Here Are The Stocks Billionaires Are Buying

Billionaires are making opposite bets on the exact same tech giants.

Every 90 days, the SEC forces billionaire fund managers to do something they would rather not: show you exactly what they own.

It is called a Form 13F, and it is one of the most underused tools in a retail investor’s arsenal. Any institutional manager with over $100 million under management must file one within 45 days of each quarter ending. The result is a public, searchable record of their entire long portfolio, updated four times a year.

There are caveats. The 45-day delay means you are seeing where they were, not necessarily where they are going. Short positions are excluded. And no single investor has a perfect track record. But when you see the same names appearing across multiple high-conviction funds, or when a legendary investor makes a dramatic, unexpected move, it is worth paying very close attention.

This quarter delivered plenty of both. Here is what the filings are telling us, and what it means for your investment portfolio.

1. Funds Are Loading Up on Microsoft and Google

Two of the world’s largest funds made major moves into Microsoft MSFT 0.00%↑ and Google GOOG 0.00%↑ this quarter, and the size of these trades is worth paying attention to.

TCI Fund Management, a $45 billion London-based hedge fund run by billionaire Chris Hohn, built a significant new position in Google this quarter, moving it up to 5% of the entire portfolio. Meanwhile, Pershing Square, Bill Ackman’s flagship fund, went the other direction and built a brand new $2.1 billion position in Microsoft, with Ackman describing it as a high-conviction long-term bet on the company’s AI monetization potential through its 450 million Microsoft 365 users.

13F Filings: TCI Fund Management Q1 2026 | Pershing Square Q1 2026

When funds of this size make concentrated moves into specific stocks, it usually signals a high degree of conviction in the long-term thesis, not a casual trade.

I personally own both and am happy holding both. But if you are asking where I see the better entry point right now, it is Microsoft. I covered the full thesis in “Microsoft Is Extremely Undervalued”.

I am now up more than 100% on my Google position, so entry here just isn’t as attractive. However, the market is currently treating Microsoft’s AI infrastructure spend as a liability. I think it is the opposite.

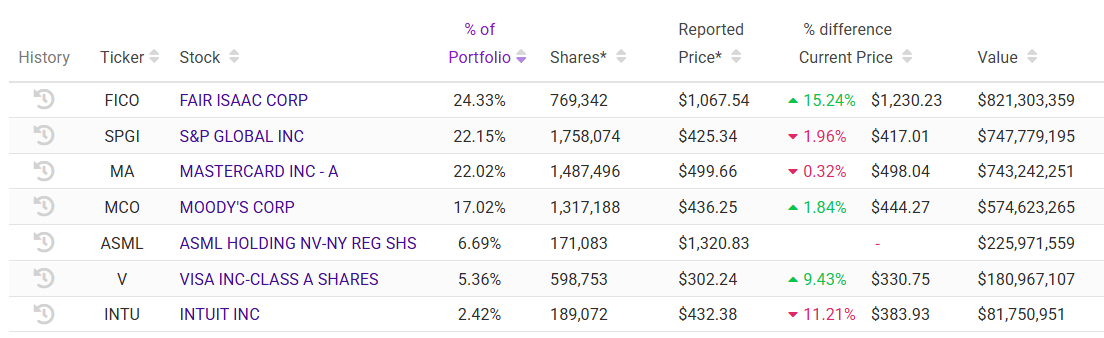

2. Dev Kantesaria

Dev Kantesaria runs Valley Forge Capital, a concentrated, high-conviction fund known for owning only the highest-quality businesses. His top holdings as of Q1 2026 include FICO 0.00%↑ (Fair Isaac), S&P Global SPGI 0.00%↑, Mastercard MA 0.00%↑, and ASML ASML 0.00%↑.

The problem? He is down roughly -20% year-to-date, a painful stretch for a manager who has historically been one of the more disciplined quality investors in the game. You’ll also notice that his portfolio holds only 7 companies.

This is actually a topic we have already dug into. In “The Software Apocalypse”, I walked through why the market is hammering S&P Global and Moody’s on AI disruption fears and why I think that thesis misses the mark entirely. These companies own proprietary, non-public data that AI models cannot legally train on. Billion-dollar institutions are not firing Moody’s in favor of a chatbot. Kantesaria’s thesis is sound, but the market is punishing him anyway in the short term.

His ASML holding is another name we have been accumulating here. I initiated a position in ASML in May 2025 and have been adding ever since. It is up over 100% from my entry and I still think the business can compound at roughly 15% annually for the next five years.

👉 Paid subs can get my buy alerts first. Here’s a limited time 20% discount.

This is a useful reminder that even “safe,” high-quality businesses are not immune to drawdowns, especially when valuations are elevated going in. Concentrated quality portfolios can get hit hard during rotations.

13F Filing: Valley Forge Capital Q1 2026

3. Berkshire Is Selling... A Lot

Warren Buffett’s Berkshire Hathaway continued its trend of reducing holdings this quarter, trimming across a number of positions. Berkshire has now been a net seller of equities for several quarters running, and the cash pile sitting on the balance sheet has grown to historic levels as a result.

To put that in perspective: Berkshire is currently sitting on more cash than most countries hold in foreign reserves. Buffett has always said he would rather hold cash than deploy it at prices he considers unattractive. The fact that he keeps choosing cash over stocks tells you something about how he views current valuations.

For dividend investors, this is worth sitting with. Berkshire is often used as a rough barometer for value availability in the market.

When the most patient, disciplined capital allocator alive keeps choosing to do nothing, it is at least worth asking whether you are getting truly great prices on the names you are adding to, or whether you are paying up for quality in a market that is still historically expensive.

That does not mean you stop investing. Dollar cost averaging into great businesses works regardless of what Buffett is doing. But it is a useful gut check when evaluating whether a position is genuinely attractively priced or just “less expensive than it was six months ago.”

13F Filing: Berkshire Hathaway Q1 2026

4. They’re Buying Uber

Pat Dorsey, the former director of equity research at Morningstar and a widely respected expert on economic moats, opened a new position in Uber UBER 0.00%↑ this quarter.

Dorsey is known for only owning businesses with durable competitive advantages, so a new buy from him is worth paying attention to. Uber’s moat argument centers on its network effects: more riders attract more drivers, which attracts more riders, in a self-reinforcing loop that is increasingly hard to displace. The platform is also expanding beyond ride-share into delivery, freight, and autonomous vehicle partnerships, such as with Rivian RIVN 0.00%↑.

Interestingly, in “There’s Always Something to Worry About”, I covered the bear case against Uber, specifically the argument that AI agents could route orders to generic couriers and bypass the platform entirely. My take was that the network effects are more durable than the bears give credit for. Dorsey opening a position this quarter suggests he lands in the same camp.

Uber does not pay a dividend today, but it is the kind of capital-light, network-effect business that could become a meaningful cash returner in the years ahead.

13F Filing: Dorsey Asset Management Q1 2026

5. All-In on Amazon

Alta Rock Capital made a big portfolio bet on Amazon this quarter. Amazon is increasingly a story about AWS (cloud), advertising, and AI infrastructure rather than just retail. For a fund that concentrates in its highest-conviction ideas, a large Amazon position signals real confidence in those secular growth drivers.

As I argued in “Everyone Is Wrong About Amazon (And The Tariffs)”, the market has been mispricing Amazon badly. Between the hidden $100B Anthropic stake on the balance sheet and the severely undervalued advertising business, there is a lot of value that the headlines simply miss. It is reassuring to see a concentrated quality fund arriving at the same conclusion.

I have roughly $40k in Amazon and if I had the capital, I would double my position. I believe that we will see AMZN 0.00%↑ eventually reach a $10T market cap in our lifetime.

13F Filing: Alta Rock Capital Q1 2026

6. They’re All Betting Big on AI

Brad Gerstner of Altimeter Capital, one of the most prominent tech-focused investors, has been leaning heavily into AI infrastructure plays. His thesis is that the current wave of AI investment is still in early innings, and the companies building the foundational infrastructure (chips, cloud, models) will compound for years.

This aligns with a broader theme across the Q1 filings: smart money is not fading AI. They are picking which AI winners will have durable, defensible moats. In “The AI Crucible”, I outlined why ASML, Microsoft, and Meta are the three companies whose results would determine whether the AI narrative holds. That framework still applies here.

13F Filing: Altimeter Capital Q1 2026

7. Chuck Akre’s Fund Faces Headwinds

Chuck Akre built one of the greatest long-term track records in investing through Akre Capital Management, concentrated in compounders: businesses that can reinvest at high rates for long periods. The fund’s largest holdings have historically included names like Mastercard, Moody’s, and Airbnb.

The concern heading into the current environment is that many of Akre’s core holdings are richly valued, and the fund has already seen trimming of positions like Mastercard and American Tower. With Akre himself retired and the next generation managing capital, the next few years will be a real test of whether the process holds up.

Mastercard and Moody’s are names I have written about extensively here. In “There’s Always Something to Worry About”, I covered why the AI disruption fears around Mastercard MA 0.00%↑ and Visa V 0.00%↑ are overblown and why the payment networks remain some of the most durable moats in existence.

13F Filing: Akre Capital Management Q1 2026

Takeaway

Here is the honest summary: the super investors are not in agreement right now. Billion-dollar funds are making opposite bets on the same stocks. Quality-focused managers are getting punished by a momentum-driven market. The greatest value investor alive is choosing cash over equities.

What does that mean for you?

It means the old rules still apply. Valuation matters. Buying great businesses at bad prices still leads to bad outcomes, even if the business is genuinely great. AI disruption is real but nearly impossible to predict with precision, and the 13F filings this quarter prove that even the smartest money in the world cannot agree on who wins and who loses.

But here is what I keep coming back to.

Whether you are building a dividend income machine or compounding growth stocks for the long run, the investors winning over decades are not the ones making the loudest calls. They are the ones who stay disciplined, buy quality at reasonable prices, and let time do the heavy lifting.

That is exactly the framework we use here. Every month I share what I am buying, what I am watching, and where I think the best risk-adjusted opportunities are across both income and growth.

If you want buy alerts the moment I am adding to positions, plus founding member access to CainAI to ask what billionares are buying, now is the time to upgrade.

Become a Paid Member and Get Founding Member Access

Stay the course. Own quality. And let compounding do what the billionaires cannot seem to agree on.

Disclaimer: This is not investment advice. Always do your own research and consult with a financial professional before making investment decisions.

whalewisdom.com is a site that tracks 13F filings if anyone wants copy the top hedge funds.

Great post!!! The construction of the reasoning is bordering on perfection.