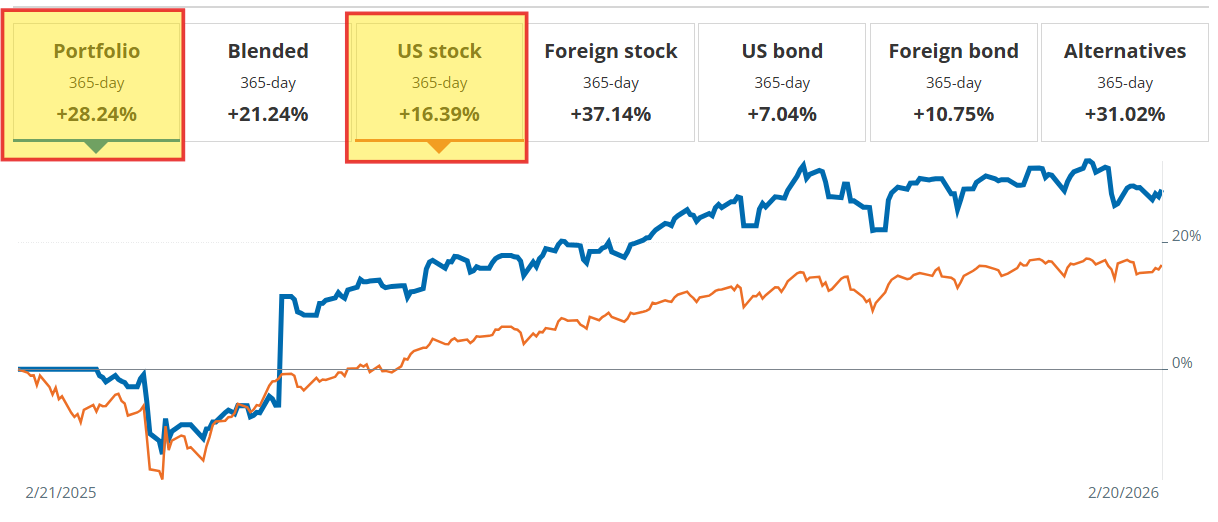

However, we capitalize on these periods of volatility. Remember, markets tend to react dramatically to both upside and downside catalysts. By adding during periods of uncertainty is how we’ve been able to outperform the indices. As we can see below, the dividend portfolio has outperformed the US stock market over the last twelve months.

👉 Upgrade To A Paid Membership To Get Access To Buy Alerts

Here is what you need to know about the current market drift, why the fundamentals of top US companies remain strong, and where to find safety (and hidden value) in the “Magnificent Seven.”

Quick Takeaways: The 30-Second Brief

The “Tariff Shock” is Temporary: President Trump’s new 15% global tariff is being deployed via “Section 122,” which has a strict 150-day limit. This is a medium-term dislocation, not a permanent structural change.

The “Safe Haven” Trade: Amidst the AI spending spree, Microsoft (MSFT) is the only hyperscaler projected to actually increase free cash flow in 2026. If you want safety, this is the play.

The Contrarian Opportunity: The market is punishing Amazon (AMZN) for its massive capex spend, but they are missing a “hidden” $100B asset on the balance sheet. (Full analysis below).

Actionable Strategy: We are shifting to a “Barbell Strategy”—buying domestic-focused sectors (Utilities, Regional Banks) to hide from tariffs, while accumulating specific tech giants on the dip.

The Situation: Tariff Whiplash

Wall Street opened lower on Monday as investors grappled with renewed volatility. The immediate catalyst was President Trump’s announcement on Saturday that he will increase his newly proposed global tariff level to 15% from 10%.

This move comes less than 24 hours after the Supreme Court struck down most of the tariffs imposed last year, ruling that the use of emergency powers to enact them was unconstitutional. In response, the administration is pivoting to Section 122 of the Trade Act of 1974, a rarely used provision that allows for temporary tariffs to address balance-of-payments deficits.

Why This Is Happening (And Why It Is Not a Crisis): The administration is using Section 122 to impose these duties for a maximum of 150 days. The stated goal is to correct the US balance of payments deficit. While the headline number of 15% sounds dramatic, it is crucial to understand the context.

It is Temporary: Unlike previous trade wars that dragged on for years with no end date, Section 122 has a hard time limit of 5 months unless Congress intervenes.

Fundamentals Are Intact: A 150-day tariff surcharge creates a headache for supply chains, but it does not destroy the business model of a company like Microsoft or Apple. These companies have massive pricing power and diversified supply chains that allow them to absorb or pass on these costs without derailing their long-term growth.

The “Refund” Chaos: A major source of market confusion right now is not just the new tariff, but the legal battle over whether the government must refund billions in old tariffs that the Supreme Court declared illegal. This creates short-term noise, but for the companies themselves, a potential refund would actually be a massive windfall of cash.

The “Safe Haven” Play: Microsoft’s Cash Flow Advantage

While the macro picture is cloudy, a clear signal is emerging within the tech sector. The “AI capex splurge” is real, and it is eating into the free cash flow (FCF) of almost every major tech giant, except one.

According to a new note from Evercore ISI, Microsoft MSFT 0.00%↑ stands out as the only hyperscaler in the Magnificent Seven expected to increase its free cash flow in 2026.

The Spenders: Amazon AMZN 0.00%↑, Google GOOG 0.00%↑, and Meta Platforms META 0.00%↑ are all expected to see year-over-year declines in FCF in 2026 as they pour money into data centers.

The Exception: Microsoft is projected to grow FCF by 5%.

For conservative investors, Microsoft represents the “safe” play: a company that is aggressively building AI infrastructure but still managing to grow its pile of cash.

Why Everyone Is Wrong About Amazon

While Evercore warns about Amazon’s declining free cash flow due to massive spending, other smart money investors are aggressively buying the dip.

Here is the contrarian bullish case:

1. Capex is “Offense,” Not “Defense”

Unlike some peers who are spending just to keep up, Amazon’s spend is demand-driven. They currently have a $240 billion demand pipeline (up 22% quarter-over-quarter). They are building data centers because customers are already lined up to rent them.

Amazon is now my largest position and I will be adding more. I will updated paid subs when I add more.

👉 Upgrade To A Paid Membership To Get Access To Buy Alerts

Keep reading with a 7-day free trial

Subscribe to Dividendomics to keep reading this post and get 7 days of free access to the full post archives.