Reddit Is Secretly An AI Company. Here's What RDDT Is Worth.

Why AI models can't stop citing Reddit, and what that's worth to shareholders.

Did you know that when you ask ChatGPT or Google’s AI something and it answers with actual confidence, there is a good chance it learned that answer from some random Reddit thread? Not a research paper. Not a news article. A comment some guy posted at 2am about his lawnmower breaking down.

I went down a rabbit hole on this and it turns out it is not a fluke. AI visibility trackers show Reddit getting cited in AI-generated answers roughly three times as often as Wikipedia.

Three times.

Wikipedia has been the internet’s fact-checking backbone for two decades, and Reddit just lapped it because AI models want real human opinions, not polished encyclopedia entries.

As an investor, that stopped me in my tracks. Reddit stumbled into a second business hiding inside the first one. Ads still pay the bills today, but the data licensing angle is what made me actually want to dig into this stock.

How Reddit Makes Money

Reddit RDDT 0.00%↑ makes money two ways.

Advertising is the larger piece and it behaves like a normal internet ad business, tied to impressions, pricing, and how well the company can target intent.

Data licensing is the smaller piece and it behaves like a royalty stream, where AI companies pay Reddit for access to its corpus of human conversation.

The first business funds today. The second business is what the market is trying to price for tomorrow.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor.

Q1 2026 Earnings

Reddit’s daily active unique users grew 17% year over year to 126.8 million in the first quarter of 2026. Revenue climbed 69% year over year to $66M, with net income of $204M, representing a 31% net margin. That is extremely impressive numbers here, considering most people don’t even know how they make money.

Diluted EPS landed at $1.01, which analysts pegged as a beat of somewhere between 63% and 74% depending on which consensus estimate you use. I care less about the exact beat percentage and more about the trend line underneath it. This marks the third straight quarter of meaningful outperformance, and management has now delivered seven consecutive quarters of revenue growth above 60%.

Guidance for the second quarter calls for revenue between $715M and $725M, with adjusted EBITDA between $285M and $295M. Both figures sit ahead of where analysts had modeled the quarter before the print.

Valuation

As of this week, RDDT trades around $200 per share, putting the market cap at roughly $37.5B on about 192.5 million shares outstanding. The stock is down meaningfully from its 52-week high near 283 dollars and well above its 52-week low near 119 dollars, which tells you plainly how volatile the sentiment swings have been on this name over the past year.

A PEG ratio under 1 usually signals that growth is undervalued relative to the multiple being paid, and that is the core bull argument here. A 37 times forward earnings multiple looks expensive in isolation, but next to a company still compounding revenue near 70% a year and expanding margins at the same time, it reads differently.

Free cash flow over the trailing twelve months sits around $869M against essentially no debt, which gives management room to keep reinvesting without touching the balance sheet.

Wall Street’s average price target sits somewhere between 225 and 235 dollars depending on the source, which implies meaningful upside from current levels. The consensus rating leans Buy.

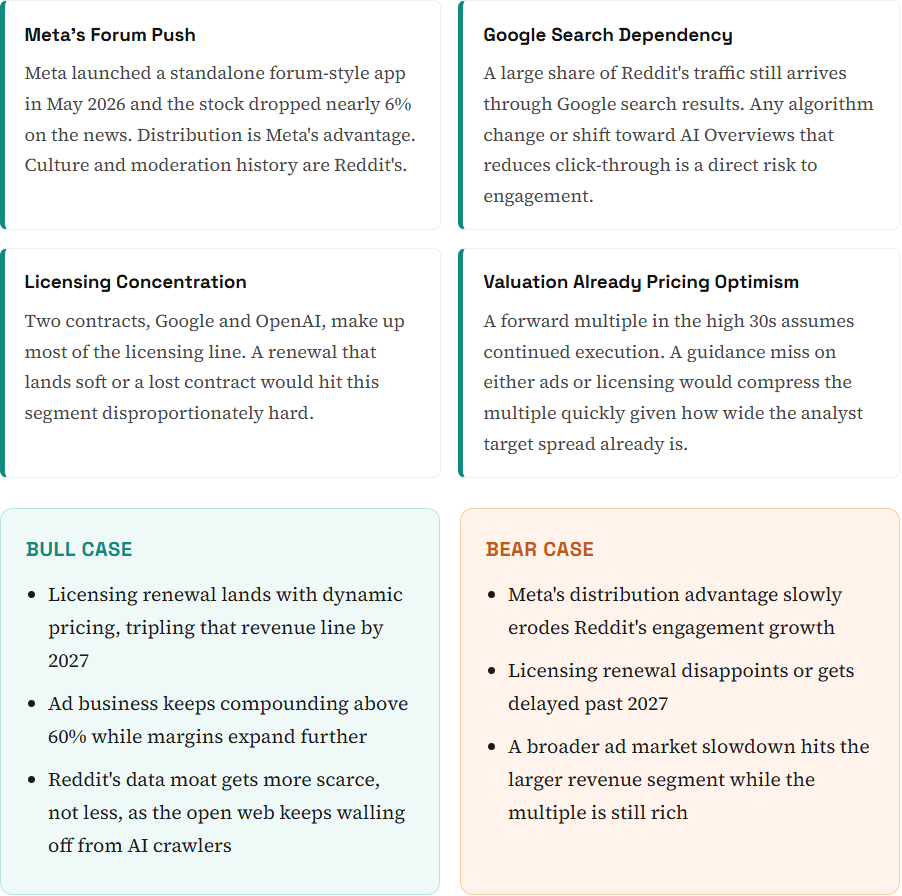

But I want to flag something that does not show up in a single headline number: the spread between the most bearish and most bullish price targets on this stock is one of the widest in large cap internet, with bear cases near 75 dollars sitting next to bull cases above 300 dollars.

My read: the multiple is not cheap on a trailing basis, but it is not disconnected from the growth rate either. This is a stock where the AI licensing renewal outcome in 2027 will likely do more to justify or destroy the current valuation than anything happening in the ad business this year.

The AI Licensing Business

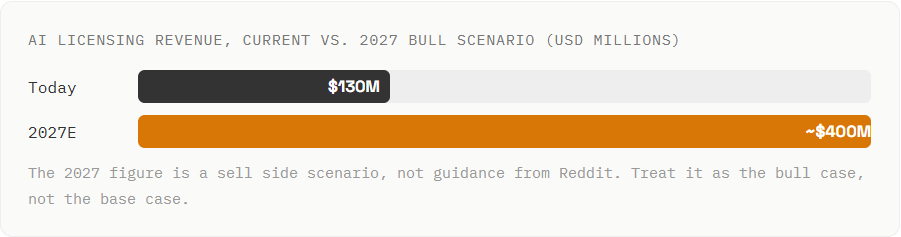

This is the part of the thesis that gets the most hype and the least clarity, so let me lay out what is actually known. Reddit’s existing licensing agreements with Google and OpenAI together generate somewhere around $130M a year, which is roughly 10% of total revenue.

The Google deal was struck near 60 million dollars annually

OpenAI deal near 70 million dollars annually.

Those contracts come up for renewal in 2027, and management has been explicit on earnings calls about wanting to move away from flat annual fees toward usage-based, dynamic pricing, where Reddit gets paid more as its data proves more essential to the answers a model gives. CEO Steve Huffman has argued that every variable has changed since the original deals were signed.

International ARPU Gap

ARPU = Average Revenue Per User

Reddit’s user base is now majority international, but its revenue is not. International daily actives grew 26% year over year to 73 million in Q1, while international revenue jumped nearly 75% to 138 million dollars on the back of international ARPU rising 51% to 2.02 dollars. Compare that to US ARPU of 9.63 dollars in the same quarter and the gap becomes the whole story.

Management has been explicit that international ARPU does not need to match US levels to matter. It just needs to keep closing the gap. Live machine translation now covers 30 languages, and Huffman has pointed to markets like the UK, Germany, and France as places where Reddit is growing daily actives faster than the overall platform average. This is the slowest-moving catalyst on this list, but it is also the one with the longest runway.

Search And Retention

A large share of Reddit’s traffic still arrives through Google search, which is both an opportunity and the risk I flag later in this piece. Reddit’s response has been to build its own on-platform search and answer tools, aiming to keep users inside Reddit for the follow-up questions that used to send them back to Google. Every query that resolves on Reddit instead of bouncing to a search engine is a query Reddit can eventually monetize directly, whether through ads or through a future AI product of its own.

My buddy Jimmy Investor also brought up a good point. META 0.00%↑ can easily copy Reddit’s ecosystem at some point.

2027 Licensing Renewal

I covered the mechanics of this earlier, but it belongs in the catalyst list because of the scale of the potential outcome. The existing Google and OpenAI deals generate roughly 130 million dollars a year combined today. Management is negotiating for usage-based, dynamic pricing on the 2027 renewal, and at least one sell side estimate has modeled this line reaching close to 400 million dollars annually if the renegotiation lands well.

Stack all four catalysts together and the pattern becomes clear. Three of them, international ARPU, ad stack efficiency, and search retention, are already showing up in the reported numbers every quarter. The fourth, the licensing renewal, is a binary event still more than a year away. That is why I keep coming back to the same conclusion: the first three justify the growth investors are already paying for, and the fourth is the one that could justify the multiple.

Risks

Where I Land

I am not going to hand you a price target and call it a day. What I will say is this. Reddit has become one of the few internet businesses that gets paid twice for the same content, once through ads and once through licensing. That is a rare setup, and it is the reason I keep this name on my watch list even at a premium multiple.

The next 18 months come down to two things. Does advertising keep compounding while Meta’s competing product ramps up, and does the 2027 licensing renewal actually reprice the data business the way management is signaling. I will be tracking both closely in future updates, alongside how this fits next to the income names I already hold.

This is not investment advice. I hold positions in various dividend and income names discussed elsewhere on Dividendomics, and my views on RDDT are observational, not a recommendation to buy or sell. Do your own research and size any position to your own risk tolerance.

Funding The Position With The Wheel

RDDT does not pay a dividend, so it will never sit in my portfolio the way a covered call ETF or an MLP does. But that does not mean my income strategy has nothing to do with it. Here is how I think about using the wheel to build a position in a name like this without writing a fresh check.

The wheel works in two stages. First, I sell cash-secured puts on RDDT at a strike below the current price, funded with cash that is already sitting in the account from dividend and distribution income. If the stock stays above my strike, I keep the premium and repeat the process. If it drops below my strike, I get assigned shares at an effective cost basis lower than where the stock traded when I sold the put, since the premium collected reduces my basis.

Second, once I own shares, I start selling covered calls against the position at strikes above my cost basis. That generates ongoing premium income on top of any price appreciation, and it turns a non-dividend payer into something that behaves a lot more like the income names I already track.

The part I want to be direct about: this only works with cash I am comfortable losing to assignment, and RDDT's volatility cuts both ways. Higher volatility means richer premiums on both the puts and the calls, but it also means bigger swings against me if I get the strike wrong. I fund this approach with income already generated elsewhere in the portfolio, not with new capital, which is the same rotation logic I laid out in my last income report.

Frequently Asked Questions

Is Reddit stock a buy in 2026?

Wall Street consensus currently leans Buy with an average price target above the current share price, though the range of individual targets is unusually wide. The decision depends heavily on how you weigh the 2027 AI licensing renewal against the current premium valuation.

How much money does Reddit make from AI companies?

Reddit’s existing licensing agreements with Google and OpenAI generate roughly 130 million dollars combined per year, close to 10% of total revenue. Both contracts are up for renewal in 2027.

Why do AI models cite Reddit so often?

Reddit’s threads capture authentic human conversation and firsthand experience in a way polished articles do not, which makes the content valuable for training and for grounding AI answers in real opinions.

What is Reddit’s biggest risk as a stock?

Competition from Meta’s new forum app and Reddit’s continued dependence on Google search traffic are the two risks most likely to show up in engagement numbers before they show up in earnings.

Never realized how many people used Reddit for info. More than Google sometimes. great analysis

Great analysis, my friend!!! It’s a pleasure to be able to contribute to the discussion in some way.