Insiders are Buying The Dip On Ares Capital (10% Yield)

ARCC’s CEO and CFO just deployed $700k of their own cash. Here is the math behind the 'Gold Standard' of private credit."

The market is currently terrified of a “SaaSpocalypse.” If you believe the headlines, private credit is a bubble and Ares Capital Corp ARCC 0.00%↑ is a software-heavy ticking time bomb. The stock is down nearly 19% from its highs, and retail investors are heading for the exits.

But while the market panics, the insiders are shopping.

Between February 5th and 9th, four ARCC executives—including the CEO and CFO—put over $700,000 of their own personal cash into the stock at $19. I teamed up with Guardian Research on today’s article. If you don’t know them, Guardian Research specializes in contrarian equity analysis — insider buying signals, asymmetric setups, and deep fundamental research across sectors. They came to me with a compelling thesis on ARCC: the insiders are cluster-buying while the market panics over software exposure, and the diversification story is being completely ignored.

Disclosure, I own ARCC and collect more than $1,100 in annual dividend income. This is not a buy recommendation. This is an analysis that highlights the stock’s strengths.

👉 Unlock Access To Yieldly By Upgrading Your Membership. Yieldly allows you to track your monthly dividend income.

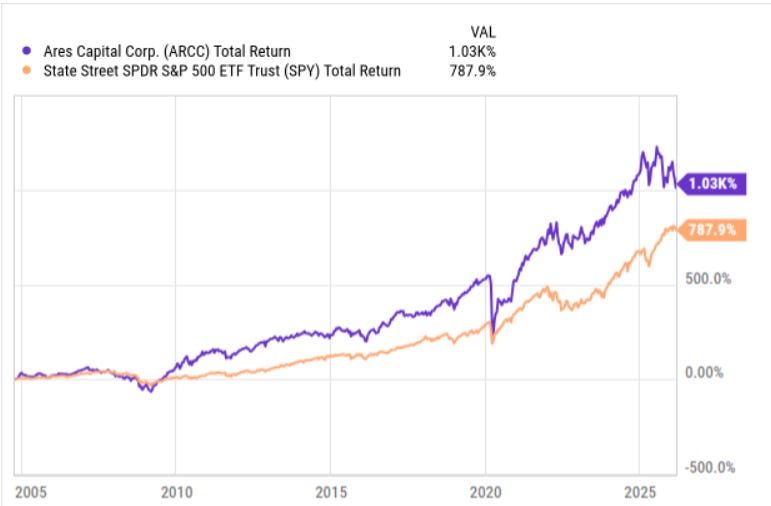

ARCC has historically crushed the S&P 500 SPY 0.00%↑ in total return as well, thanks to its double-digit dividend yield.

1. Insider Buying

Between February 5th and 9th, 2026, four Ares Capital insiders, including the CEO, COO, CFO, and a board director, bought 36,686 shares of their own stock. These were open-market purchases totaling roughly $704,000 of personal capital deployed at an average price of $19.18.

Think about the vantage point of these four individuals. They oversee a $29.5 billion lending portfolio. They sign off on the credit memos for 603 different borrowers.

Meanwhile, the market is panicking. ARCC is down nearly 19% from its 52-week high, trading at a rare 0.95x Price-to-NAV. The narrative in the headlines is clear: Private credit is a bubble, and ARCC’s 24% software exposure is a ticking time bomb. We believe the market has it wrong. By focusing exclusively on a “SaaSpocalypse” that has yet to show up in the actual credit data, investors are ignoring the highest-quality, most diversified income vehicle in the market.

2. Why ARCC is Structurally Superior

For those unfamiliar, a Business Development Company (BDC) is essentially a publicly traded private credit fund. Regulated under the Investment Company Act of 1940, BDCs must distribute at least 90% of their taxable income to shareholders, making them a favorite for income seekers.

ARCC isn’t just another BDC; it is the Gold Standard. Backed by Ares Management ($450B+ AUM), it enjoys a scale moat that smaller peers cannot replicate. In 2025 alone, ARCC reviewed roughly $1 trillion in potential deals, closing on just 1.6% of them. This level of selectivity is why ARCC’s non-accruals (defaults) sit at just 1.2%, compared to the BDC industry average of 3.8%.

3. The Macro: The Structural Retreat of Banks

The rise of private credit isn’t a “cyclical bubble”—it’s a structural shift. Since the 2008 financial crisis, Basel III and Dodd-Frank have forced banks to retreat from middle-market lending due to high regulatory capital charges.

Middle-market companies (doing $100M to $1B in revenue) represent a third of U.S. private sector GDP. They need capital to grow, and private credit providers like Ares have stepped in as the primary lenders. With the “Basel III Endgame” proposals looming, this trend is likely to accelerate, not reverse.

4. ARCC Portfolio Deep Dive

We are not calling a bottom in software. We are saying the risk is priced in, while the diversification is ignored.

The “SaaSpocalypse”: 24% of ARCC is in Software. If AI truly destroys mid-market SaaS economics, ARCC will take hits. However, management’s “Three-Layer AI Defense” focuses on foundational infrastructure (core systems that are too risky to “rip and replace”) and proprietary data moats.

Rate Cuts: As the Fed cuts rates, NII (Net Investment Income) compresses. We saw Core EPS move from $2.33 in 2024 to $2.01 in 2025.

The Counter-Argument: Lower rates make borrowers healthier. It reduces their interest expense and improves their coverage ratios, leading to fewer defaults.

The market is pricing ARCC as if it were a pure-play software fund. It isn’t. 76% of the portfolio has nothing to do with software.

Breaking Down the Non-Software Engine

The 76% of the portfolio that has nothing to do with software is comprised of “GDP-plus” businesses—companies that are essential to the functioning of the U.S. economy and possess significant pricing power.

Healthcare Equipment & Services (11.3%): This is the second-largest vertical. These are high-barrier-to-entry businesses with mission-critical products. In 2025, ARCC’s healthcare borrowers saw organic EBITDA growth that was double the rate of the broader market.

Commercial & Professional Services (9.4%): These companies provide the “plumbing” of corporate America—logistics, facility management, and outsourced compliance. These are recurring-revenue models with extremely high switching costs.

Ivy Hill Asset Management (8.3%): This is ARCC’s wholly-owned “middle-market engine.” Ivy Hill manages its own portfolio of middle-market loans, providing ARCC with a high-yielding, diversified stream of dividend income that outperformed traditional first-lien yields throughout 2025.

The Defensive Core (Insurance, Financials, Industrials): Combined, these sectors represent over 20% of the book. These are “hard asset” or “contracted cash flow” businesses that provide a massive counter-weight to tech sentiment.

Financials: Earnings Are Solid

While the headline Core EPS of $0.50 met analyst expectations, the underlying “engine” of ARCC showed significant activity to offset the Federal Reserve’s rate cuts in late 2025.

ARCC’s Core EPS of $2.01 for the full year 2025 was a decrease from $2.33 in 2024, a direct result of falling base rates affecting its floating-rate portfolio. However, management successfully countered this yield compression through record-breaking origination volume.

Total Investment Income: Rose to $793 million in Q4 2025 (up 4.5% year-over-year).

Fee Generation: Capital structuring service fees jumped to $57 million, fueled by a massive $5.8 billion in new gross commitments during the quarter.

Portfolio Velocity: ARCC exited $4.7 billion in investments in Q4 alone, demonstrating high liquidity and the ability to recycle capital into higher-quality first-lien positions.

The “Institutional-Grade” Funding Advantage

While retail investors often focus purely on a BDC’s dividend, sophisticated analysts look at the liability side of the balance sheet. ARCC’s ability to source cheap, stable capital is its greatest competitive advantage. In 2025, while smaller BDCs struggled with tightening bank credit, ARCC executed a “masterclass” in capital management, adding a record $4.5 billion in new gross debt commitments.

ARCC ended 2025 with over $6 billion in total liquidity, including available cash and massive capacity across its diversified credit facilities. This “dry powder” allowed management to play offense in Q4, committing $5.8 billion to new deals while many competitors were forced to the sidelines.

Credit Facility Strength: ARCC maintains relationships with over 40 banks, expanding its facilities by $1.4 billion in 2025 while actually reducing its borrowing spreads by an average of 20 basis points.

The CLO Engine: In December 2025, ARCC priced its largest-ever on-balance sheet CLO (Ares Direct Lending CLO 8) at $700 million, securing long-term financing at a blended cost of SOFR + 147 bps. This diversified funding mix reduces reliance on any single market.

5. The Dividend: Best-in-Class Payout

For the income-focused investor, the dividend isn’t just a “feature”—it is the entire thesis. At a price of $18.99, ARCC’s 10.1% yield is no longer just “attractive”; it is effectively pricing in a level of distress that the underlying credit data simply doesn’t support.

To understand why this payout is the “Gold Standard,” we have to look past the yield and into the structural plumbing of the distribution.

The Coverage Ratio: $0.09 of “Breathing Room”

ARCC currently pays a quarterly base dividend of $0.48 ($1.92 annualized). In Q4 2025, the company generated Core EPS of $0.50. This results in a 108% coverage ratio. While a 108% margin might seem thin to an equity investor used to Apple or Microsoft, for a BDC—which is legally required to distribute almost everything it earns—this is a healthy cushion. It means that even after paying out one of the highest yields in the S&P 500 ecosystem, ARCC is still “over-earning” its dividend by $0.09 per share annually, which is retained to bolster Net Asset Value (NAV).

The “Spillover” Safety Net: $988 Million in Reserve

The most misunderstood aspect of ARCC is its Taxable Spillover. Because the IRS requires BDCs to distribute 90% of taxable income, any excess income earned during “boom” years is carried forward on the balance sheet.

Estimated 2026 Spillover: $988 million ($1.38 per share).

The “Zero-Earnings” Buffer: If ARCC’s earnings theoretically dropped to zero tomorrow, management could continue to cut a $0.48 check for nearly three full quarters using only this accumulated “spillover” cash.

This is the ultimate insurance policy. While peers like Blue Owl OBDC 0.00%↑ or FS KKR FSK 0.00%↑ have navigated choppy coverage in the past, ARCC’s spillover allows it to maintain a rock-solid payout even if the Fed aggressively cuts rates or if the “SaaSpocalypse” causes a temporary spike in non-accruals.

6. Valuation: The Math Works at $19

Valuing a BDC is fundamentally different from valuing a tech stock. You aren’t paying for “future dreams”; you are buying a pool of existing loans. The most honest metric of value is the Price-to-NAV (Net Asset Value) ratio—essentially, are you paying more or less than the literal cash value of the loans on the books?

Historically, ARCC is a “premium” BDC. Because of its scale and low loss rates, investors typically pay 1.05x to 1.10x NAV to own it. As of March 2, 2026, the script has flipped:

Current Price: ~$18.99

Net Asset Value (NAV): $19.94

Price-to-NAV: 0.95x

For the first time in nearly two years, you can buy the world’s largest private credit portfolio at more than a 5% discount to its NAV. The market is effectively saying that 5% of ARCC’s loans are “bad” or will disappear. However, with non-accruals at a measly 1.2%, the math suggests the market is pricing in a catastrophe that hasn’t happened.

Conclusion: A Rare Entry Window

Guardian Research: The insider cluster-buy is the ultimate “tell.” When the C-suite buys $700k of stock while the market panics over headlines, the asymmetric risk/reward favors the patient investor.

TheGamingDividend: From an income perspective, the combination of 108% dividend coverage and a $1.38/share spillover makes this one of the safest double-digit yields available.

Enjoyed this deep dive? I share institutional-grade research and dividend analytics like this frequently. Join 5,000+ investors and get the next one delivered straight to your inbox.

| A guest post by

|