How $1,000 Per Month in Passive Income Actually Works & How Long It’ll Take You

How Real People Are Using Yield to Replace Their Paychecks Without Chasing Gimmicks

Most people assume that making $1,000 per month in passive income requires millions of dollars or some complex strategy that feels out of reach. You don’t need to watch another bullshit Youtube video about opening a storefront on Shopify or about dropping products on Amazon AMZN 0.00%↑. This process is a lot more straightforward.

Whether you are starting with just $250 a month or a $25,000 portfolio, getting to $1,000 per month is a matter of simple math. Once you understand the income potential of your investments and how long it will take to reach your goal, the entire process becomes much easier to plan. I will show you what it actually takes to generate $1,000 per month in income. I will also outline three different approaches based on your risk tolerance, capital, and timeline.

How $250 A Month Can Turn Into a Reliable Passive Income Stream

Most people overestimate what they can do in a year, and underestimate what they can build in a decade. When it comes to long term investing, consistency beats intensity. And SCHD is one of the best ETFs for consistent dividend investors who want to build real, usable income over time.

These paths include:

A safe, long-term strategy focused on dividend growth

A moderate approach using higher-yield assets

A faster, income-first method that prioritizes cash flow

No gimmicks. No fluff. Just real-world income math that works. I’ve been able to significantly outpace the return of market indexes while also generating superior income levels from my portfolio. Over the last twelve months, my dividend portfolio is now up over 42%, compared to the US Stock Market increase of 15.5%.

What $1,000 per Month Actually Means

Before jumping into strategy, let’s get clear on the math.

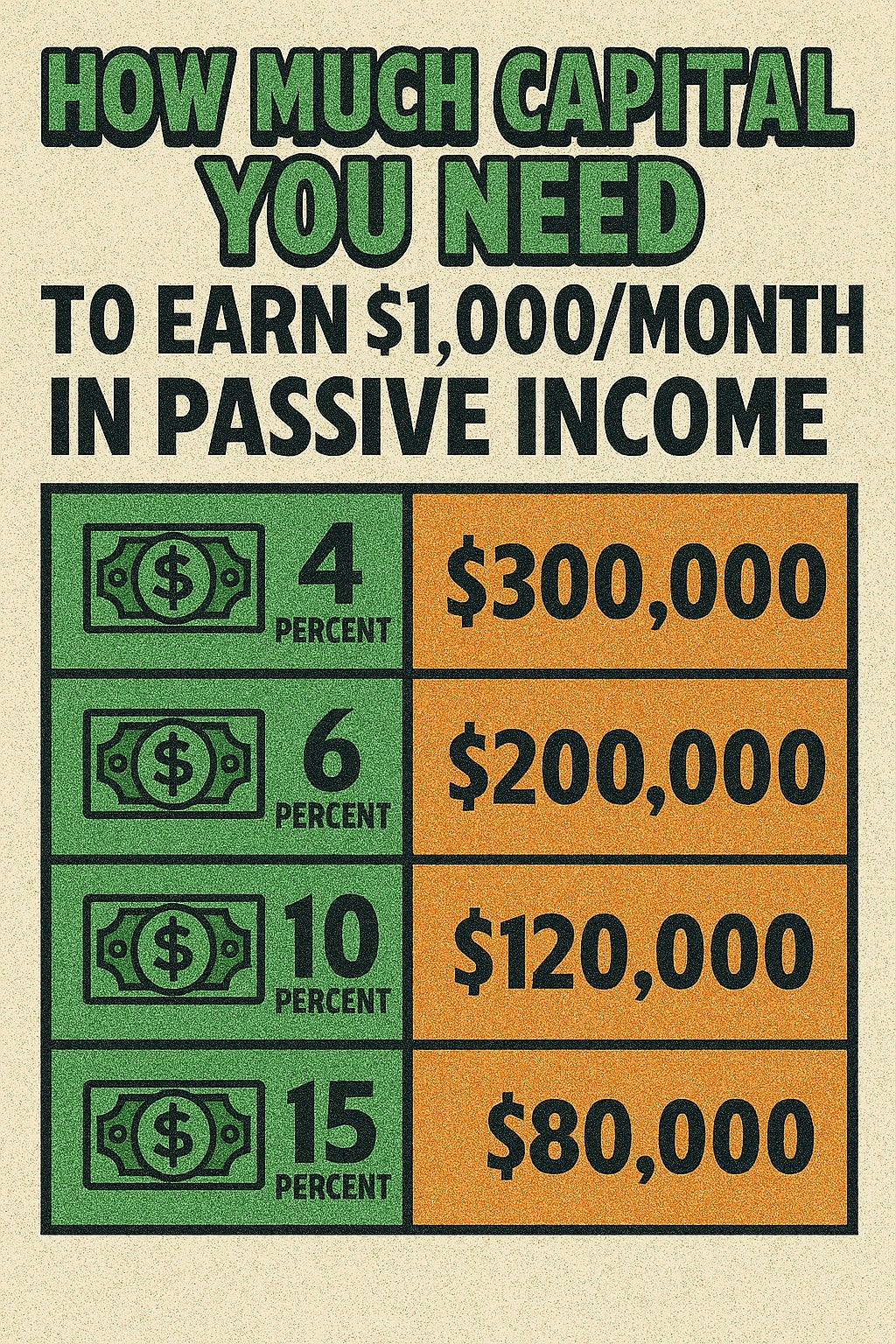

Earning $1,000 per month means producing $12,000 per year in passive income. How quickly you can get there depends entirely on the yield of your investments.

Here is how much capital you would need at different yield levels - it’s a simple math problem of amount x yield.

The higher the yield, the less capital you need. But that often comes with trade-offs, including more volatility, lower growth potential, or a need for more active management.

Some people prefer a slow and steady path with high-quality dividend stocks. Others are open to using tools like closed-end funds, high-yield ETFs, or margin to speed things up.

Three Real Paths to $1,000 per Month

There is no single way to reach your income goal. Some people prefer a slow and steady approach, while others want results as fast as possible.

Below are three paths to earning $1,000 per month in dividends, each with different levels of capital, yield, and risk.

Path One: The Safe and Steady Route

Who this is for: Investors who want income with long-term growth and lower volatility.

Typical investments: Blue-chip dividend ETFs like SCHD 0.00%↑ and DGRO 0.00%↑, along with quality stocks like Johnson & Johnson JNJ 0.00%↑ and Realty Income O 0.00%↑. You can even choose a total market fund, which includes exposure to the entire stock market with something like Vanguard’s Total Stock Market ETF VTI 0.00%↑.

Average yield: Around 3 to 4%

Capital required: About $300,000

Timeframe: 10 to 15 years with regular contributions and reinvestment

This route is perfect for people who want to sleep well at night. You will not get huge payouts early on, but you will build a solid income stream that grows over time.

Path Two: The Balanced Income Approach

Who this is for: Investors who want higher income without taking on extreme risk.

Typical investments: REITs, BDCs, and high-yield ETFs like MAIN 0.00%↑, DNP 0.00%↑, ARCC 0.00%↑, EPD 0.00%↑, and GPIQ 0.00%↑ or JEPQ 0.00%↑.

Average yield: Around 7 to 10%

Capital required: Around $120,000 to $170,000

Timeframe: 5 to 8 years with consistent investing and some reinvestment

This is a practical middle ground. It offers higher yield than dividend growth stocks, while still avoiding the most aggressive strategies. Many of the funds in this group pay monthly and generate real cash flow you can use.

Path Three: The Aggressive Cash Flow Plan

Who this is for: Investors who want income fast and are willing to accept more risk or complexity.

Typical investments: YieldMax ETFs, synthetic strategies like QDTE 0.00%↑, YMAX 0.00%↑, ULTY 0.00%↑, and XDTE 0.00%↑ and tactical margin.

Average yield: 12% upwards of more than 50%.

Capital required: As little as $30,000 to $80,000

Timeframe: 1 to 3 years if reinvested and managed properly

This is the strategy for people who want results now. It uses high-yield instruments that often come with more volatility or tax complexity. Some investors use margin here to amplify returns, though it must be done carefully.

Each of these paths can work. The key is choosing the one that matches your personality, timeline, and comfort level. I have been able to incorporate a mixture of these paths to outpace the return of the market while also generating a growing stream of dividend income.

The Levers That Accelerate Your Results

No matter which path you take, your results will depend on a few key levers. These are the variables you can control to either speed up or slow down your journey to $1,000 per month in income.

Here is what makes the biggest difference:

1. Reinvesting Your Dividends

The simplest and most powerful move. Reinvesting your dividends creates a snowball effect. Instead of withdrawing the income, you use it to buy more income-producing assets. Over time, this accelerates your cash flow and shortens the time it takes to reach your goal.

2. Increasing Your Contributions

If you can regularly invest more each month, even a little, your timeline improves dramatically. An extra $250 or $500 per month might cut years off your goal, especially if you are using funds with 8 to 10 percent yields.

3. Using Margin Responsibly

Margin is a powerful tool when used correctly. Some investors use margin to buy more dividend-paying assets and generate weekly or monthly income on borrowed funds. It comes with risks, but if you understand your cost of borrowing and stay conservative, it can boost your cash flow significantly.

4. Choosing Monthly or Weekly Payers

Timing matters. Monthly or weekly-paying ETFs, BDCs, and CEFs create more consistent income you can reinvest or use. They also help you build psychological momentum by letting you see results faster.

5. Avoiding Yield Traps

Not all high yields are safe. Some funds offer unsustainable payouts that rely on return of capital, excessive leverage, or declining assets. Choosing high yield is fine but you must also look at dividend stability, NAV performance, and management track record.

Each of these levers can shorten your path or make it more efficient. The more you combine them, the faster you move toward your goal without needing to chase risky trades or time the market.

Up next, I will show you how I personally approach this using an AGGRESSIVE APPROACH. Here’s a real portfolio designed to generate over $2,000 per month in dividends.

🔒 Subscriber Exclusive: My Exact $1,000+ per Month Income Plan

So far, you’ve seen the math and the strategy. But here is how I put it into practice.

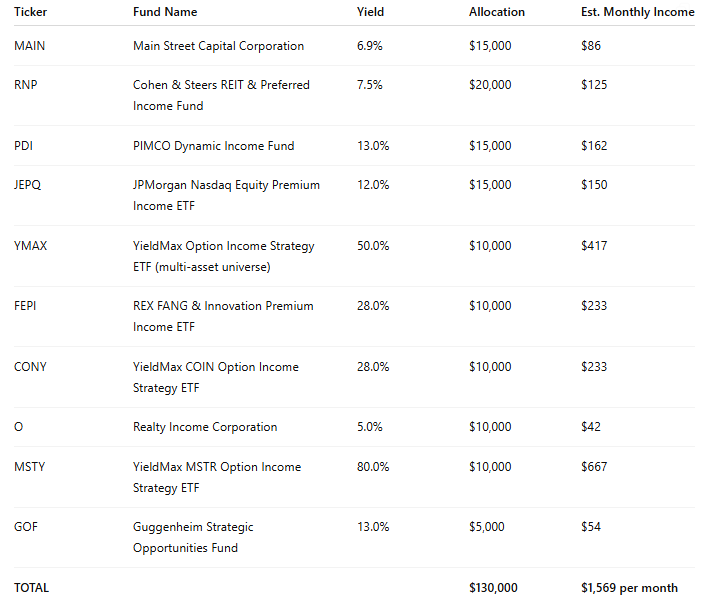

In this section, I will show you the actual structure of a dividend portfolio designed to generate $1,000 per month in income using real tickers, real yields, and real portfolio math.

An Efficient Income Allocation

This model is based on a portfolio size of approximately $150,000, spread across multiple monthly-paying assets with high and moderate yields.

Margin Strategy Snapshot

I currently use leverage in an effort to amplify the income that my portfolio generates. That leverage allows me to hold a larger position in high-yield names like MSTY 0.00%↑ and FEPI. The margin-financed portion of the portfolio yields over 40% on average, which still results in a strong net positive income spread.

Margin is never required. But used carefully, it can bridge the gap between capital limitations and income needs.

How I Use Margin Safely to Increase My Dividend Income

·Margin is money you borrow from your brokerage firm to invest. You are borrowing money and using your stocks as collateral.

How I Use This Income

70% of income is reinvested automatically into underweighted positions

30% is used for living expenses, margin interest, and cash buffer

I track portfolio changes monthly in my Dividend Update reports

$396,000 Dividend Portfolio Update #1

Most people share opinions. Fewer share receipts. Today I’m opening the curtain and walking you through my actual portfolio. Every fund, every stock, every decision reflects how I’m building income, protecting downside, and positioning for long-term wealth.

But What About Growth?

This portfolio is built for income, not for aggressive capital appreciation.

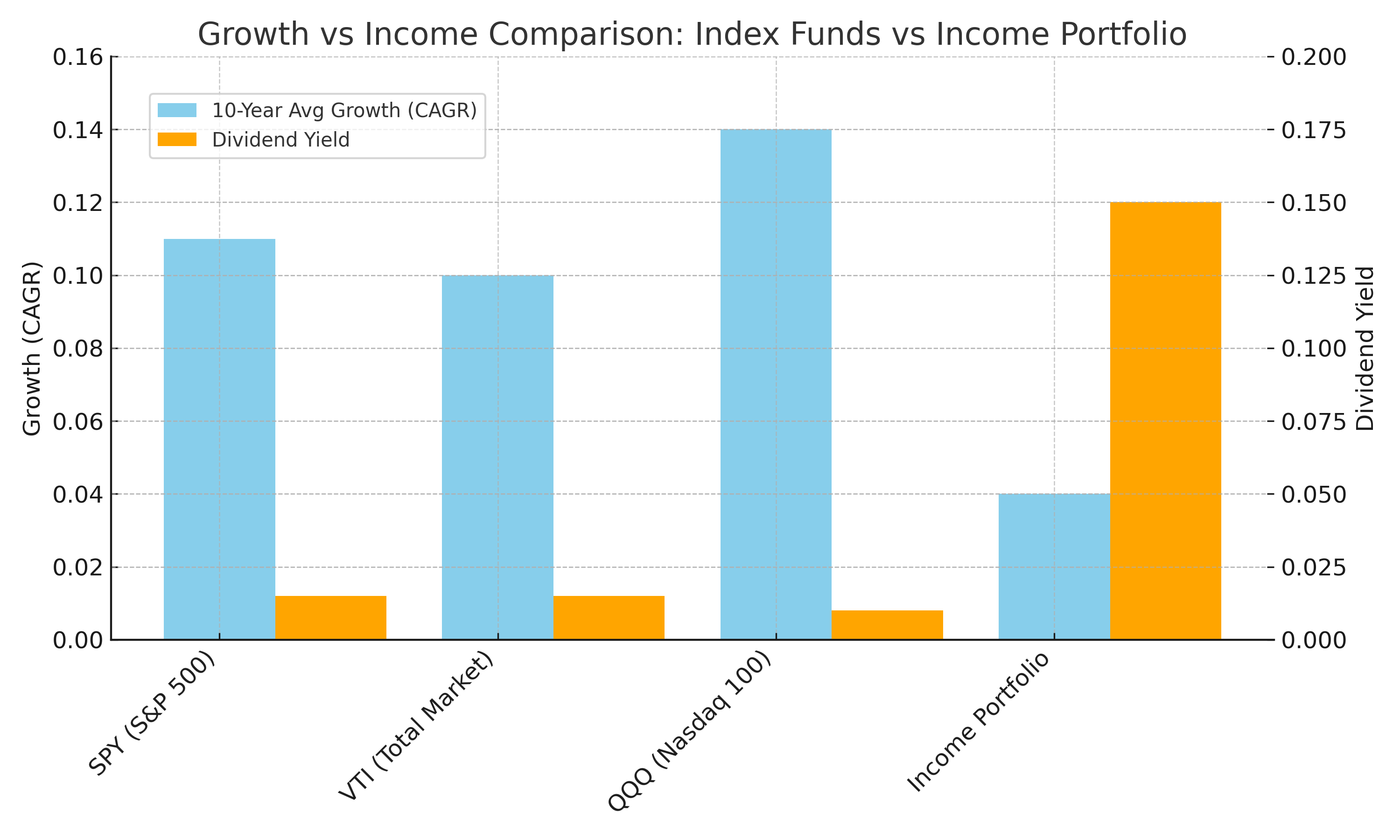

Many of the holdings in this list, such as PDI, GOF, YMAX, and MSTY, are designed to generate high cash flow through option premiums, fixed-income exposure, or leverage. That means their total return over time may lag well-known index funds like:

SPY (S&P 500 ETF) SPY 0.00%↑

VTI (Total Stock Market ETF) VTI 0.00%↑

QQQ (Nasdaq 100 ETF) QQQ 0.00%↑

Those funds are focused on long-term growth, powered by innovation and corporate earnings expansion. They reinvest profits, compound steadily over time, and tend to outperform income-focused assets over multi-decade timeframes.

In contrast, this income portfolio functions more like a cash-flow engine. It sacrifices long-term upside in exchange for consistent monthly payments that can be used today. The tradeoff is simple:

Index ETFs provide more growth with lower current income

Income-focused funds provide more income with limited long-term growth

So Who Is This For?

This kind of portfolio is not meant for everyone. It is most useful for people who are at a point in their financial journey where cash flow matters more than compounding.

It is well suited for:

Individuals approaching or already in early retirement who want consistent income without needing to sell shares

Investors with moderate portfolios who want to live off the yield while preserving their principal

Creators, entrepreneurs, or freelancers looking to replace unpredictable income with something steady

Anyone building toward financial independence and prefers seeing income results every month rather than waiting years for appreciation

Those comfortable with short-term price fluctuations in exchange for higher income today

People who want to use income to cover recurring bills, reinvest opportunistically, or ease into part-time work

This strategy is about producing tangible results now. It is not the fastest path to wealth, but it is a reliable path to freedom.

The chart above visually compares the tradeoff between growth and income across three major index funds—SPY, VTI, and QQQ—versus a high-yield income portfolio. As you can see, SPY, VTI, and QQQ offer significantly higher long-term growth potential, with average annualized returns ranging from 10 to 14 percent over the past decade.

However, their dividend yields remain quite low, hovering around 1 to 1.5 percent. In contrast, the income portfolio provides much higher monthly cash flow, with a yield near 15 percent, but it offers limited capital appreciation over time. This illustrates the core decision for investors: prioritize growth for future wealth or focus on income for financial independence and lifestyle flexibility today.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

Love the actionable articles, it not only explains what to do, but how to do it and how you can get started based on your risk and where you are.