How to Build a $1,000/Month "Forever Paycheck" (Without Yield Traps)

Stop chasing 100% yields. Here is the reliable way to cover your bills monthly.

In the hunt for passive income, it is easy to get seduced by triple-digit yields. But as we head into 2026, the market environment is shifting, and a 50% yield is meaningless if your principal is eroding by 40%.

For the new year, I am deploying a more sophisticated strategy. The goal is no longer just “income”—it is sustainable solvency. I am building a “Forever Paycheck” designed to deposit cash into my account every single month while preserving the capital base.

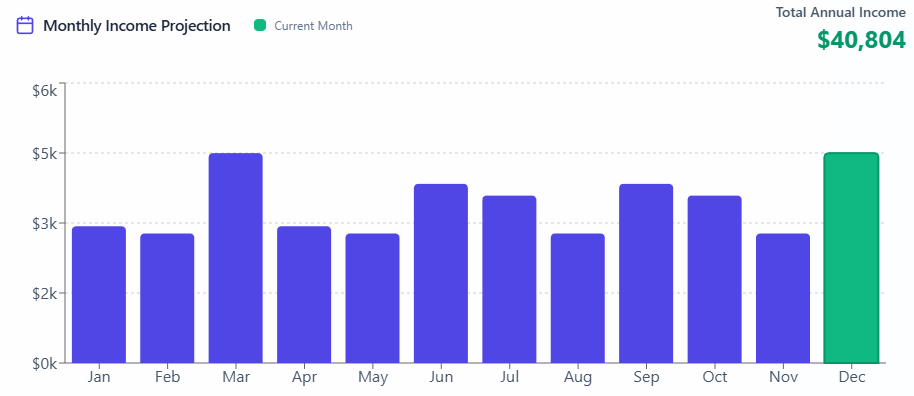

I’ve made some portfolio shifts recently and now my estimated annual dividend income sits above $40,000. I track my portfolio shifts and health with the Yieldly Dashboard.

Real Estate: Betting on the Rate Cut Cycle

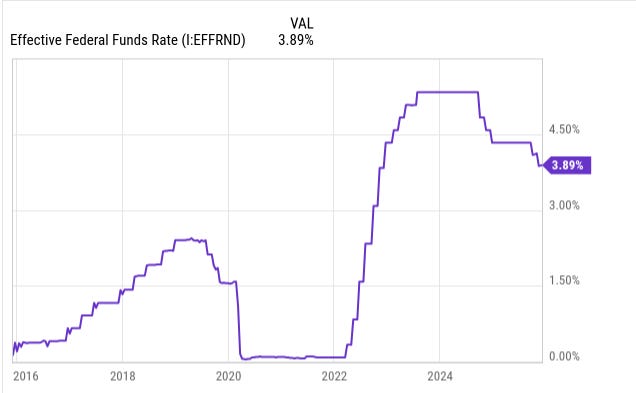

The first corner of the triangle anchors the portfolio in tangible assets. With the Federal Reserve signaling a stabilizing or declining rate environment for 2026, the sector poised for the most aggressive recovery is Real Estate. As we can see below, the federal funds rate was aggressively hiked to ten year highs throughout 2022 and 2023. This was done in response to record breaking inflationary data, as well as in reaction to the pandemic. The Fed had cut rates twice this year so far, but the federal funds rate still remains near its ten year highs.

Interest rates have a direct impact on the cost of borrowing. Since real estate is a sector that is arguably the most reliant on access to cheap debt to fuel operations. Simply put, a higher interest rate environment means that the cost of debt financing is more expensive. This negative impacts the operating spread for real estate businesses, between the cost of its debt and the yield/cash flow collected from its properties.

As a result of higher interest rates, many of the best REITs in the world have remained heavily suppressed. While their valuation and share price have remained suppressed, there are plenty of opportunities to lock in a sustainable high dividend yield.

Realty Income O 0.00%↑ is one of the cornerstones of the REIT market. Known as “The Monthly Dividend Company,” it has paid 600+ consecutive monthly dividends, but the real story is the valuation gap. As interest rates fall, the cost of borrowing for REITs drops, widening their profit margins.

By buying now, we are effectively locking in a ~5.5% yield—which is at the high end of its historical range. Realty Income pays out a dividend on the 15th of every singe month.

By investing into O 0.00%↑, you can essentially collect rent in the form of dividends. O has so many well known tenants under their umbrella:

This provides the “rent check” stability that high-yield option funds simply cannot match.

👉 Need help starting your journey? Consider the Dividend Income Start Kit!

👉 Here is what’s included:

✅ The Dividend Blueprint (PDF)

A step-by-step guide showing how I structure my portfolio, grow monthly cash flow, and reinvest for long-term income.✅ Monthly Dividend Map

50+ hand-picked tickers that pay monthly so you can ladder your income all year long.✅ Dividend Tracker (Google Sheet)

The exact spreadsheet I use to track yield, forward income, reinvestment, and portfolio growth.✅ Dividend Growth Legends: 50+ Stocks - Free eGuide

50 stocks that have an established history of dividend increases.✅ List of ETFs for Beginners To Start With

The Growth Engine: Monetizing Volatility

Stability is great, but we still need exposure to the AI revolution. The mistake many investors make is thinking they have to choose between “boring dividends” and “tech growth.” However, there are now covered call ETFs that pay you a double-digit dividend yield, while still growing your capital over time.

I believe that one of the best choices in the sector is:

Goldman Sachs Nasdaq-100 Core Premium Income ETF GPIQ 0.00%↑

This is an institutional-grade strategy that holds the actual Nasdaq-100 giants such as:

Nvidia NVDA 0.00%↑

Apple AAPL 0.00%↑

Microsoft MSFT 0.00%↑

Amazon AMZN 0.00%↑

Alphabet GOOG 0.00%↑

The fund offers a dividend yield of about 10% and uses a “Dynamic” call-writing strategy. Unlike older funds that cap your gains, GPIQ adjusts its option coverage between 25% and 75% depending on market volatility.

When volatility is high: They sell fewer options to generate the same income, leaving more of your portfolio uncapped to ride the recovery.

The Result: You get a target yield of ~10% while still participating in the majority of the Nasdaq’s upside.

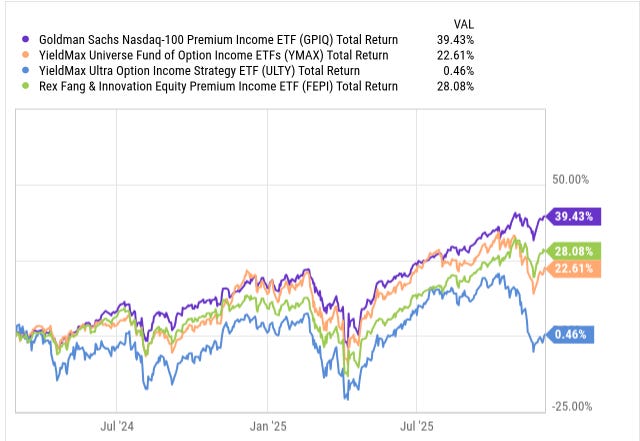

This is the “Have Your Cake and Eat It Too” trade for 2026: capturing the growth of Big Tech while generating double-digit monthly income. The fund is so strong that it has outperformed other funds that offer much higher dividend yields.

YieldMax Universe of Option Income ETFs YMAX 0.00%↑ - 47% dividend yield.

YieldMax Ultra Option Income Strategy ETF ULTY 0.00%↑ - 77% dividend yield.

Rex Fang & Innovation Equity Income ETF FEPI 0.00%↑ - 25% dividend yield

As we can see below, GPIQ (purple) has the highest total return due to its ability to participate in market rallies. I believe that GPIQ has proven to be a safe forever hold.

Becoming The Lender

Most people pay interest to lenders. They pay credit card interest, mortgage interest, car loan interest, etc. What I love about the stock market is that it allows us to become the lenders and collect interest from the world.

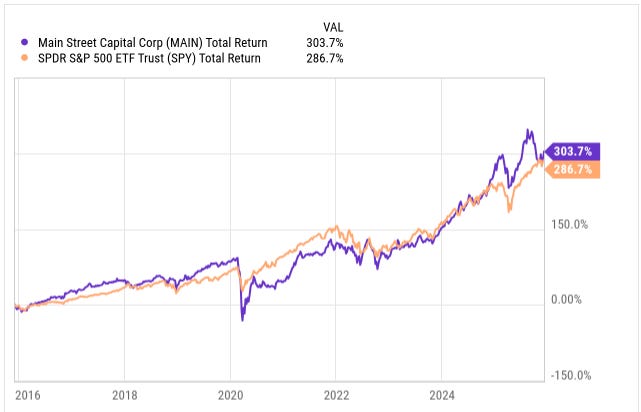

To supercharge the yield without risking erosion, we step into the role of the lender. Business Development Companies (BDCs) lend capital to middle-market firms, and Main Street Capital MAIN 0.00%↑ is the gold standard in this space. In plain English, MAIN lends capital to a diverse range of businesses that operate in different sectors. MAIN relies on a borrower’s ability to repay their loans, rather than grow earnings. So in other words, MAIN will provide favorable growth for shareholders as long as borrowers continue to keep up with their required debt maintenance. This is a much easier bet to make than hoping a company grows its earnings over time.

MAIN now offers a 7.1% dividend yield and payouts are issued on a monthly basis.

Unlike many peers that are externally managed (where fees eat into your returns), Main Street is internally managed, meaning its incentives are perfectly aligned with shareholders.

In fact, MAIN has outperformed the S&P 500 over the last decade. I fully expect this outperformance to continue.

This structure has allowed it to grow its Net Asset Value (NAV) to record highs for 13 consecutive quarters—a feat almost unheard of in the high-yield space. With a yield hovering around 7% and frequent special dividends, MAIN acts as the “banker” of the portfolio, profiting from the credit demand of growing American businesses.

The Roadmap to $1,000/Month

To generate $1,000 in monthly passive income, you need a portfolio value of approximately $150,000 (assuming a sustainable 8% blended yield).

HOWEVER, You don’t need $150,000 today. You just need to let the “Snowball Effect” work. Here are three realistic timelines to hit that goal based on your monthly contribution (assuming dividend reinvestment):

Scenario 1: The “Steady Builder” ($500/Month)

Strategy: You contribute $500/month and reinvest all dividends.

Time to $1,000/Month: ~13.5 Years.

The Reality: This is the slow lane, but it works. In the early years, your dividends are small. But by Year 10, the dividends themselves are contributing almost as much to the pot as your deposit is.

Scenario 2: The “Aggressive Saver” ($1,000/Month)

Strategy: You match your contribution to your goal ($1k in, $1k goal).

Time to $1,000/Month: ~8.5 Years.

The Reality: This cuts 5 years off your journey. By investing aggressively, you reach “Escape Velocity” faster—the point where your portfolio generates enough income to buy meaningful amounts of new shares on its own.

Scenario 3: The “Accelerated Path” ($2,500/Month)

Strategy: Prioritizing the portfolio above all other discretionary spending.

Time to $1,000/Month: ~4 Years.

The Reality: This is how you change your life in under 5 years. If you started today with $0, you could have a perpetual $1,000 monthly income stream by 2030.

If you’re just starting out, it may feel a bit scary to need a large amount of capital invested. This is why I recently published a post explaining how growth is an important part of the strategy.

The One Stock Every Dividend Investor Should Own for the Next Decade

Most people know me for dividend investing. It is the core of almost everything I build. But one thing I do not talk about enough is the role that growth plays in an income focused strategy and how it reduce the burden of margin debt. Growth is not the opposite of dividends.

The lesson for 2026 is clear: Don’t rent your yield. Own the assets that pay you.

👉 Calculate your own specific timeline with Yieldly.