Tech Earnings Roundup: The AI Infrastructure Supercycle Arrives

Why Big Tech’s Record CapEx is a Generational Buying Opportunity, Not a Bubble.

The Q1 2026 earnings season has officially marked the end of the “AI hype” phase and the beginning of the AI Execution Era. For investors, the narrative has shifted. It is no longer enough for Big Tech to show flashy demos; the market is still scrutinizing the massive capital expenditure (CapEx) required to build the world’s new digital backbone.

While headlines may focus on “skyrocketing costs,” a closer look at the numbers of the latest earnings reports reveals a powerhouse trend: demand is finally catching up to capacity.

I’ve been pounding on the table that this would be the case.

From Amazon’s record-shattering cloud backlog to Microsoft’s triple-digit AI growth, the “Big Four” are proving that their multi-billion dollar bets are beginning to yield tangible, high-margin results.

In this edition, we’ll break down:

The Cloud Re-acceleration: Why AWS, Azure, and Google Cloud are all seeing a “second wind.”

The CapEx Debate: Is the $200B+ spend a risk or a necessary moat?

The Efficiency: How AI is being used internally to protect margins.

My Outlook: Why we’re going much higher.

Bloom Energy Update: >140% return since buy alert was issued.

Amazon (AMZN): The Cloud Re-Acceleration and the $364B “Wall”

Amazon AMZN 0.00%↑ delivered a powerhouse quarter that effectively silenced skeptics who thought AWS was maturing into a slow-growth phase. Management’s message was clear: AI is the new fuel for the cloud. I combed through the latest earnings report and here are the highlights that I find most notable.

Key Highlights:

The AWS Re-Acceleration: Cloud growth accelerated to 28% year-over-year, reaching a $150 billion annualized revenue run rate. This is the fastest growth rate Amazon has reported in 15 quarters.

The Backlog: Perhaps the most “bullish” data point was the AWS backlog, which hit $364 billion (up from $244 billion last quarter). Even without including the recently announced Anthropic deal, this represents massive, multi-year commitments from 80% of the Fortune 100.

Operating Efficiency: Despite heavy spending, worldwide operating income hit $23.9 billion, resulting in a record 13.1% operating margin.

Project Leo: Amazon is moving aggressively into satellite connectivity, confirming a partnership to power services for iPhones and Apple Watches. This isn’t just a science project; management expects it to be a “many billion-dollar revenue business.”

CEO Andy Jassy addressed the “CapEx elephant in the room” head-on. While memory and component costs are “skyrocketing,” Amazon is leaning into its custom silicon, Trainium, to mitigate costs. Jassy noted that Trainium could save the company “tens of billions of dollars” in CapEx each year and provide a massive operating margin advantage over competitors who rely solely on external chips, like Nvidia NVDA 0.00%↑.

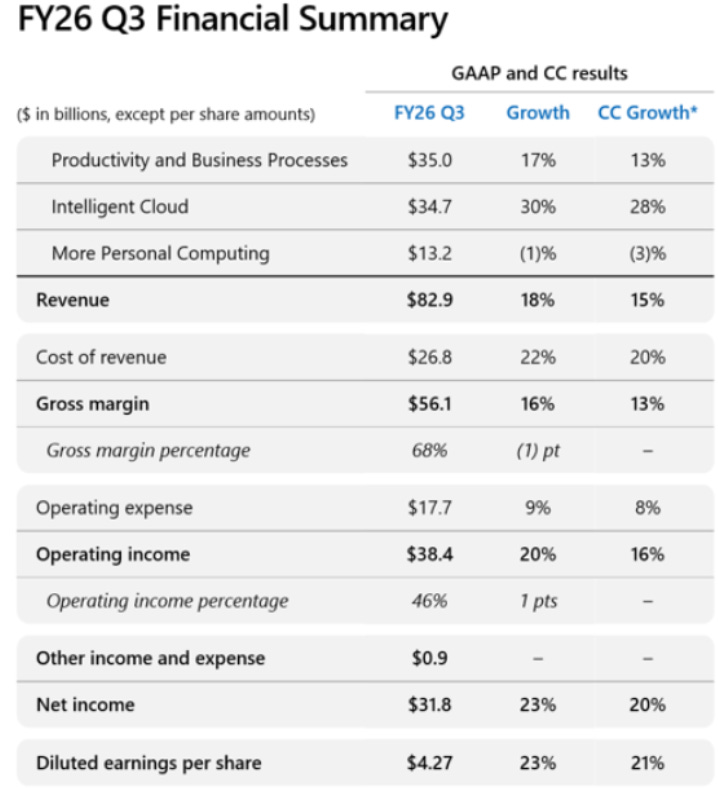

Microsoft (MSFT): AI Demand Outstripping Supply

Microsoft’s MSFT 0.00%↑ Q3 2026 report (Fiscal Q3) reinforced its position as the clear leader in AI monetization. While some investors flinched at the scale of infrastructure spending, the underlying data shows that Microsoft isn’t just spending money, it’s struggling to keep up with an explosion in customer orders.

Key Highlights:

The Big Beat: Revenue hit $82.9 billion (up 18% YoY), comfortably ahead of analyst estimates. Net income rose 23% to $31.8 billion.

Azure Acceleration: Azure and other cloud services grew 40% year-over-year. Crucially, management noted that AI services are contributing a growing percentage of that total growth.

The $37B AI Run Rate: In one of the most significant disclosures of the quarter, CEO Satya Nadella revealed that Microsoft’s AI business has already surpassed a $37 billion annual revenue run rate, up a staggering 123% YoY.

Copilot Adoption: Microsoft 365 Copilot continues to scale rapidly, now surpassing 20 million paid seats.

CFO Amy Hood made it clear that Microsoft is “moving aggressively” to add capacity. The company added another gigawatt of power capacity this quarter alone and is on track to double its data center footprint in just two years.

While the market focused on a projected $190 billion in 2026 CapEx, the “bullish” reality is that Microsoft’s commercial backlog (RPO) surged 99% YoY. They are building data centers to fulfill signed contracts.

Alphabet (GOOGL): A Real Contender

Alphabet’s GOOG 0.00%↑ Q1 2026 report silenced the bears with a performance that proved Search is thriving while Google Cloud has officially matured into a primary growth engine.

The $20B Milestone: Google Cloud revenue surged 63% year over year to $20 billion, marking its first time crossing that quarterly threshold. More importantly, operating income for the cloud segment nearly tripled to $6.6 billion, with margins expanding to 32.9%.

The $460B Backlog: In a stunner, the Google Cloud backlog nearly doubled sequentially to $462 billion. Management noted that roughly 50% of this is expected to convert to revenue in the next 24 months, providing a massive multi year visibility floor.

Search Resilience: Despite fears that generative AI would cannibalize traditional search, Search and Other revenue grew 19% to $60.4 billion. CEO Sundar Pichai noted that “AI Mode” and AI Overviews are driving query volumes to record highs.

Subscription Scale: Alphabet now has 350 million paid subscribers across YouTube, Google One, and its Gemini-powered AI plans. This is a strong signal that consumers are willing to pay for premium AI integration.

Sundar Pichai leaned into the “full stack” advantage. Alphabet is now processing over 16 billion tokens per minute via its first party models, which is up 60% sequentially. While they are currently “compute constrained,” management raised their full year 2026 CapEx outlook to the $180B to $190B range. They are betting heavily that their custom TPU (Tensor Processing Unit) hardware will eventually offer a cost structure their competitors cannot match.

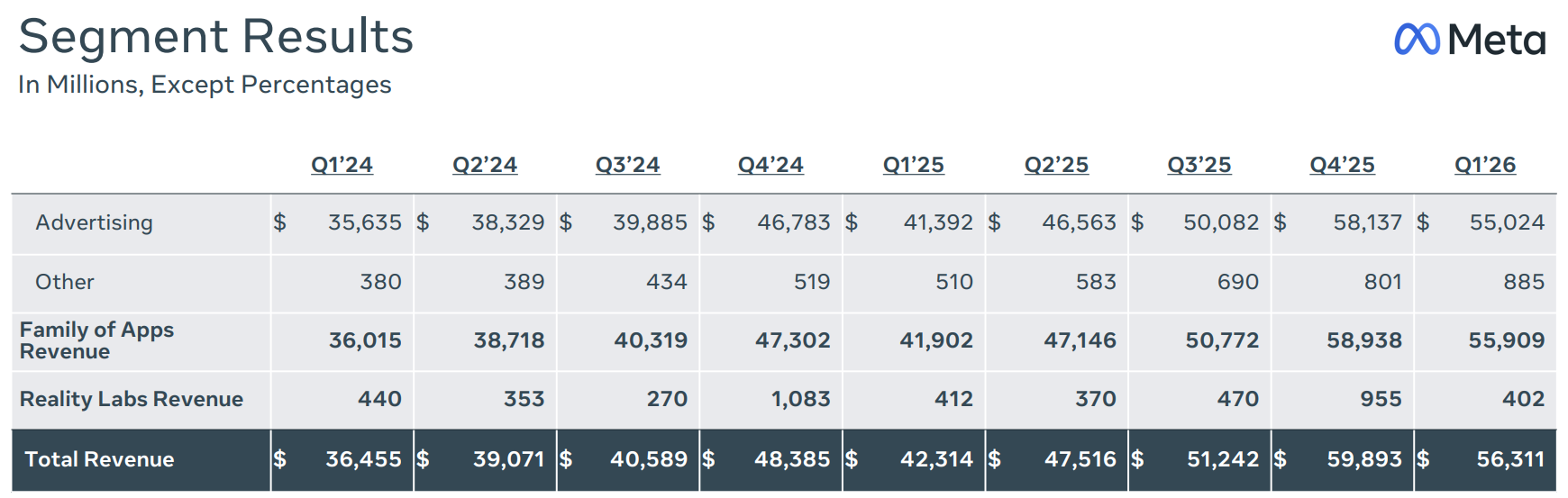

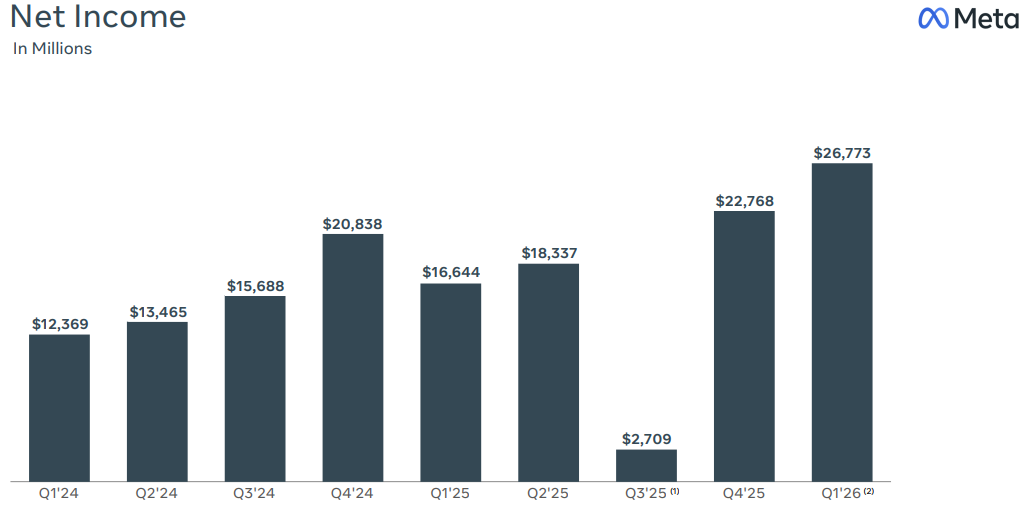

Meta (META): The Engagement Machine Hits Overdrive

Meta META 0.00%↑ delivered a masterclass in how to use AI to squeeze more value out of an existing user base. While they are not selling cloud infrastructure to other companies, they are using AI to make their own digital real estate significantly more profitable.

Key Highlights:

The Big Earnings Beat: Meta reported an EPS of $10.44, far exceeding the $6.65 analyst forecast. Revenue hit $56.3 billion, up 33% year over year.

AI Driven Engagement: More than 40% of the content users see on Instagram is now recommended by AI. This shift has fundamentally changed the engagement math, helping ad impressions grow 19% worldwide.

Pricing Power: The average price per ad increased 12% year over year, showing that advertisers are willing to pay more for the improved targeting and performance driven by Meta’s new AI models.

Agentic Commerce Growth: The release of “Muse Spark” and other agentic tools led to a tenfold increase in weekly business conversations. This signals a new era of automated commerce on WhatsApp and Messenger.

Wearables Momentum: Daily active users of Ray-Ban Meta smart glasses tripled year over year, proving that Meta is successfully moving from social media into AI hardware.

Mark Zuckerberg acknowledged that the company previously underestimated its compute needs. Consequently, Meta raised its 2026 capital expenditure guidance to a range of $125B to $145B. Despite this massive spend, Meta generated $12.4 billion in free cash flow this quarter. Management remains confident that the efficiency gains from their “Muse” models will continue to support high operating margins even as they build out the next generation of AI infrastructure.

Bloom Energy (BE): Powering the Digital Age

Keep reading with a 7-day free trial

Subscribe to Dividendomics to keep reading this post and get 7 days of free access to the full post archives.