Meta & Microsoft Are Both Cheaper than the S&P 500 (And I’m Buying)

MSFT showing 55% upside and META priced like a slow-growth utility. Generational Buying Opportunity.

Wall Street is panicking because big tech is spending billions on AI hardware, and they don’t see the immediate “payoff” yet. They see a money pit; I see the best buying opportunity of the decade.

I’m not interested in standing on the sidelines while the market wait-and-sees. While institutional investors hesitate, I am using the cash flow my portfolio already generates to secure my stake in the companies building the digital backbone of the next century. While the market frets over short-term costs, I am looking at long-term dominance.

I’m putting my money where my mouth is. Using the cash flow my portfolio is already generating, I am moving $8,000 more into Meta META 0.00%↑ and $4,000 more into Microsoft MSFT 0.00%↑.

I wanted to highlight some interesting points on why I believe MSFT and META are undervalued right now. I will cover the following:

Growth Catalysts

Price Targets

Earnings Metrics

Valuation

Valuation: March 2026 Snapshot

Before we dive into the specific analysis, let’s look at the numbers. The primary reason I am adding to these positions now is that the recent sell-off has pushed their valuations to levels that, quite frankly, make the rest of the market look expensive. Some of these companies trade at their lowest multiples over the last few years.

Meta is currently trading cheaper than the average S&P 500 stock, despite having significantly higher margins and growth potential. Microsoft is trading at its lowest forward multiple in three years. When you can buy the world’s best business models at a discount to the "average" company, you take it.

Microsoft (MSFT): Scaling the AI Utility

Wall Street is panicking over a tiny, 1% drop in growth for Microsoft’s MSFT 0.00%↑ cloud business. They are obsessing over a small detail while ignoring the fact that the company is actually getting much stronger.

Over the last six months, MSFT has declined by more than 18%.

The Yieldly Dashboard pulled in analyst data and states that there is an average upside potential of 55.3%. from the current levels.

👉 Unlock Access To Yieldly By Upgrading Your Membership. Yieldly allows you to track your monthly dividend income and operates as a universal stock search tool.

1. The $625 Billion Pre-Paid Tab

Microsoft’s $625 billion backlog is the ultimate safety net. While most mega-cap companies struggle to grow their contract base by 15%, Microsoft’s surged 110% in one year. This means even if they didn’t sign a single new customer, they have over half a trillion dollars in revenue already scheduled to hit the bank.

A huge chunk of this—about $281 billion—comes from long-term commitments from AI leaders like OpenAI and Anthropic. These companies are now effectively locked into Microsoft’s infrastructure for years, creating a massive revenue floor that protects the stock from market downturns.

This backlog also explains why Microsoft is comfortable spending $37.5 billion on hardware in a single quarter. They aren’t building data centers on a hunch; they are building them to fulfill contracts that are already signed. With an average contract length of 2.5 years, this $625 billion ensures a steady stream of cash for dividends and buybacks. Microsoft has already sold its future production. Now they just have to collect the checks.

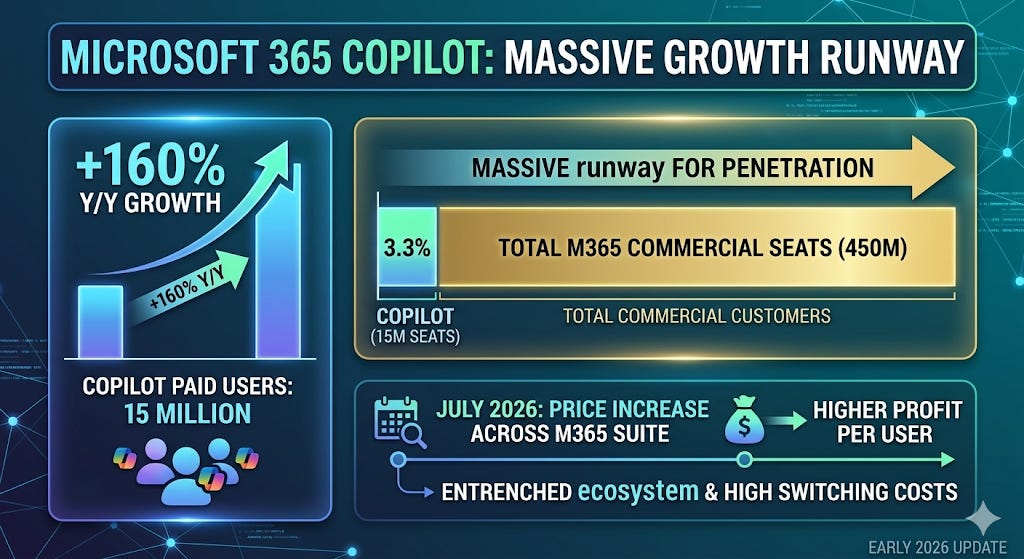

2. Copilot is Just Getting Started

Microsoft 365 Copilot just hit 15 million paid users. While that is a 160% increase from last year, it only represents about 3% of Microsoft’s 450 million total commercial customers. This tiny penetration rate shows the massive runway still ahead.

As more companies integrate these tools into their daily workflows, the switching costs become insurmountable. Once an enterprise automates its operations with Copilot, moving to a competitor is too expensive and disruptive. Microsoft is also set to raise prices across its suite in July 2026. This allows them to extract more profit from every single user in an ecosystem they already dominate.

3. Building Their Own Tech

The Maia 200 AI chip is designed specifically to run massive AI models like those found in Copilot and Azure. By using its own silicon, Microsoft can reduce the “Total Cost of Ownership” for its AI servers by more than 30%.

The Cobalt 200 CPU handles the general computing tasks that support AI. It delivers up to 50% better performance than the previous generation of chips. Because these chips are more energy-efficient and powerful, Microsoft can pack more computing power into the same data center space. This allows them to lower the cost of every “AI answer” provided to a customer, which directly increases their profit on every subscription sold.

This shift turns Microsoft into a digital utility. Just as a power company owns the generators and the wires, Microsoft now owns the chips, the servers, and the software.

By verticalizing the entire stack, they are no longer just a software vendor. They are the essential infrastructure that other companies must rent to exist in the AI era. This transition locks in their competitive advantage for the next decade because competitors who don’t own their own silicon will struggle to match Microsoft’s pricing and efficiency.

Meta Platforms (META): The Silent AI Standard

Meta Platforms META 0.00%↑ is my highest conviction play. My current position is just over $30,000, and I am adding $8,000 more. The market is missing the fact that Meta is no longer just a social media business. It has become an AI infrastructure powerhouse that owns the most valuable data set on earth.

While the market obsesses over the $115 billion to $135 billion in capital spending for 2026, they are missing a massive structural shift. Meta has pivoted from a social app company to an industrial-scale AI utility, building the foundational machinery that will run the next decade of digital commerce.

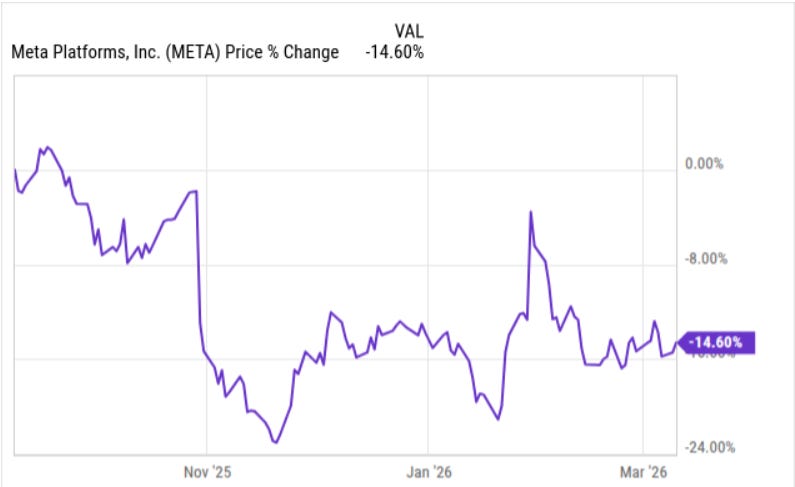

META has fallen by more than 14% over the last 6 months.

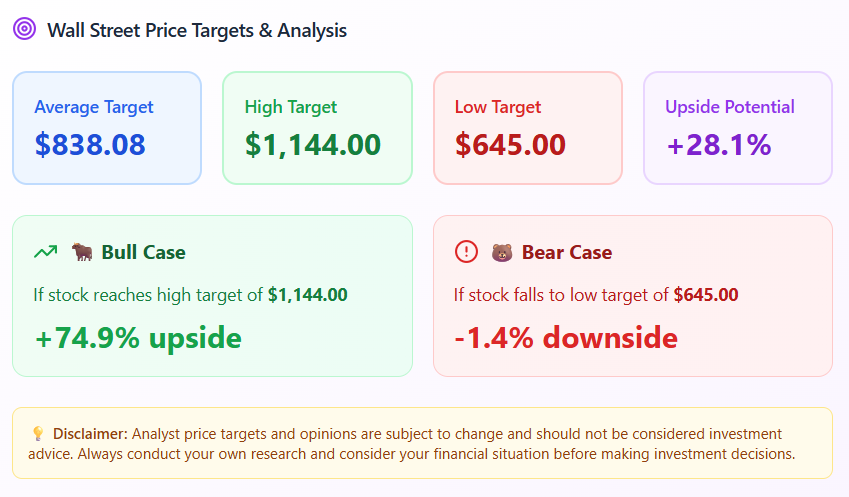

👉 Yieldly compiled analyst data and the upside severely outpaces the risks. META has a an average potential upside of 28.1%, while the downside sits around 1.4%

Turning Data into an Ad Printing Machine

Meta is hitting a rare financial “sweet spot” where both the volume of its ads and the price of those ads are rising simultaneously. In the most recent quarter, ad impressions grew 18% due to a surge in engagement from AI-recommended content like Reels and Threads. Typically, such a massive increase in inventory would cause prices to drop, but Meta actually saw a 6% increase in the average price per ad. This happened because their new AI engine, Andromeda, has become so accurate at predicting user intent that every individual ad is now more likely to lead to a sale, allowing Meta to charge a premium for every “eyeball” they provide.

The efficiency is now being driven by Advantage+ and Andromeda, which have automated the entire sales funnel. Advertisers are seeing a 24% increase in conversions because the AI is no longer just “guessing” who might click; it is using real-time data from 3.5 billion users to find the exact person ready to buy. By removing manual targeting and replacing it with machine learning that is 87% accurate at predicting outcomes, Meta has lowered the cost of acquiring a customer for brands by over 30%. This is creating a powerful flywheel: better ad performance brings more advertiser spending, which gives Meta more data to train the AI, making the entire platform even more profitable.

The Android of AI Strategy

Meta is making its Llama AI models open source. This is a brilliant move to destroy the pricing power of rivals like OpenAI. By giving the tech away for free, Llama is becoming the default choice for developers worldwide. This turns Meta into the unofficial operating system for AI. The more people use Llama, the more Meta learns and the harder it becomes for anyone to catch them.

The next step is the integration of Manus AI agents into WhatsApp. This is a massive new revenue stream. Soon, millions of small businesses will have automated Meta AI agents closing sales 24/7. Meta will not just collect ad fees. They will likely take a cut of every transaction those agents facilitate.

The Best Deal in Tech

Meta is currently the best-valued AI play in the market because it is being priced like a slow-growth utility while delivering the numbers of a high-growth tech leader. At roughly 22x forward earnings, it is trading at a lower multiple than the average S&P 500 company (currently 23.6x). It is also the cheapest of the Magnificent 7 alongside Nvidia, despite Meta having a more direct and proven path to monetizing AI through its 3.5 billion daily users.

The path to $1,000 per share by 2028 is driven by a massive “earnings catch-up.” Meta is currently in a heavy investment phase, spending up to $135 billion this year on the hardware needed to run the next generation of AI. As this infrastructure matures, the massive depreciation costs will level off while the revenue from AI-driven ads and WhatsApp commerce continues to scale. With analysts already projecting EPS to climb toward $40 by 2028, even a modest market multiple of 25x would put the stock at four figures. You are essentially buying the world’s most advanced AI lab at a bargain-bin valuation.

My Positioning Strategy

As you can see from my dashboard, my total annual income is now north of $42,000. This cash flow gives me the “dry powder” to ignore short-term volatility and buy these dips while others are fearful.

The Plan:

META: Adding $8,000. Chasing the massive upside in their “Family of Apps” and the future of AI commerce.

MSFT: Adding $4,000. My “Fortress” play—the most stable, high-margin growth engine in existence.

I don’t care about the noise. I care about who owns the future. Right now, that’s Microsoft and Meta.

What about Amazon?