If This Is a Bubble, It’s the Most Profitable One in History.

The numbers show a market powered by earnings, not euphoria.

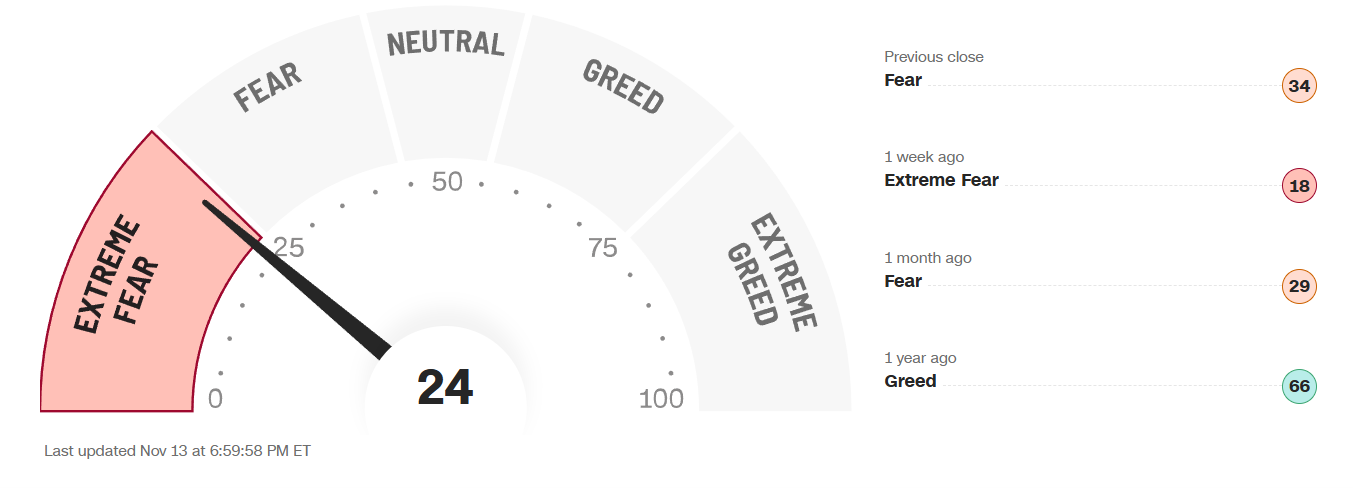

Every time the market climbs to a new high, investors start to panic.

The same word appears again and again.

Bubble.

We heard it in 2013.

We heard it in 2017.

We heard it in 2021.

Now we are hearing it again.

The problem is that the word “bubble” gets repeated so often that people stop looking at the data. They react to headlines instead of underlying business strength. And when fear drives your decisions, you always end up behind those who study fundamentals.

Here is the truth that almost nobody wants to acknowledge. If this is a bubble, it is the most profitable one investors have ever experienced. Corporate earnings have never been stronger. Cash flow is hitting record levels. Balance sheets are healthier than they were five or ten years ago.

The rally we are seeing is powered by revenue growth, rising profits, and real demand. When you track the numbers closely, the picture looks very different from what you hear on financial television or social media. This is why I have become so focused on analyzing my own portfolio using clear, objective data. When you break down fundamentals into simple visuals and trends, fear dissolves. You can see the strength that headlines tend to bury.

And that brings me to the point of this article.

We are not in a bubble. The data proves it.

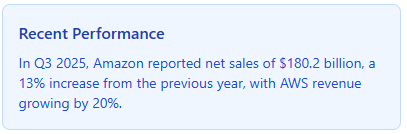

For instance, Amazon $AMZN recently reported a strong earnings report with massive growth across operating segments.

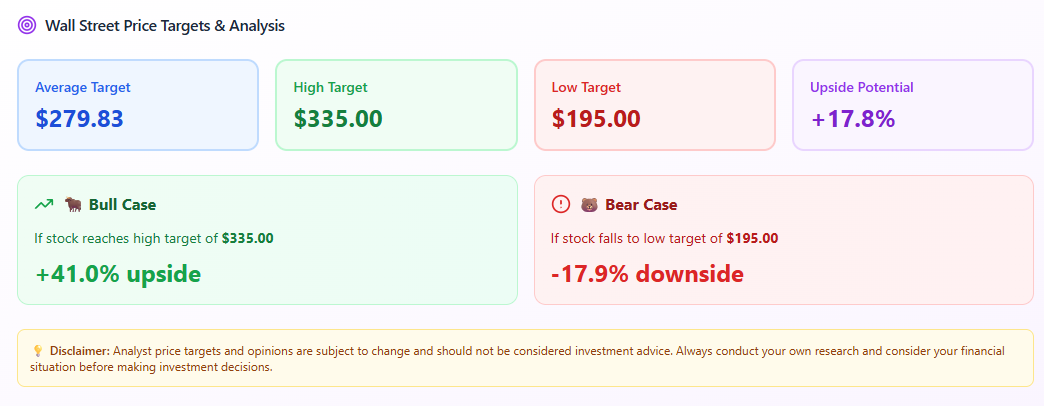

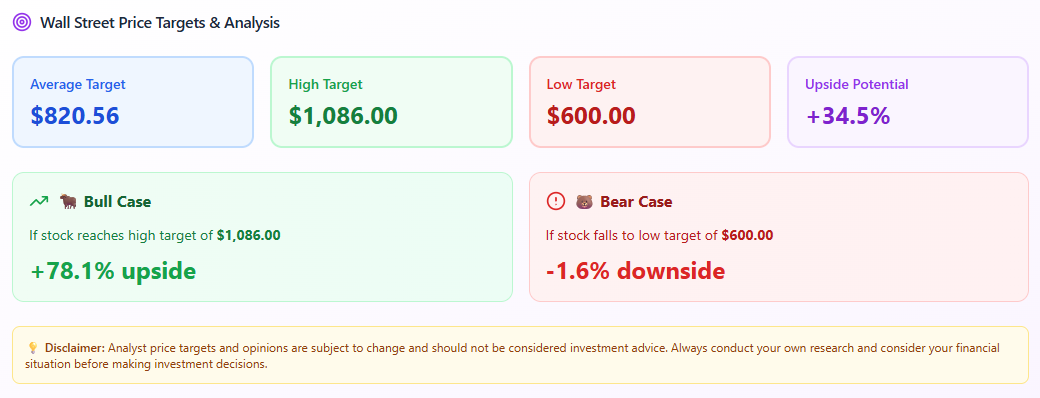

👉 As a result, Yieldly estimates the potential upside outweighs the downside risk.

👉 Access The Yieldly Dashboard At A Discounted Rate! (BLACK FRIDAY DISCOUNT)

The AI Investment Wave Is Creating Real, Measurable Growth

One of the strongest arguments against the idea of a bubble is the scale and quality of corporate investment in artificial intelligence. Companies are spending real money on real infrastructure that is already improving productivity, expanding margins, and unlocking entirely new revenue streams.

Amazon $AMZN

Microsoft $MSFT

Alphabet $GOOG

Meta Platforms $META

Nvidia $NVDA

All of these businesses have collectively committed tens of billions of dollars to AI infrastructure, model training, and data center expansion. These investments are not hopes for the distant future. They are already producing measurable returns.

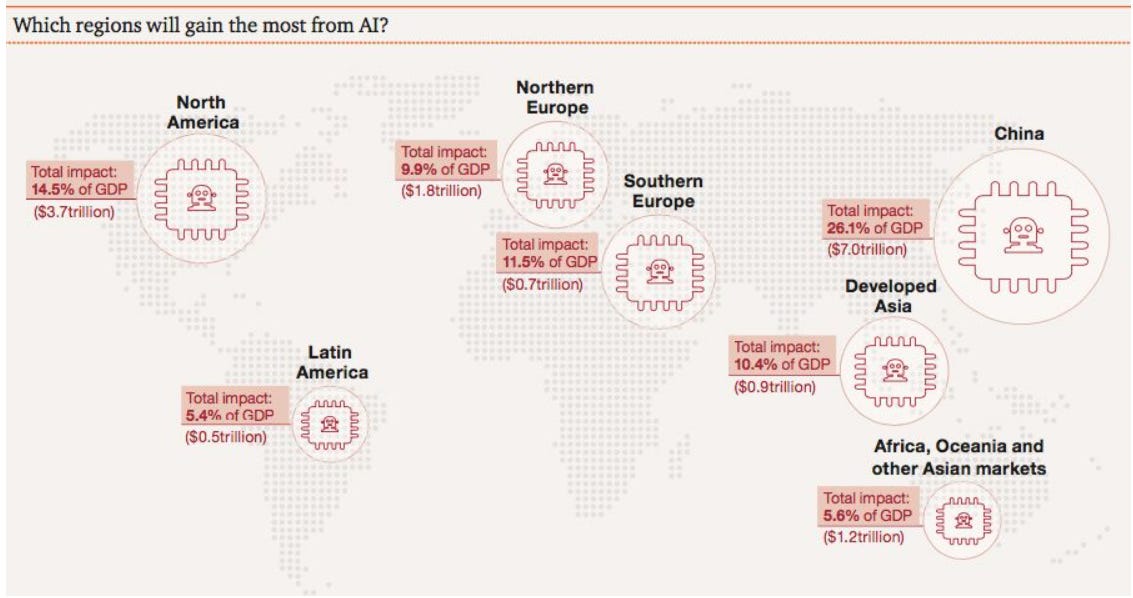

Analysts expect global AI spending to reach more than one trillion dollars annually before the end of the decade. McKinsey estimates that AI could add between 2.6 and 4.4 trillion dollars in annual value to the global economy. PwC projects that AI could add more than 15 trillion dollars to global GDP by 2030. These are not speculative numbers. They reflect real efficiency gains and real improvements in business productivity.

Companies that adopt AI early are already reporting meaningful improvements. Customer service teams can now resolve far more tickets per hour. Software engineers are completing tasks faster with coding assistants. Logistics and supply chain networks can optimize inventory with greater accuracy. Marketing teams are generating more output with fewer people. These changes raise output while lowering costs, which translates into higher margins.

The broader impact is just beginning. AI does not behave like past technology waves that had limited reach. It affects nearly every industry. Healthcare, finance, retail, manufacturing, real estate, transportation, and education are all adopting AI tools that reduce labor intensity and increase precision. This leads to stronger operating performance, which naturally supports higher valuations.

Valuations Look High, But the Market Is Still Fairly Priced

At first glance, the market looks expensive. Prices are at all-time highs, multiples have expanded, and several mega-cap leaders trade at valuations that make people uncomfortable. High prices, however, do not automatically mean overvaluation.

Valuation only becomes stretched when earnings fail to justify the price. That is not the case today. The companies driving this market higher are growing faster than their multiples. Amazon, Microsoft, Alphabet, Meta, and Nvidia all delivered double-digit revenue growth while expanding margins and increasing cash generation. When earnings rise at this pace, the fair value of these companies rises too.

A second misconception is that valuations must return to historical averages. This belief is driven by anchoring bias, which is the tendency to rely on old reference points even when the environment has changed. Investors remember the market trading at lower multiples in the 2000s and 2010s and assume the present must eventually return to those levels. They anchor their expectations to the past rather than evaluating what has changed today.

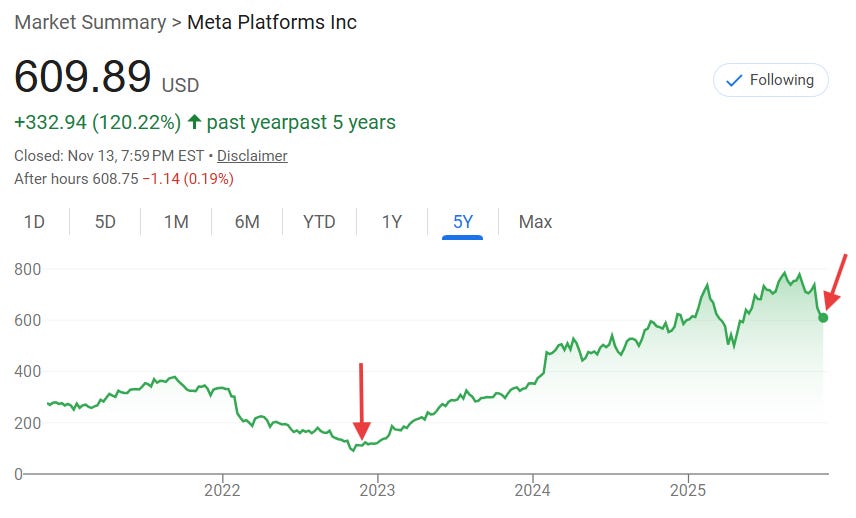

They say things like: ‘Why would I buy META today, when I could’ve bought it at $150 3 years ago?’

But that is irrelevant.

👉 Yieldly indicates that there’s massive upside potential in META right now, based solely on its earnings.

Markets do not price companies based on what they used to be. They price companies based on what they are becoming. Multiples shift when the underlying economics shift. Artificial intelligence is now increasing corporate productivity, lowering operating costs, and creating entirely new revenue streams. Companies are generating more profit from the same level of resources, and this directly raises their intrinsic value.

Anchoring bias causes investors to compare today’s valuations to outdated eras, even though those eras did not have AI-driven efficiency gains, cloud dominance, recurring revenue models, or the current scale of global demand. When businesses become more profitable and more efficient than they were in the previous decade, they deserve higher valuation ranges. Anchoring to old multiples prevents investors from recognizing that the fair value of the market has legitimately increased.

Not ready to upgrade? That’s fine! When you become a free subscriber today, you will gain access to the following:

✅50+ Monthly Dividend Stocks provides a list of tickers that send income to your account every single month.

✅ETFs for Beginners breaks down income focused funds that simplify the investing process.

✅Dividend Legends highlights companies with long histories of increasing dividends through every type of market.

These are tools that will help you get your dividend journey started.

What My Long-Term Projections Show

When you run the numbers using reasonable assumptions, the long-term outlook is far stronger than most investors realize. I am not using aggressive inputs. I am not assuming constant outperformance or unrealistic growth. The projections are built on a simple idea. If earnings remain stable and the market continues to compound at a normal rate, the portfolio moves higher over time.

This is the base case I track.

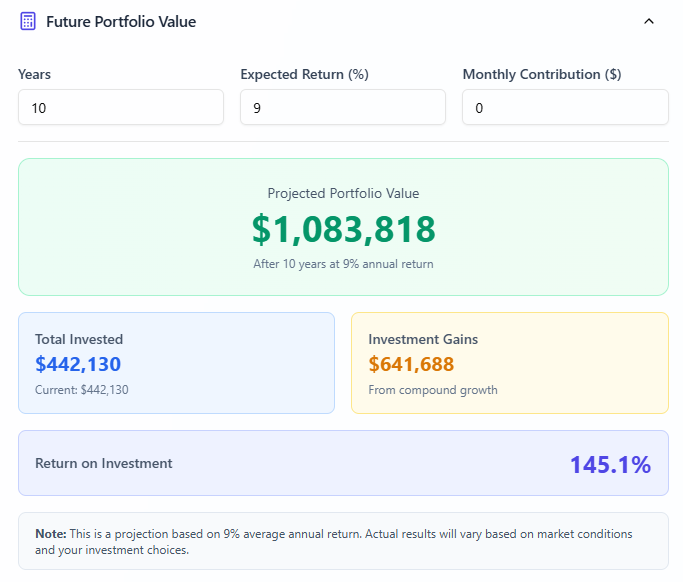

Below is the ten-year projection I use as part of my long-term planning. No monthly contributions. A modest expected return. Nothing extreme. Just the math of compounding in a stable earnings environment.

The projection shows a future value of about $1.08M over ten years, driven mostly by compound gains rather than new contributions. The important point is not the exact number. It is the relationship between current fundamentals and future results. When earnings hold up, the compounding continues. When businesses stay profitable, the long-term math remains intact.

This is why I do not anchor to headlines. I anchor to data. If the companies driving this market continue to grow revenue and expand margins, the long-term return profile remains strong. The projection above reflects that reality.

Conclusion

The bubble narrative feels convincing because fear is always louder than data. But when you strip out the headlines and look only at earnings, margins, productivity, and investment spending, there is nothing in the numbers that resembles a market built on weak foundations.

Companies are generating real cash. They are improving efficiency through AI. They are raising guidance instead of cutting it. They are investing in growth rather than pulling back. These are the conditions that support long-term compounding, not conditions that lead to collapse.

The projection I shared earlier is not a prediction. It is a reminder. When fundamentals hold up, long-term returns remain steady. You do not need to call tops or bottoms. You only need to understand whether the underlying engine of the market is breaking down or strengthening.

Right now, it is strengthening.

That is why the market looks expensive.

Strong businesses deserve higher valuations.

If we were in a bubble, the data would show it. It does not. And until it does, the long-term outlook remains intact.

Focus on the fundamentals, ignore the noise, and let the math do the work.

Thank you for this article!