How I Use Margin to Turn Dividends Into a $5,000 Monthly Paycheck

Using Dividends & Margin To Build Steady Income That Rivals A Paycheck

I remember the days when every raise at work felt like a joke. A few extra hundred dollars here and there, but with twice the responsibility. It never seemed to matter how much harder I worked, the paycheck still came up short. My efforts always felt like they were fueling someone else’s wealth while leaving me stressed about bills and the future.

I’d go through these stupid one-on-one calls to discuss performance and it always felt like managers nitpick the smallest things to criticize. I hated the fact that my value was ultimately determined by a manager. That frustration is what pushed me to look for something better. I wanted income that was steady, predictable, and not tied to the mood of a boss or the politics of a workplace. That is when I started focusing on dividends.

Dividends come in whether I am working or not. They do not care if I am on vacation, sick, or just not in the mood to grind through another endless week. The checks arrive like clockwork, and they grow over time.

It made me wonder. What if my portfolio could send me $5,000 every month, the same way an employer sends a paycheck, but without the stress, the meetings, and the endless demands?

The Math Behind $5,000 a Month

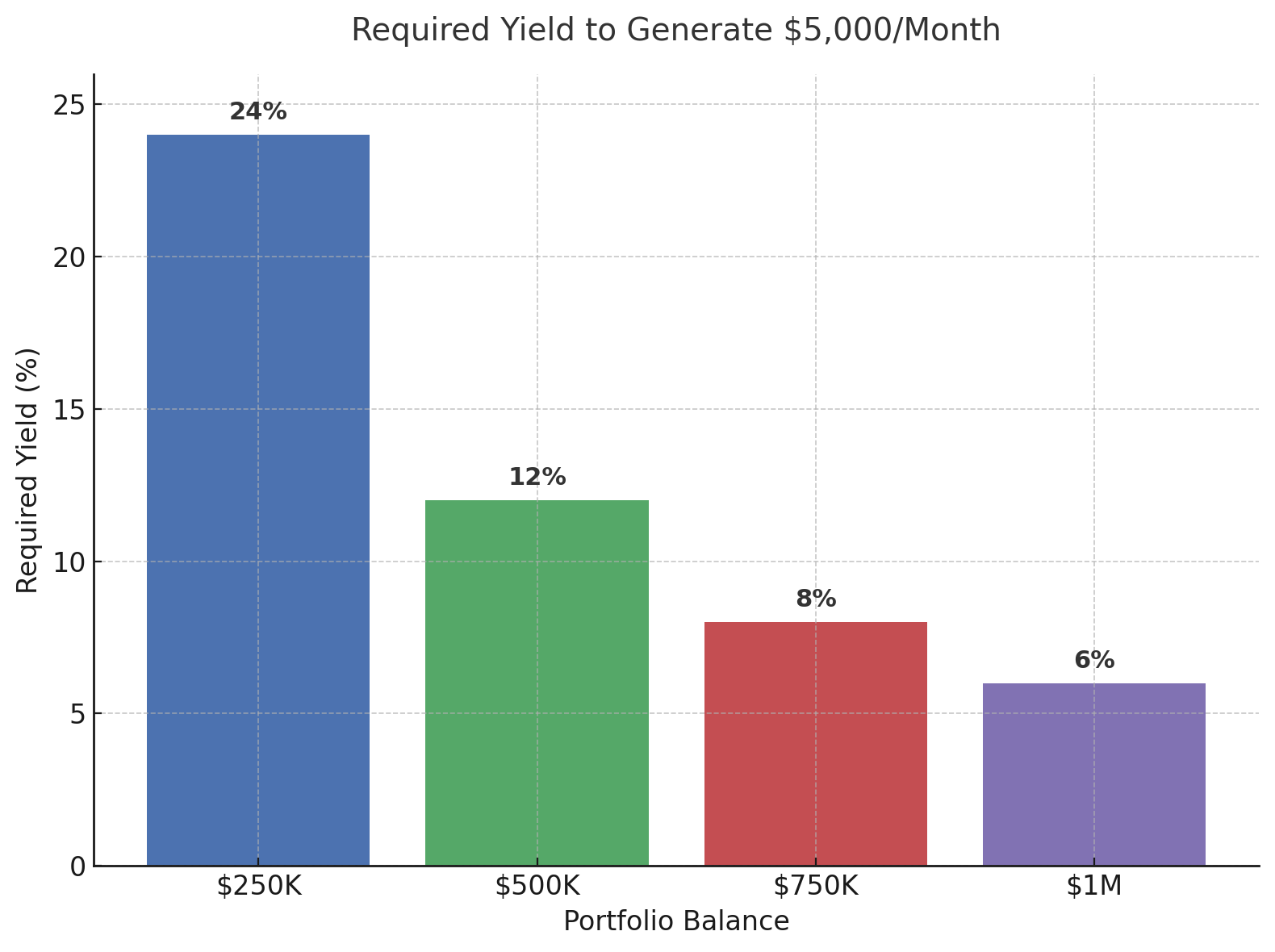

At first, the idea of collecting $5,000 a month in dividends might sound impossible. But when you break it down, the math is actually simple. Your portfolio balance and the average yield of your investments determine how much income you can collect.

Here is what the roadmap looks like:

With $1,000,000, you would need an average yield of 6% to generate $60,000 per year, or $5,000 per month.

With $750,000, the target yield rises to 8% to reach the same $60,000 annually.

With $500,000, you would need a yield of 12% to collect $5,000 per month.

With $250,000, it requires a much higher yield of 24% to reach the same income level.

Seeing it this way makes it easier to visualize what is realistic. For investors with a larger nest egg, even moderate yields can comfortably create a paycheck replacement. For smaller portfolios, it often means pursuing higher-yielding funds or a more aggressive strategy. However, there are tons of different funds that offer dividend yields above 30%, which means it’s relatively easy to create a large dividend income nowadays.

I utilize many of these high-yield funds to bring in thousands of dollars of dividends every month. For instance, I collected $3,991 in dividends in August. I published dividend reports on a monthly basis for readers.

August 2025 Dividend Report

For the month of August, my dividend portfolio paid me $3,991.11 in dividend income. On a year-to-date basis, I’ve now collected over $28,000 in passive income with dividends. I aim to accumulate $100,000 annually in dividends and I want you to join me on the journey. This is money that I didn’t have to actively work for and doesn’t include capital earned through other business ventures.

👉There is an exclusive Seeking Alpha analysis at the bottom of this article. Seeking Alpha charges $239/year to access full analysis. Paid subscribers here get the same depth of research, plus my personal portfolio, at a fraction of the cost.

If you’re serious about building steady, predictable cash flow from dividends, this guide is the best place to start.

I’ve put together a curated, research-backed list of WEEKLY & MONTHLY paying option ETFs, designed to help you create reliable income every single month:

✅ ETFs that actually pay WEEKLY and monthly, not quarterly

✅ Estimated yields commonly above 30%. Dividend yields can be as high as 100%.

✅ My top picks for consistent income engines

✅ Includes newer, high-yield option income funds from the YieldMax suite, Roundhill, NEOS, Kurv, and Goldman Sachs

It is one thing to understand the math, but it is another to build a portfolio that actually delivers the income. That is where most investors struggle. Some chase yields that are too high and end up with funds that erode over time. Others stay too conservative and never generate enough cash flow to make a real difference.

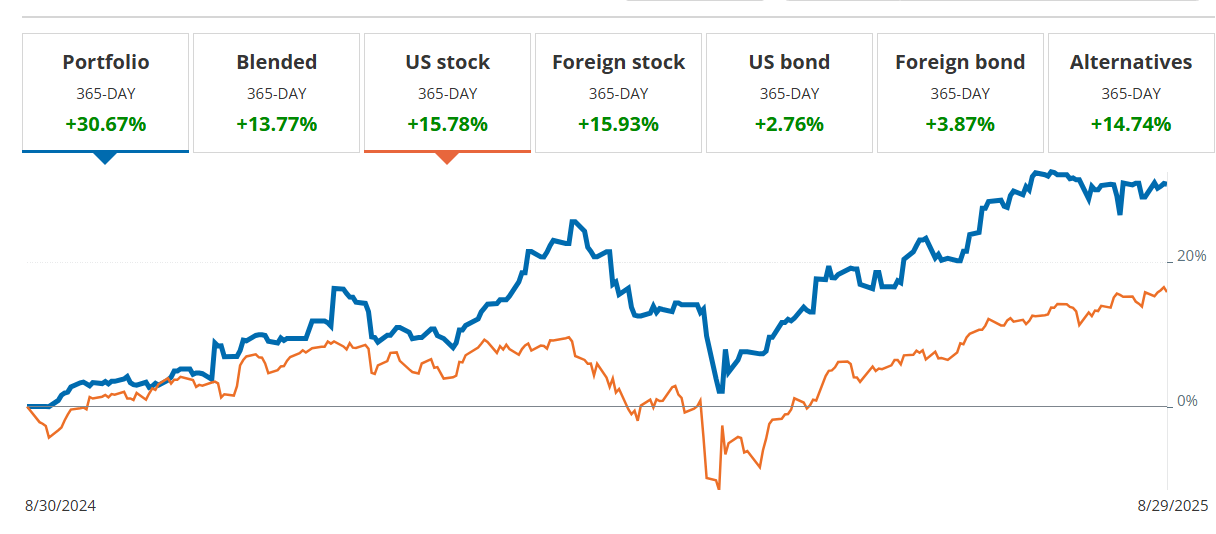

The key is finding the right balance. Balance is how I was able to achieve higher returns than the market indexes over the last twelve months.

My Portfolio: 30.67%

US Stocks: 15.78%

Turning the Math Into Action

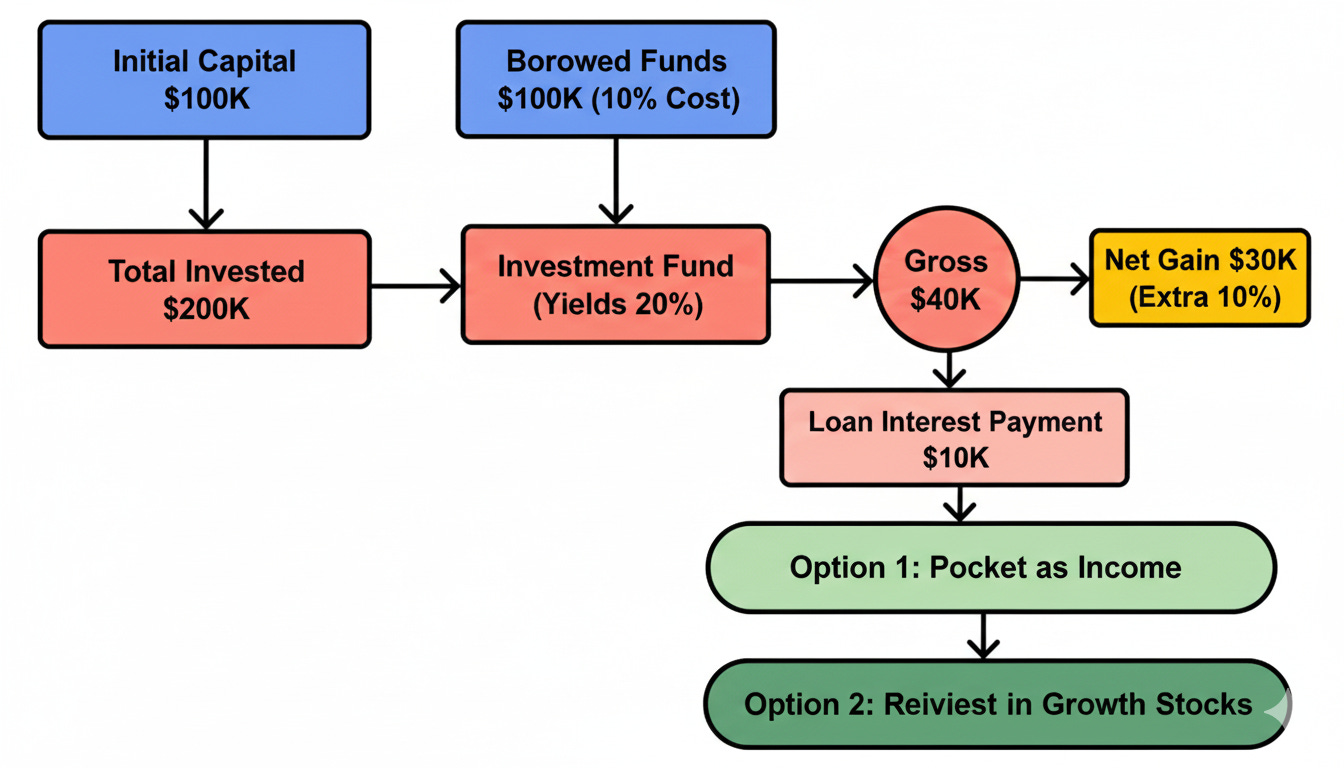

Margin Debt: is the money an investor borrows from a brokerage firm to purchase securities. This allows an investor to use leverage to buy more securities than they could with just their cash, magnifying both potential gains and losses. The existing securities in the investor's account act as collateral for the loan.

The real breakthrough comes when you stop thinking of margin as just a way to speculate and start seeing it as a tool for income. If you can borrow at a lower rate than what your investments pay in distributions, the difference becomes pure profit. That spread can then be reinvested into growth holdings without you having to touch your original capital.

For example, imagine borrowing at 10% while buying into a fund that yields 20%. The extra 10% is yours. That 10% can either be pocketed as income or funneled into growth stocks that build long-term appreciation. Over time, you are essentially using other people’s money to accelerate both income and growth.

This approach strikes a balance that most investors never think about. Your high-yield assets cover the cost of leverage and provide a steady stream of dividends. Your growth positions, funded by the spread, compound quietly in the background. Together, they create a system where you are not forced to choose between living off income today and building wealth for tomorrow.

Now, think about this in terms of the $5,000 per month target. Maybe your portfolio is currently producing $3,500. By applying margin strategically, the spread from high-yield funds could be exactly what closes the gap to $5,000. That difference can be the bridge between having supplemental cash flow and replacing a full paycheck.

This approach strikes a balance that most investors never think about. Your high-yield assets cover the cost of leverage and provide a steady stream of dividends. Your growth positions, funded by the spread, compound quietly in the background. Together, they create a system where you are not forced to choose between living off income today and building wealth for tomorrow.

3 Margin Worthy Holdings

To see how this approach works in real life, let’s look at three holdings that balance stability, high yield, and the ability to fund future growth.

👉There is an exclusive Seeking Alpha analysis at the bottom of this article. Seeking Alpha charges $239/year to access full analysis. Paid subscribers here get the same depth of research, plus my personal portfolio, at a fraction of the cost.

Ares Capital (ARCC) ARCC 0.00%↑

This has been a cornerstone of my portfolio for years. As the largest business development company in the U.S., it lends primarily through senior secured debt, which puts it at the top of the repayment ladder.

The dividend yield consistently hovers around 9% and is well-supported by earnings. This makes ARCC an ideal candidate for margin, since the yield spread over borrowing costs can be redirected into growth plays while still keeping your base income steady.

The price has remained stable for over two decades now.

Additionally, ARCC has paid out a high dividend yield for over two decades straight.

Rex Fang & Innovation Equity Premium Income ETF (FEPI) FEPI 0.00%↑

This is one of the newer high-yield option funds I track. By writing calls against high-growth names like Tesla TSLA 0.00%↑, Meta META 0.00%↑, and NVIDIA NVDA 0.00%↑, it transforms volatility into income. The current yield sits around 20%–25%. Even if you haircut that number for sustainability, FEPI still provides a huge cushion over typical margin rates. The extra income can either be pocketed as spendable cash or rotated into safer dividend growers.

The best part of FEPI is that it holds a ton of high quality technology companies within. So you are able to participate in the growth of the market and still collect a double-digit yield.

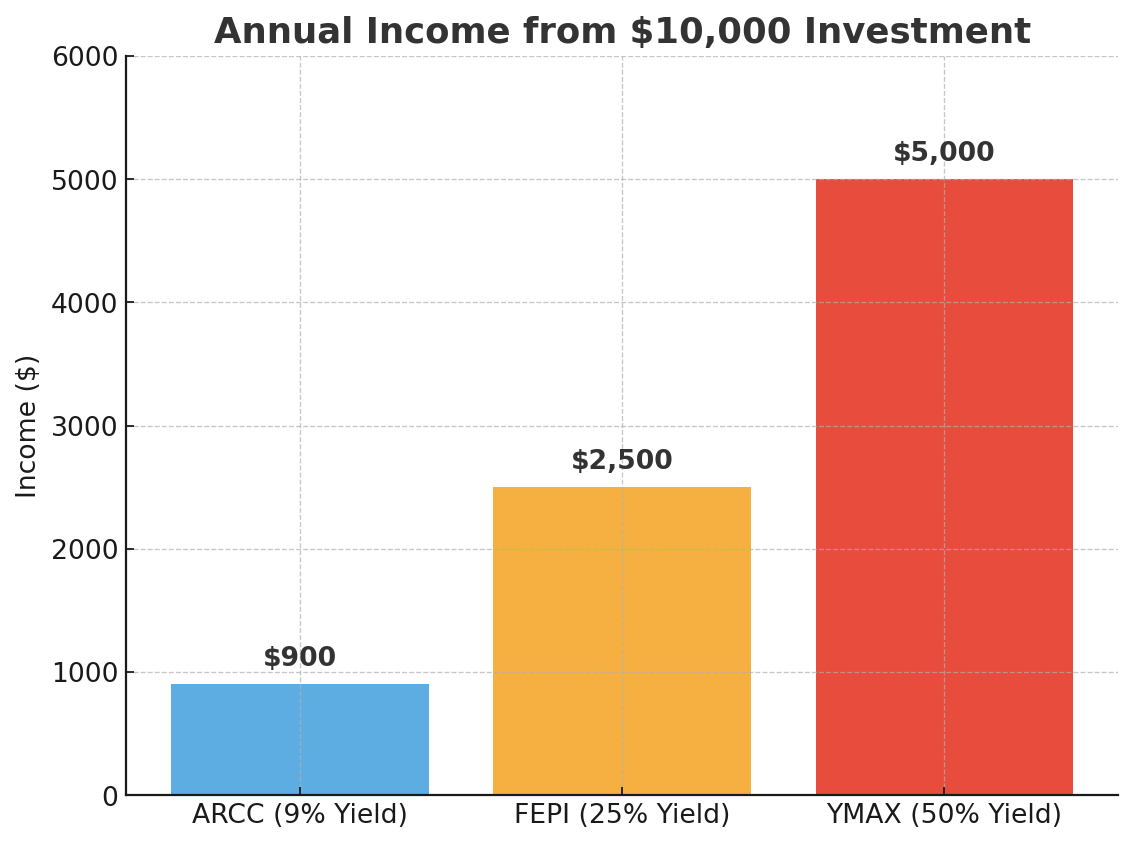

With a yield as high as 25%, a $10,000 investment can generate $2,500 per year. This large yield is perfect for implementing margin.

YieldMax Universe Of Funds ETF (YMAX) YMAX 0.00%↑

YMAX represents another class of income generators. These are ultra-high-yield funds that focus on single-stock covered call strategies. The payouts can exceed 40% on paper, though investors need to be realistic about potential NAV erosion over time. YMAX can fit nicely in a strategy like this if you treat it as a cash-flow engine rather than a long-term compounder. The oversized yield relative to margin costs creates immediate profit spreads that can be harvested and reallocated.

Together, these holdings illustrate the point: you don’t need to choose between income and growth. By strategically applying margin, you can let ARCC and FEPI fund the reliability, while YMAX produces excess cash that can be rotated into growth stocks. The end result is a portfolio that pays you now while still building wealth for the future.

👉Here is an exclusive Seeking Alpha analysis for free.

Here’s The Flow -

I use margin for YMAX and pocket the spread.

I allocate the distributions received from YMAX and buy more shares of FEPI, which is much safer.

I then take the distributions from FEPI and buy more shares of high-yield assets like ARCC, which provides stability.

Finally, the distributions received from ARCC are allocated to growth positions like ASML Holdings ASML 0.00%↑, Google GOOG 0.00%↑, or a regular ETF like QQQ 0.00%↑ or VTI 0.00%↑

Turn $100K Into $3,000 A Month In Dividends

Most people assume you need millions to live off dividends. After all, if you’re only getting a 3% yield from blue chip stocks, $100K won’t even buy you $3,000 a year. That’s not enough to cover groceries, let alone rent or a mortgage.

3 Safe High-Yield Investments That Can Pay You for Life

When I first started chasing dividend income, I thought I had struck gold. The logic seemed simple enough: find the highest yield and enjoy bigger paychecks every month. I bought into funds promising 60%, 75%, even 100% yields. At the time, it felt like I had discovered a shortcut to financial freedom. & Yes, I am telling the truth, these funds do exist.

Balancing Yield with Risk

Seeing numbers like 25% and 50% can make it tempting to simply throw all your money into the highest yielding funds. But here is the reality: the higher the payout, the more likely there are tradeoffs hidden underneath.

Take ARCC for example. At a 9% yield, it may not sound as exciting as FEPI or YMAX, but ARCC’s income stream is built on senior secured lending. That means it sits at the top of the repayment ladder when borrowers run into trouble. It is not flashy, but it is consistent and consistency is what keeps a portfolio standing during rough markets.

Now look at FEPI. Its strategy is built on writing calls against high growth names like Tesla and NVIDIA. This generates a yield in the 20% plus range, but that yield depends on volatility. If volatility cools, distributions could shrink. FEPI offers an attractive balance of income and exposure to innovative companies, but it is not the type of position you put your entire retirement savings into.

Finally, there is YMAX. On paper, a 40 to 50% yield looks like a dream. In reality, many ultra high yield option funds trade off that income with NAV erosion. Over time, the share price can drift lower even as payouts continue. This does not make YMAX unusable. It just means you have to treat it as a cash flow engine rather than a compounding long term hold.

This is why balance matters. Instead of chasing one extreme, the strategy is to combine them. ARCC gives the portfolio stability. FEPI provides an elevated level of income while maintaining some exposure to innovation. YMAX acts like a turbocharger, delivering cash flow that can be redirected into growth or reinvested elsewhere.

By blending these three, you get the best of both worlds: reliable income, attractive upside, and opportunistic yield, all without relying too heavily on a single strategy.

How I Use The Dividend Wheel Strategy With A $350K Portfolio

I have approximately ~$500K invested across a plethora of different accounts that all work in conjunction with one another. This only includes cash that has been allocated towards stocks and doesn’t include any Crypto or Real Estate. I’m working on an efficient way to release a full portfolio breakdown at some point in the future but for now, I wanted to provide a small glimpse into what my holdings and dividend income levels look like.

Using margin to buy high yield stocks, using those dividends to buy safer lower yielding ones and around and around it goes. A great system.

I remember reading about your idea of using margin at a lower rate and buying ETFs that offer a higher rate of return. I don’t remember seeing the results of your test and I was wondering if you could fill us in? Thank you