How I’d Collect $3,000 In Monthly Dividend Income From A $150K Medium-Risk Portfolio

It’s not about outperforming. It’s about getting paid to live on your terms

There’s something transformative about knowing that your portfolio will pay you regardless of what the market does, how your job is going, or where interest rates stand.

A consistent dividend income stream doesn’t just fund your bills. It buys you peace of mind. It reduces dependency on your employer, cushions economic downturns, and gives you the flexibility to make decisions based on desire instead of need. Whether it's taking a break from work, relocating, traveling, or covering a surprise expense, passive income adds breathing room to your life.

And perhaps most importantly, it acts as a long-term shield against inflation.

When prices rise, most people feel it immediately in the grocery store, at the gas pump, or in their rent. But dividend-paying assets can offset that pressure. Many companies and funds raise distributions over time, especially in sectors like energy, real estate, and infrastructure. Even if the payout stays flat, the fact that you own an income-producing machine means you aren’t stuck relying solely on savings that lose value every year.

Dividend income makes you less reactive and more proactive. It creates a buffer. It creates freedom. It puts you back in control.

And in a world where everything keeps getting more expensive, control is one of the most valuable things you can own.

This Might Be the Best Time in History to Build Income

If you are an income-focused investor, we are living in one of the most rewarding environments ever.

Between a flood of high yield ETFs, weekly paying option funds, structured credit vehicles, and business development companies, there has never been more variety or yield to work with. You no longer need a million dollar portfolio to generate meaningful cash flow.

With just $150,000, it is entirely possible to create a stream of income that pays over $3,000 per month. While this does not come without tradeoffs, it is a powerful way to turn stagnant capital into consistent income, especially for investors who already have a solid foundation built.

Top 5 Dividend Stocks Paying Me In June

There’s something powerful about getting paid just for owning shares.

This is the kind of strategy that is less about growing your net worth and more about extracting value from it.

How I Define Medium Risk

This portfolio is not for someone just starting out. If you are still in the accumulation phase, I believe you should build your foundation using a diversified mix of high quality stocks, ETFs, and long term compounders.

But if you have already done that and are looking to add an income layer that delivers real, usable cash, this strategy has potential.

I define this approach as medium risk for three reasons:

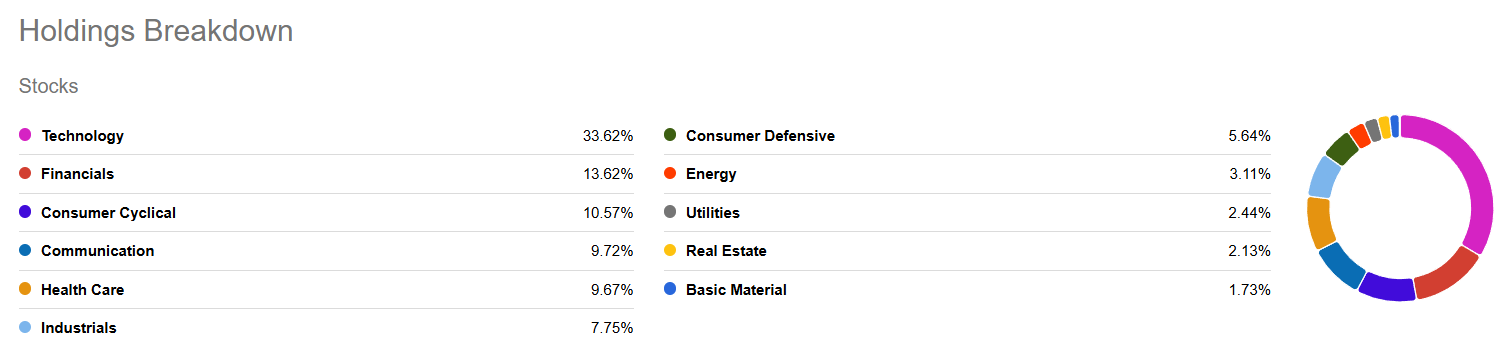

• More than half of the holdings are tied to indexes or diversified baskets, not individual stocks

• I avoid ultra concentrated, single stock synthetic ETFs, which tend to be more volatile and unpredictable

• The portfolio blends monthly and weekly cash flow streams, which gives it better liquidity and flexibility

This is not a YOLO setup. There are higher yielding options out there, but they come with much more risk. I built this with a focus on resilience, not just raw income.

What You Need to Know About High Yield Assets

This portfolio leans into four core categories:

Index-Linked Option Income ETFs

Funds like GPIX, XDTE, and QDTY use derivatives to generate consistent cash flow. They sell options against indexes like the S&P 500 and Nasdaq to extract yield while capping upside. Think of it as trading potential future gains for income now.BDCs (Business Development Companies)

PBDC offers actively managed exposure to companies that lend to small and mid-sized businesses. These are yield engines by design, funneling 90%+ of their earnings back to shareholders.Credit-Focused Closed-End Funds (CEFs)

ECC gives exposure to CLO equity—leveraged, floating-rate debt backed by corporate loans. High yield, actively managed, and tactically used in this allocation.Fund of Funds (FoF) and Weekly Option Hybrids

YMAG and YMAX invest across multiple strategies and pay weekly, offering both yield and high payout frequency. They come with risks, but their diversification provides some insulation.

Each holding is income first. Growth potential is limited, especially with the option ETFs, which cap upside by design. These funds trade off price appreciation for aggressive distributions.

And that is okay, as long as you understand the tradeoffs.

I will be sharing a portfolio of holdings below.

If we did a quick back test of the performance of this portfolio of holdings shared below. compared against the S&P, we can see that the performance is closely aligned. The only difference is that this approach spews off a lot more income.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

What Makes This Strategy Medium Risk

Many of these holdings have:

• Less than three years of track record

• Limited performance history in bear markets

• Exposure to debt rated below investment grade

• Variable distribution policies that can change frequently

I have intentionally avoided crypto-linked funds, single stock options strategies like MSTY, and hyper concentrated positions. Instead, this portfolio leans on funds with broad exposure, index overlays, or actively managed BDC and credit strategies that filter out underperformers.

So while the yield is high, the risk is diversified. I consider this a manageable setup for investors who already have other assets or a strong portfolio backbone.

So let’s take a look at the portfolio below -

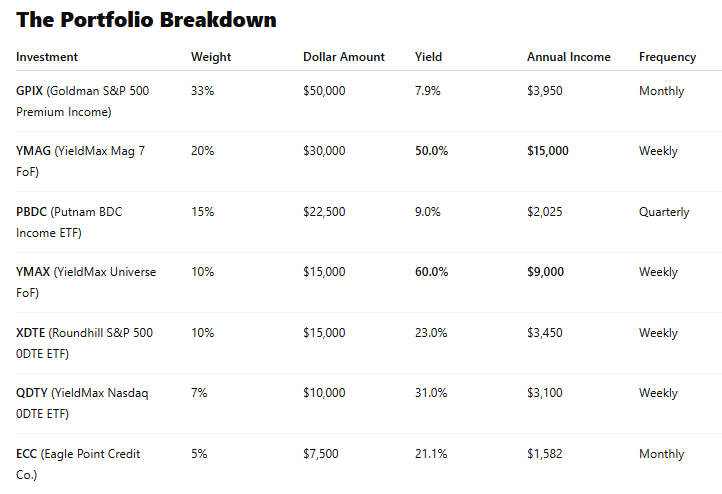

Total Annual Income: $38,107

Average Monthly Income: ~$3,175

Payment Frequency: Mixed (weekly + monthly + quarterly)

Why I Chose These Holdings

GPIX (Goldman S&P 500 Premium Income) - GPIX 0.00%↑

A resilient anchor. It provides index-linked exposure with a dynamic options overlay that adjusts with volatility. More agile than traditional covered call ETFs, making it a smart foundation. This allows GPIX to ease the use of options during bull markets, which would allow the price to grow alongside the rest of the market. Conversely, the fund may write a larger amount of options against its holdings during period of sideways or downward market movement.

I like GPIX because it actually holds the underlying equities within, creating a more stable fund. GPIX has a very reasonable gross expense ratio of 0.35%. Having the majority of the portfolio tied to the movements of an index significantly reduces the risk profile over the long term.

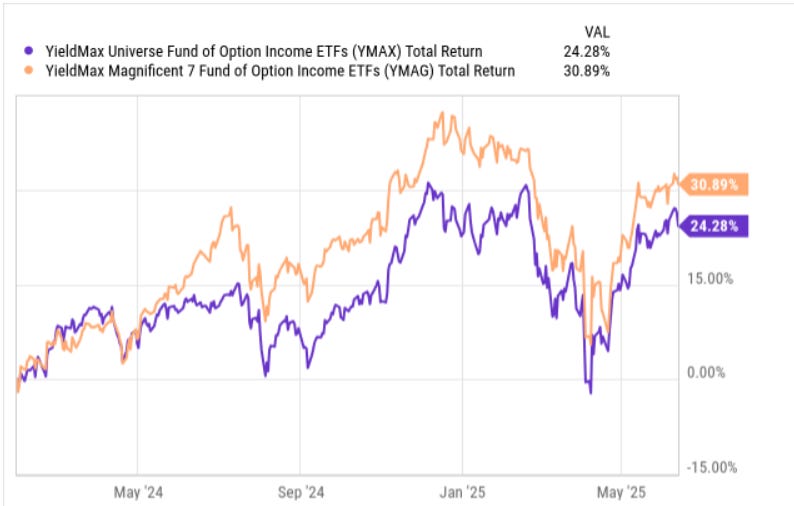

YMAG (YieldMax Mag 7 FoF) - YMAG 0.00%↑

YMAX (YieldMax Universe FoF) - YMAX 0.00%↑

These are the income drivers of the portfolio. YMAG focuses on the Magnificent 7 via synthetic strategies, while YMAX diversifies across high-yield assets and income overlays. Their weekly payouts and high yields (50–60%) are unmatched—but require awareness of tracking error and long-term sustainability. So YMAG aims to mimic the daily price change of the following companies:

Apple AAPL 0.00%↑

Microsoft MSFT 0.00%↑

Amazon AMZN 0.00%↑

Nvida NVDA 0.00%↑

Tesla TSLA 0.00%↑

Alphabet GOOG 0.00%↑

Meta Platforms META 0.00%↑

PBDC (Putnam BDC Income ETF) - PBDC 0.00%↑

PBDC is an actively managed business development companies ETF that eliminates exposure to underperforming BDCs. PBDC enables investors to collect a high dividend yield from the combination of the highest quality BDCs available. By choosing PBDC, you have the absolute highest level of diversity across the sector exposure that the debt investments are within.

The actively managed style increases the odds that PBDC can outperform through a changing interest rate environment. Management has done a great job at filtering out the BDCs that have suffered from distribution cuts or shrinking NAVs.

XDTE (Roundhill S&P 500 0DTE ETF) - XDTE 0.00%↑

QDTY (YieldMax Nasdaq 0DTE ETF) - QDTY 0.00%↑

Tactical exposure to 0DTE (same-day expiry) options strategies. These are newer products but provide structured, high-frequency income backed by large-cap indexes like the S&P 500 and Nasdaq.

How To Collect A Dividend Every Week Using Debt

Let’s be honest. Your bills do not show up once a quarter.

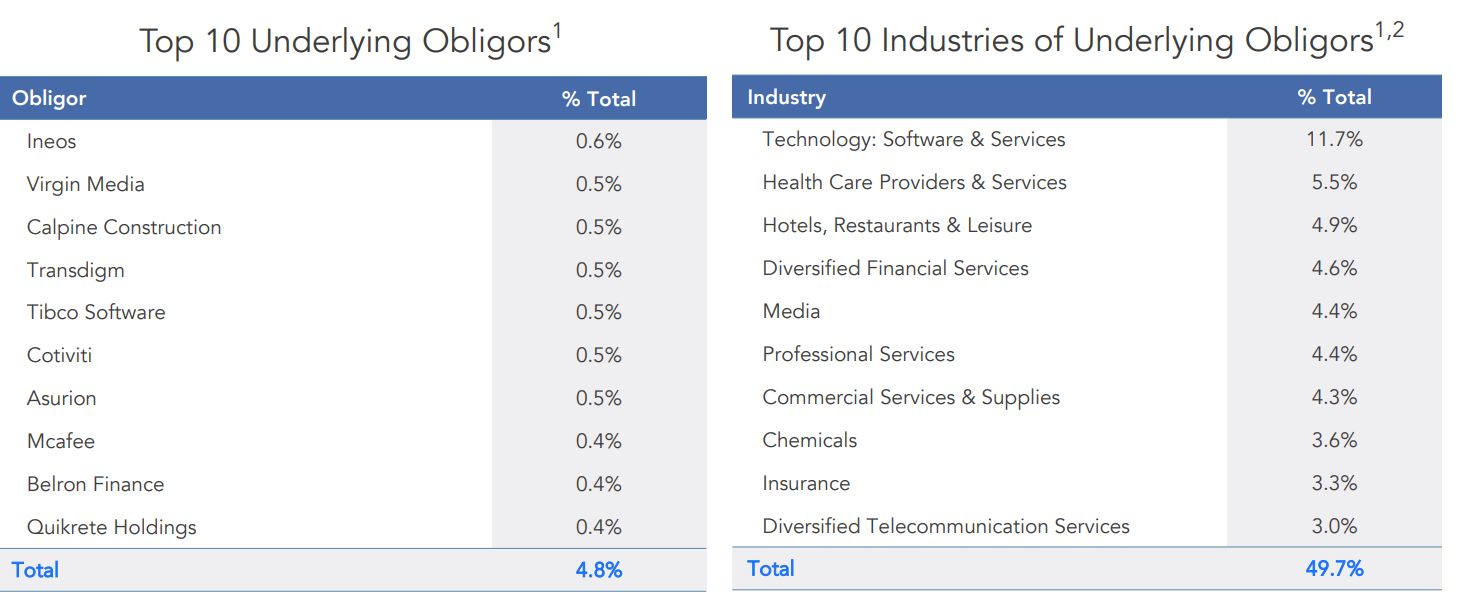

ECC (Eagle Point Credit Co.) - ECC 0.00%↑

A specialist in CLOs, which are baskets of corporate loans repackaged for institutional income. ECC manages the equity layer—high risk, high reward. Used here for credit diversification. ECC's strength is all in its diversity and solid dividend coverage.

The portfolio is spread across 1,792 underlying loan obligors, with a primary focus on CLO-equity investments. Over 92% of their portfolio operates on a floating rate basis, meaning that ECC can rake in higher levels of cash flow because of a higher interest rate environment.

Final Thoughts: Income As a Lifestyle Choice

This portfolio is built for payouts, not performance.

It won't beat the S&P 500. It won't make headlines. But it will send you cash every week and every month, which is a powerful tool for any investor seeking time freedom, career flexibility, or early lifestyle upgrades.

If you already have a solid net worth and want to start harvesting income, this approach is for you. It’s not about chasing the next big thing, it’s about building cash flow that supports your life.