Exclusive Analysis: ASML Holdings - Will Benefit From AI Growth

I plan to accumulate at least $10,000 worth of ASML because...

This analysis is exclusively for premium subscribers. Free subs can get a small glimpse into the analysis.

Executive Summary

ASML Holding (ASML) remains one of the most strategically vital companies in the semiconductor supply chain. It dominates the global market for photolithography systems and especially EUV (extreme ultraviolet) technology. These are essential to the production of advanced semiconductors. Despite recent underperformance in its stock price and market unease over forward bookings, the long-term demand for ASML’s equipment remains intact, driven by AI, data center expansion, and regionalization of chip manufacturing. Current valuation compression presents a compelling opportunity for long-term investors.

The company is up nearly 127% over the last five years. Despite this, I believe the price has the power to 5x from the current level over the course of the next decade.

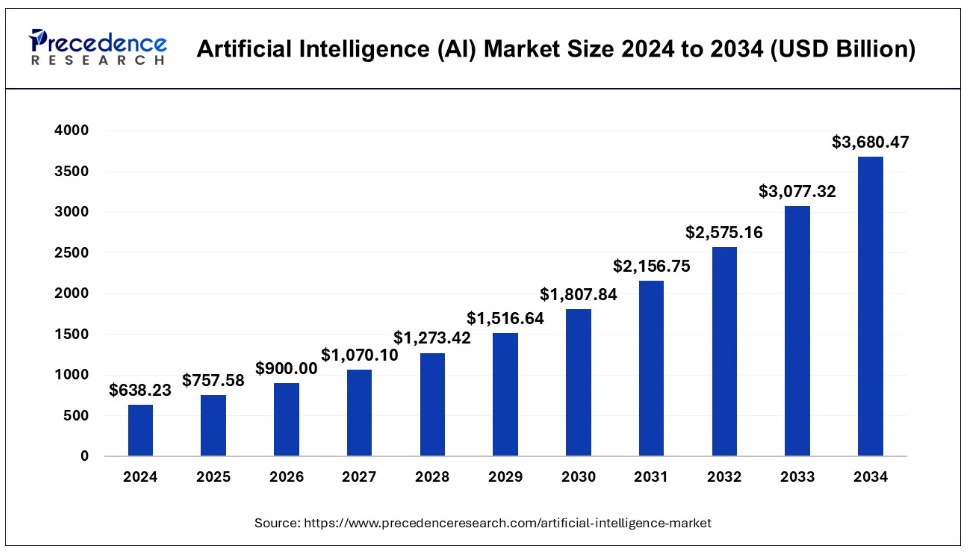

The size of the AI market alone is projected to grow at a CAGR (compound annual growth rate) of 19.20% through 2034. Yes, 19.20% growth PER YEAR. ASML is uniquely aligned to capture a sizeable amount of this growth over the next decade.

Financial Results and Operational Performance

Q1 2025 Financials:

ASML reported net sales of €7.7 billion and net income of €2.4 billion, representing a net income margin of 30.4%. Earnings per share came in at €6.83, beating analyst estimates by €0.31. Gross margin expanded to 54%, driven by favorable EUV product mix, higher ASPs, and installed base service revenues. Operating profit margin was slightly down quarter-over-quarter but improved meaningfully year-over-year.

Revenue Breakdown:

Net system sales totaled €5.7 billion

EUV: €3.2 billion

DUV and other: €2.5 billion

Installed Base Management: €2.0 billion

Net bookings: €3.94 billion

60% from Logic customers

40% from Memory

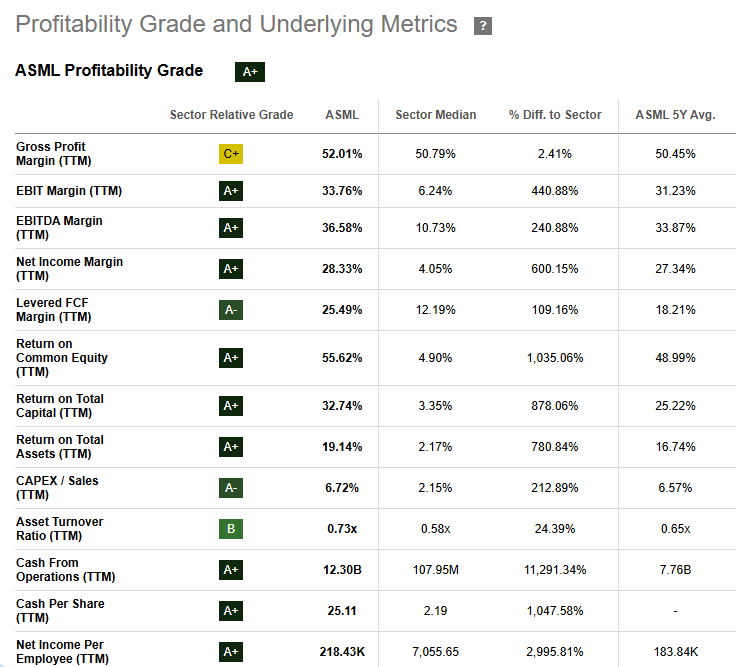

The bookings miss (vs. €4.8 billion expected) was a focal point of the market’s negative reaction, despite being partially expected due to quarterly volatility and order lumpiness. Gross margins exceeded guidance and reflected solid operational execution. ASML currently earns an A+ rating in terms of profitability!

Demand Outlook and Growth Drivers

Secular Tailwinds: AI, HPC, and Cloud Infrastructure

Spending from hyperscale cloud providers such as Amazon, Microsoft, Google, are Meta are projected to exceed $500 billion by 2026, growing over 40% YoY. These companies require custom, high-performance chips that depend on ASML's advanced lithography tools. EUV and upcoming High NA systems are integral to sub-5nm chip production, underpinning future semiconductor capabilities.