How to Retire on $500K (Without Being Frugal)

Looking abroad for financial freedom and the 10% yielding assets that make it possible.

The American retirement dream is mathematically dead for the majority of the population.

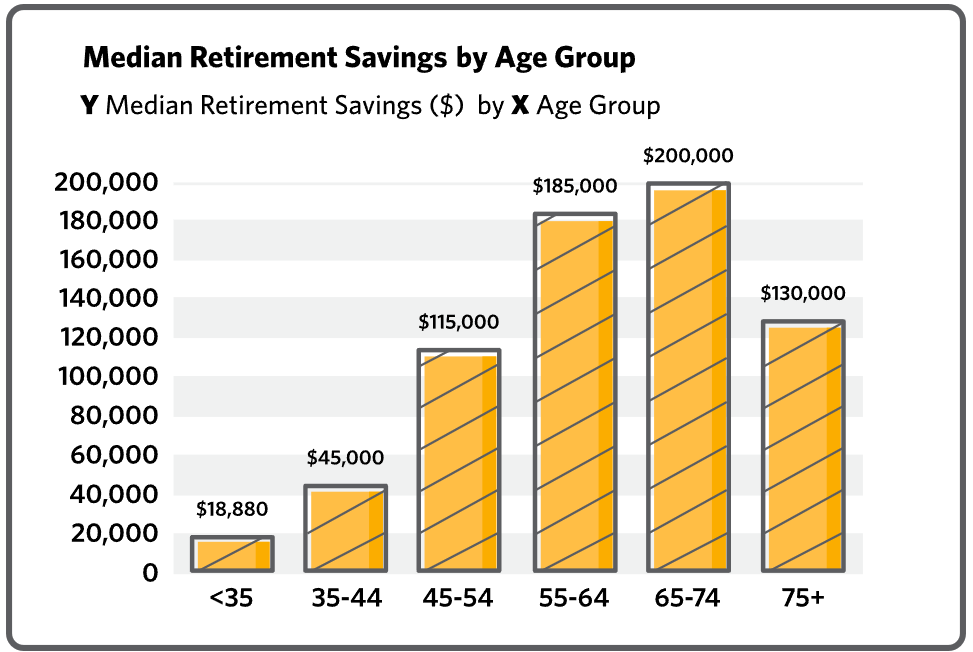

It is a statistical fact that most people will retire with insufficient funds. According to the Federal Reserve’s most recent Survey of Consumer Finances, the median retirement savings for Americans between the ages of 55 and 64 is just $185,000.

That is it. After forty years of labor, the average person has enough saved to cover maybe three years of nursing home care.

Meanwhile, financial planners keep moving the goalposts. They tell us we now need $1.5 million or even $2 million to retire with dignity. For a median earner, hitting that number is like trying to win the lottery. In fact, a recent survey showed that 1 in 10 Americans actually consider “winning the lottery” to be their primary retirement plan.

The system is broken. Inflation eats your savings, healthcare costs bankrupt seniors, and Social Security is a safety net full of holes. If you play by the old rules, you will lose.

But there is a “backdoor” out of this system. You do not need $2 million. You do not even need $1 million.

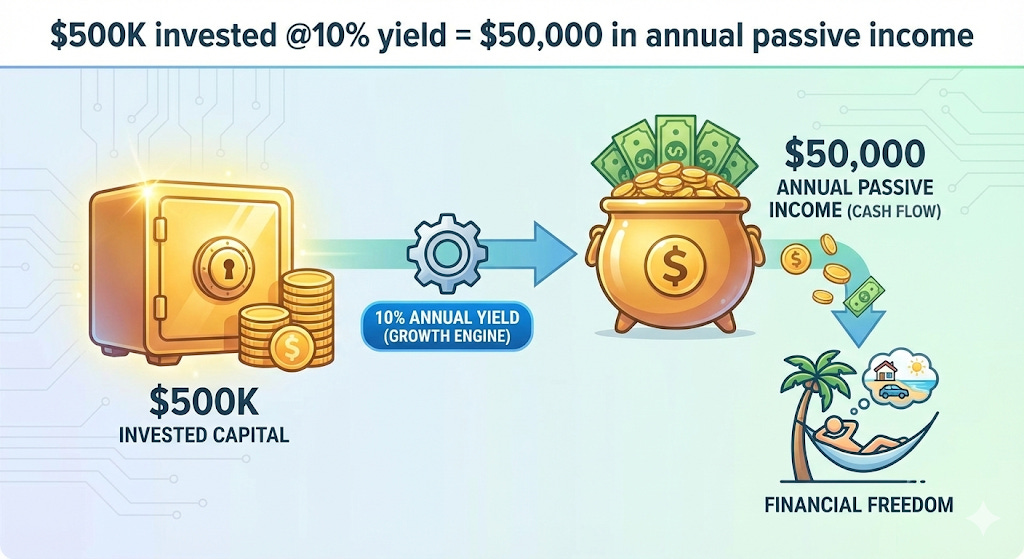

You can retire like royalty with a portfolio of $500,000. It’s simple math.

But how do you achieve a 10% yield? I will show you.

You just have to be willing to leave the broken system behind, which most people aren’t willing to do.

The Fix: Location Arbitrage

The reason you need millions of dollars in the US is because the cost of living is artificially high. You are paying a premium for proximity to high paying jobs that you no longer have.

The fix is Location Arbitrage. You earn and invest in the strongest currency on earth (the US Dollar) and you spend it in economies where it buys you a king’s life. During my trip to Japan, and it opened my eyes to what is possible. While Americans are paying $15 for something as simple as a sandwich, I was eating world class meals for $5.

In this article, I will provide “Escape Hatches” where a $50,000 annual income (generated from a $500k portfolio) puts you in the top 1% of earners. You will learn:

3 locations where $50,000 in annual income can get a high quality of life.

6 stocks that have a dividend yield of at least 10%.

How to generate passive income with dividends, without having to sell any investments.

Here are three 3 locations where $50,000 in annual income is enough to get a better quality of life than in the United States.

1. Japan

Japan is safer than any US suburb. The healthcare is affordable and modern. The infrastructure is efficient and jobs for Americans are plentiful.

The Cost: You can rent a clean, modern apartment in a major city like Fukuoka or Osaka for $650 a month.

The Lifestyle: You are eating out every night. You are taking high speed trains on the weekend. You are living without the fear of crime or medical bankruptcy.

2. Portugal

If you dream of Europe, Portugal is the answer. It offers the Old World charm of France or Italy at a fraction of the cost. I traveled through Portugal in 2024 and found out why it’s so popular with expats. The country promotes a high quality of life and can be affordable if you’re earnings USD.

The Cost: A couple can live comfortably on $2,500 a month in cities like Braga or Coimbra.

The Lifestyle: 300 days of sunshine. Incredible wine for €4 a bottle. Easy access to the rest of Europe.

3. Thailand

This is where your money goes the furthest.

The Cost: Luxury condos with pools and gyms cost $1,000 a month.

The Lifestyle: You can afford domestic help. You can eat at Michelin guide street food stalls for $3. You are living a life of actual luxury that would cost $200,000 a year in New York.

6 Stocks That Can Build the 10% Income Machine

The geography is the easy part. The hard part is generating the cash. How do you squeeze $50,000 of reliable income out of $500,000? You cannot do it with index funds yielding 1.5%.

To make this escape plan work, we need our money to work five times harder than the average investor. We are targeting a 10% yield on cost.

This requires a mix of Business Development Companies (BDCs), Closed End Funds (CEFs), and Option Income ETFs. The

Here is the watchlist of assets that currently yield north of 10%. These are the tools that fund the escape.

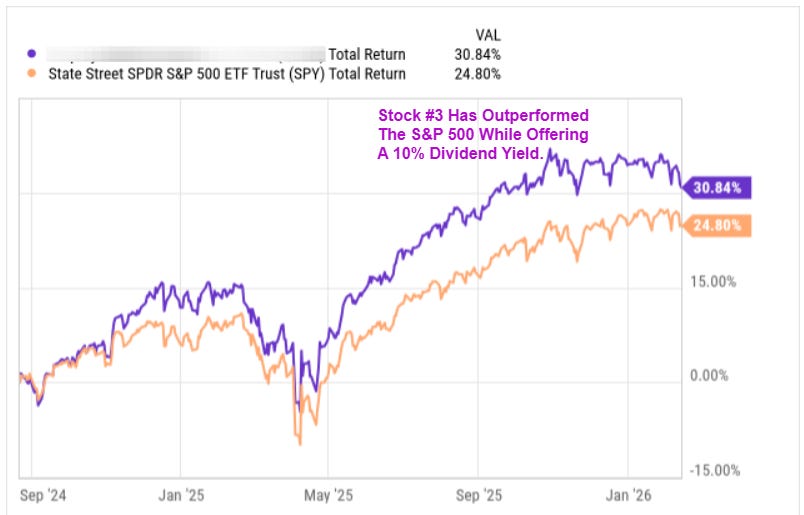

1. Bain Capital Specialty Finance BCSF 0.00%↑

Dividend Yield: ~14%

You aren’t just buying a generic lender; you are buying access to the Bain Capital deal flow. This gives BCSF a massive “origination advantage.” They see deals that regular banks and smaller BDCs never get invited to.

The Safety Net: 65%+ of their portfolio is First Lien Senior Secured debt. This means if a company goes bankrupt, BCSF gets paid back first—before other lenders and shareholders. Their “non-accrual” rate (bad loans) is currently just ~1.5%, proving they are excellent at picking winners.

The “Spillover” Bonus: BCSF is a cash machine. They often earn more cash than they are required to pay out, creating a “spillover” reservoir (currently ~$1.46 per share). This acts as a safety cushion for the regular dividend and fuels the frequent “Special Dividends” they pay on top of the monthly distribution.

The Trade: You are effectively becoming a partner in a private credit fund that lends to stable, middle-market companies ($10M–$150M EBITDA) that power the US economy.

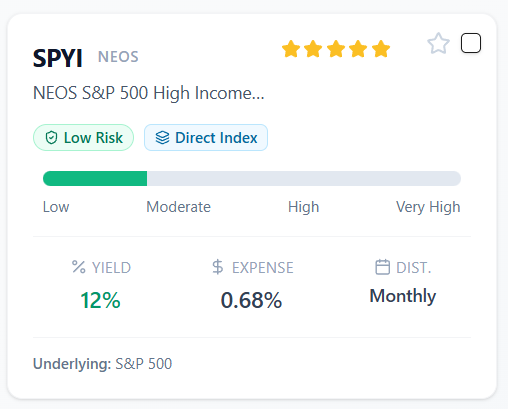

2. NEOS S&P 500 High Income ETF SPYI 0.00%↑

Dividend Yield: ~12%

Most investors own the S&P 500 (SPY) and get a tiny 1.3% yield. SPYI holds the exact same stocks—Apple, Microsoft, Nvidia—but uses an institutional options strategy to generate massive monthly cash flow.

SPYI is now listed as a 5-star fund in the High Yield Database. Paid subs get instant access to the High Yield Database.

The Safety Net: Unlike traditional “Covered Call” funds that cap your upside completely, SPYI uses a “Call Spread” strategy. They sell options above the current price. This means if the market rallies, you still participate in the growth. You get the 12% yield plus stock appreciation.

The Kicker (Tax Loophole): This is the real secret. SPYI utilizes Section 1256 Contracts for its options. In plain English: 60% of your income is taxed at the lower Long-Term Capital Gains rate, regardless of how long you hold the fund. It is one of the most tax-efficient income vehicles in existence.

To see the remaining 4 high yield assets that complete this 10% income portfolio, including the “Blue Chip” BDC and the 14% yielding inflation hedge, upgrade your subscription below.

Not ready to upgrade? That’s fine! You can still get a shortcut on your investing journey with this starter guide. You can get the dividend starter bundle so that you can skip the mistakes that I made.

👉 Here is what’s included:

✅ The Dividend Blueprint (ebook)

A step-by-step guide showing how I structure my portfolio, grow monthly cash flow, and reinvest for long-term income.✅ Monthly Dividend Map

50+ hand-picked tickers that pay monthly so you can ladder your income all year long.✅ Dividend Tracker (Google Sheet)

The exact spreadsheet I use to track yield, forward income, reinvestment, and portfolio growth.✅ Dividend Growth Legends: 50+ Stocks

50 stocks that have an established history of dividend increases.✅ List of ETFs for Beginners To Start With

3. Amplify CWP Growth & Income ETF QDVO 0.00%↑

Dividend Yield: ~10%

This is not a passive computer algorithm. It is actively managed by DIVO founder Kevin Simpson’s team. They hand-pick high-quality growth stocks like Google, Amazon, and Visa.

The Safety Net: Most high-yield funds own slow-growth “zombie” companies. QDVO owns the fastest-growing companies on earth. If the market rips higher, your principal grows with it.

The Kicker (Tactical Calls): Passive ETFs sell options on 100% of their portfolio every month, capping their winners. QDVO is “tactical.” They might only write options on 30% of the portfolio, or none at all if they think a stock is about to pop. They only sell upside when they think the stock is overbought, maximizing your total return.

4. NEOS MLP & Energy Infrastructure MLPI 0.00%↑

Yield: ~13%

MLPI buys the “toll roads” of the American energy grid—pipelines and storage facilities. These companies (like Enterprise Products Partners) charge fees based on volume, not the price of oil. They make money whether oil is $50 or $100.

The Safety Net: Energy infrastructure is a hard asset. In a world of printing money and sticky inflation, owning physical pipelines is one of the best ways to preserve purchasing power.

The Kicker (No K-1s): Usually, investing in pipelines (MLPs) is a tax nightmare requiring a specific K-1 form. MLPI solves this. It functions as a standard ETF (1099 form) but preserves the tax benefits. A massive portion of that 15% yield is often classified as “Return of Capital,” meaning it is largely tax-deferred until you sell the shares.

5. Guggenheim Strategic Opportunities Fund GOF 0.00%↑

Dividend Yield: ~17.7%

Guggenheim is a legendary fixed-income manager. This Closed-End Fund (CEF) has access to obscure bond markets—like asset-backed securities and military housing bonds—that retail investors cannot buy.

The Safety Net: Consistency. GOF has never cut its dividend since its inception in 2007. Through the 2008 crash, the 2020 pandemic, and the 2022 rate hike cycle, they kept the monthly check steady.

The Kicker (The Premium): Because GOF is so popular, it often trades at a premium to its assets (you pay $1.20 for $1.00 of assets). However, anytime that premium dips, you have a massive buying opportunity. You are essentially hiring a Wall Street bond desk to run a leveraged credit portfolio for you.

6. Ares Capital Corp ARCC 0.00%↑

Dividend Yield: 10%

ARCC is the largest BDC in the world. They have a portfolio of nearly 500 companies. When you buy ARCC, you aren’t just buying a stock; you are buying a diversified index of the American middle-market economy.

The Safety Net: Size matters. During the 2008 financial crisis and the 2020 pandemic, smaller BDCs went bust. Ares used its massive balance sheet to buy their competitors for pennies on the dollar. They are the “consolidator” in the industry.

The Kicker (Spillover): Ares is conservative. They often earn more money than they pay out. They currently sit on hundreds of millions in “spillover income” (undistributed earnings). This acts as a massive rainy-day fund, virtually guaranteeing the dividend will remain safe even if the economy hits a recession.

The Bottom Line

The “retirement crisis” is only a crisis if you insist on retiring in the same broken system that caused it.

You can lower your expenses by moving to another location in the world. You can raise your income by investing in assets like produce a sustainable stream of passive dividend income.

The math works. You just have to be brave enough to make the move.

BCSF shows to pay quarterly and monthly unless this, changed recently.

I would also add Panama to your list. Pensionado visa program gives the expat no taxes at all on all wealth and money generated outside Panama, discounts 10-50% on a lot of services, good and cheap public healthcare, excellent and cheap private healthcare, very safe (especially compared to neighbouring countries), very advanced banking system. No obligation on days living there. Plus they offer more visa programs for non retired people