If I Had to Start Investing With $1,000, Here's What I'd Do

A Beginner's Blueprint for Building Real Wealth One Month at a Time

Most people are one paycheck away from panic.

You probably know someone like that. Maybe you have been that person.

A raise will not fix it. A second job will not fix it. What actually changes the equation is owning something that pays you while you sleep or grows in value.

If you’re living paycheck to paycheck, I want you to look around and assess the things you own.

Do you have the latest iPhone? Why?

Is your car worth more than what you have in savings? Why?

How often do you eat outside versus cooking at home? Why?

If these points apply to you, there’s a structural issue that you need to address. How do you expect to get rich if you’re spending all of your disposal income.

I got my first corporate job at 19 while I was still in college. Good money for my age, stable, benefits, the whole thing. And about three months in I looked around and thought there is absolutely no way I am doing this for 40 more years.

I was making $2,800 a month after taxes and I committed $500 of it to investing every single month without touching it.

Not because I had it all figured out. Because I knew I needed a way out from that misery. I didn’t really have a clear vision of what ‘investing’ meant back then, but I knew I wanted control over my money.

I eventually scaled that number up every time my income grew, and eight years later I crossed $1,000,000 in invested assets. It started with exactly the kind of plan I am about to show you.

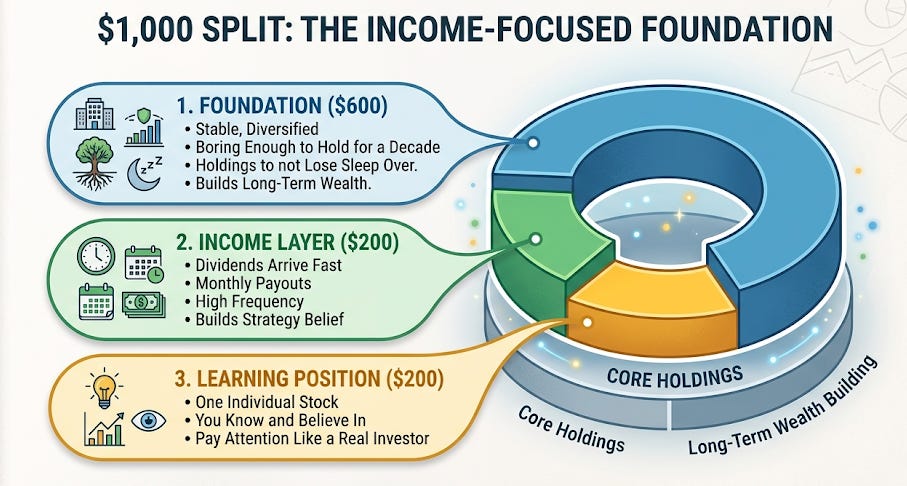

Here’s How I’d Split the $1,000

Before we get into the breakdown, let’s be clear about something.

$1,000 is not the destination. It is the proof of concept. The people who actually build wealth are not the ones who invested $1,000 once and waited. They are the ones who kept feeding the machine every single month, rain or shine, whether the market was up or down.

$500 a month into a disciplined portfolio will do more for you than a one-time $10,000 lump sum from someone who never touches their account again. Consistency beats capital every time.

So treat this $1,000 as your foundation. Then make a commitment to add to it regularly, even if it is $50 a month to start. The habit matters more than the amount.

Now here’s the split.

$600 goes to your foundation.

These are your core holdings. Stable, diversified, and boring enough to hold for a decade without losing sleep. This is where your long-term wealth gets built.

$200 goes to your income layer

This is the position that shows you dividends arriving fast. Monthly payouts, high frequency, builds belief that the strategy actually works.

$200 goes to your learning position

One individual stock you actually know and believe in. This is where you start paying attention like a real investor.

That’s it. Three layers. One simple plan.

The next few sections break down exactly what I’d buy in each one and why.

First $600: Your Foundation

Most beginners make the same mistake when they first start investing. They either go too aggressive chasing the highest possible returns, or they go too conservative and park everything in something so safe it barely moves. Both approaches miss the point. The goal with this first $600 is to build something that grows your capital steadily over time, gives you broad exposure to the best businesses in the world, and is boring enough that you never feel the urge to sell it when things get bumpy.

This is not the exciting part of the portfolio. It is the part that does the heavy lifting while everything else gets the attention. Think of it as the engine under the hood. You do not see it working but without it nothing moves.

I’d split this between two positions.

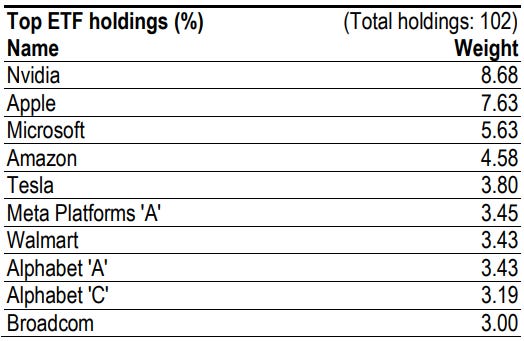

Invesco NASDAQ 100 ETF: QQQM — $350

QQQM 0.00%↑ tracks the Nasdaq 100, meaning you own a piece of the 100 largest non-financial companies on the planet.

Apple , Microsoft MSFT 0.00%↑, Nvidia , Meta META 0.00%↑, Amazon AMZN 0.00%↑. The best businesses in the world, in one fund.

Think about what these companies actually do. They do not just survive recessions, they come out the other side bigger and stronger. Microsoft has its hands in cloud computing, AI, gaming, and enterprise software. Nvidia is the backbone of the AI revolution. Apple has over a billion loyal customers who upgrade their devices every two years without thinking twice.

When you buy QQQM you are not betting on one company getting it right. You are betting that innovation and technology continue to drive the economy forward. That is about as safe a long term bet as you can make.

Fun fact! QQQM is my largest holding in my portfolio.

This is your growth engine. It is not a high-yield position but that is not why it is here. It is here because your income layer needs a strong capital base to grow from. A portfolio that only chases yield without growing its underlying value is standing still. QQQM makes sure that does not happen.

Put $350 here and leave it alone.

Vanguard Total Stock Market Index Fund ETF: VTI — $250

The other $250 goes into VTI, which gives you exposure to the entire U.S. stock market in one fund. We are talking over 3,500 companies across every sector and size. Large cap giants, mid cap growers, small cap underdogs, all of it in a single ticker.

This is the absolute lowest risk way to invest your money.

Here is why that matters. No one knows which sector is going to lead the market over the next decade. In the 2000s it was financials. In the 2010s it was tech. In the 2020s it has been a mix of AI, energy, and consumer staples depending on the year. VTI removes the guesswork entirely. You own everything, so whatever wins, you win with it.

Where QQQM is concentrated on elite growth names, VTI is your broad diversification play. They work together without much overlap drama. QQQM handles the high conviction growth bet and VTI handles everything else the economy has to offer.

Together these two positions give a beginner something most people spend years trying to build: real exposure to the market’s long term upside without needing to pick individual winners.

👉 If you want to get involved with investors who love growing their wealth and talking about stocks, consider joining the paid subscription. 10% discount included.

Next $200: Your Learning Position

This is where you get to make a more personal choice. And it is where you start learning the most.

I would use this slice to buy one individual dividend stock, something you actually know and believe in as a business. Not because individual stocks are always better than ETFs, but because owning a single company teaches you something that owning a fund never quite does.

You start reading earnings reports. You notice when the company raises its dividend. You feel it personally when the stock dips and you have to decide whether to hold or add more.

The best part about starting here is that you do not need to go hunting for obscure names. Some of the best dividend stocks in the world are companies you already interact with every single day.

If I had to guess, you are probably familiar with these three companies and you know exactly how they make their money.

Apple AAPL 0.00%↑ - You probably own one of their products right now. Over a billion people do. Apple has built one of the most loyal customer bases in history, and that loyalty translates directly into consistent cash flow, share buybacks, and a dividend that keeps growing. The yield is modest but the capital appreciation that comes with it makes this one of the strongest long term holds on the market.

Coca-Cola KO 0.00%↑ - People have been buying Coke in recessions, wars, financial crises, and pandemics for over a hundred years. Warren Buffett has held it for decades and has no plans to sell. The dividend has grown every single year for over 60 consecutive years, making it one of the most reliable income stocks on the planet. Boring? Yes. Proven? Absolutely.

Walmart WMT 0.00%↑ - When the economy gets tough, people do not stop buying groceries. They just start buying them cheaper. That is exactly why Walmart thrives when other retailers struggle. It has raised its dividend every year for over 50 consecutive years and continues to expand into e-commerce and healthcare, making it far more than just a big box store at this point.

Pick the one that resonates most with you. Learn the business. Own it with conviction.

Last $200: Your First Income Hit

Once you have your foundation and your individual stock picked out, this last $200 has one job: show you that the strategy actually works.

This is not about finding the highest yield. It is about building the habit and the belief that your money can pay you while you do nothing. That sounds simple but most people never actually feel it until they see it happen in their own account.

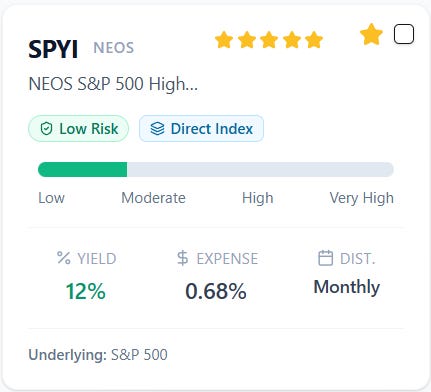

NEOS S&P 500 High Income ETF - SPYI 0.00%↑

SPYI owns the S&P 500 and layers an options strategy on top of it to generate monthly income that is significantly higher than what a standard index fund would pay. You get broad market exposure to the 500 largest companies in America and a monthly distribution that typically yields around 10 to 12% annually.

That monthly cadence matters more than people realize. When you see income land in your account thirty days after you invested, something clicks. The strategy stops being theory. You start watching the position, tracking the payouts, thinking about what happens when they reinvest. You start caring in a way that a quarterly payer never quite triggers.

$200 in SPYI at a 10% yield is roughly $20 per year, about $1.67 per month. That is tiny. But that is not the point. The point is that your money just paid you without you lifting a finger. Once you feel that for the first time, you will never stop wanting more of it.

Turn On DRIP and Walk Away

This is the step most people skip because it feels too simple to matter. It is the most important thing you will do after making your first purchase.

DRIP stands for Dividend Reinvestment Plan. Every time one of your positions pays you a dividend, instead of that cash sitting idle in your account, it automatically goes back in and buys more shares. No action required. No decision to make. No temptation to spend it.

Here is why this is such a big deal. That $1.67 SPYI pays you in month one does not just sit there. It buys more shares of SPYI. Those shares pay their own dividend next month. Which buys more shares. Which pays more dividends. The loop never stops and it never needs your attention.

It feels completely invisible in year one. You will look at your account and wonder if anything is actually happening. It is. The math is just quiet at first.

By year two you start noticing. Your monthly income is slightly higher than it was six months ago and you did not add a single extra dollar. By year three it is obvious. The portfolio is genuinely feeding itself and the gap between what you put in and what it produces keeps widening.

This is the part nobody tells beginners about. The market gets all the attention. Stock picks get all the attention. DRIP just sits in the background doing the most important work of all, turning every dollar you earn into more dollars that earn more dollars.

One click. Leave it on. Never turn it off.

Final Thought: The First $1,000 Is Never About the Money

Remember those questions from earlier? The iPhone. The car. The takeout.

Nobody is judging you for any of that. The point was never to make you feel bad. The point was to show you that the gap between where you are and where you want to be is not about income. It is about where your money goes after it hits your account.

$1,000 invested with a plan beats $10,000 spent on things that do not pay you back. Every single time.

You now have the plan. The only thing left is to start.

I wish they had Substack when I started investing

With fraction buys at most brokerages, you can buy big names and turn on Drip to keep the position leveling up, especially if you are just starting or don’t have a lot of capital to start.