The 37% Dividend Yield: How to Generate a 'Second Paycheck' Every Friday

Tax-Free Dividends? $10,000 Invested = $3,700 In Dividends!

We are often taught to invest for a “someday” that is decades away. We are told to bury our money in growth funds and wait for retirement to enjoy the fruits of our labor. But true financial freedom isn’t about having a pile of cash at age 65—it’s about having cash flow today.

Imagine if your portfolio paid your rent, your grocery bill, or your car payment every single week. A reliable, high-frequency income stream buys you two things that are more valuable than a high credit score: peace of mind and autonomy. I wanted to provide some insights into a fund that has the following benefits:

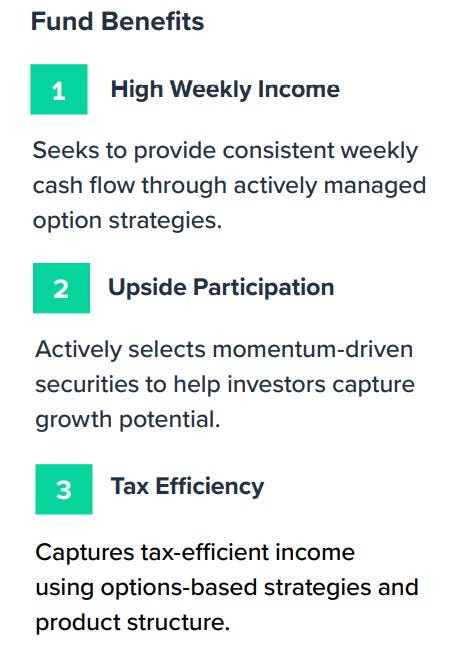

Weekly dividends.

High dividend yield of 37%

Direct exposure to technology stocks

Tax Free Dividends (almost)

Defensive against market declines.

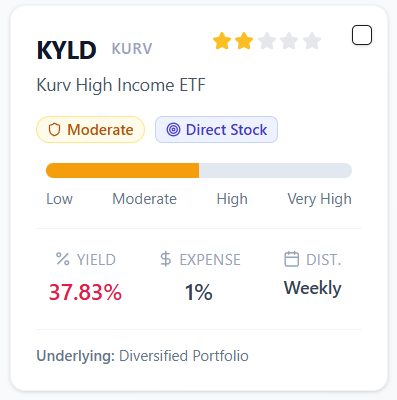

The Kurv High Income ETF KYLD 0.00%↑ is built for this exact purpose. It doesn’t ask you to wait. It is designed to transform volatility into a weekly paycheck, allowing you to live off your assets without having to sell them. The fund is relatively new so I’m willing to bet that most folks have never heard of it.

Our High Yield ETF Database confirms that KYLD currently offers investors a ~37% dividend yield and issues payouts every Friday. However, the fund only earns a 2-star rating and we will cover the risks associated.

$10,000 invested = $3,700 in annual passive income = a $71 dividend every Friday.

$25,000 invested = $9,250 in annual passive income.

$50,000 invested = $18,500 in annual passive income.

$100,000 invested = $37,000 in annual passive income.

The great thing is that this process is scalable. You can start accumulating a high yield fund like this with as little as $1 a day. You can invest at your own pace, it doesn’t matter. The most important thing is to get started and remain consistent.

👉 3 Remining Pre-Launch Discount Spots For Access To The High Yield ETF Database. You also get access to the Yieldly Dashboard.

👉 This database will help you quickly locate the highest quality income funds broken down by rating.

Fund Strategy and Holdings

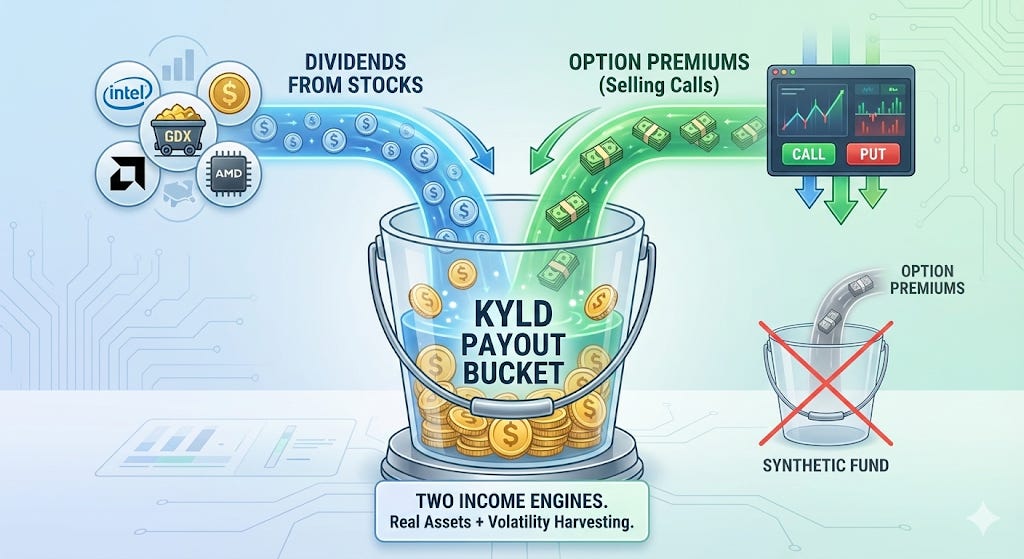

Unlike “synthetic” option funds that only hold cash and derivative contracts, KYLD is backed by real assets. The fund employs a “Covered Call” or “Buy-Write” strategy that offers a two-pronged approach to returns:

Direct Equity Exposure: The fund actually buys and owns the underlying securities. This is critical because it means you aren’t just betting on price movements; you possess ownership in the companies. This allows the fund to collect the actual dividends paid by these companies (like Intel or Gold Miners) in addition to the option premiums.

The “Call Write”: To generate its massive yield, the fund sells (writes) call options against these positions. This “harvests” the volatility of the market, turning price swings into cash premiums that are paid out to you.

Active & Diverse Selection: KYLD doesn’t just buy the S&P 500. It actively selects high-volatility sectors where premiums are richest. As of early 2026, the fund holds a unique mix:

Tech & AI: Direct shares in volatile names like Intel INTC 0.00%↑, Advanced Micro Devices AMD 0.00%↑, and Reddit RDDT 0.00%↑.

Hard Assets: Significant ownership in Mining ETFs like Silver Miners SIL 0.00%↑ and Gold Miners GDX 0.00%↑ to hedge against inflation.

Cash Equivalents: A portion held in T-Bills for stability.

This illustration helps paint the picture on how KYLD generates its income.

Performance Insights: The “All-Weather” Test

Because KYLD owns the actual underlying stock but caps the upside by selling call options, its behavior changes drastically depending on the market cycle. You cannot treat this like a standard index fund; you must understand how it reacts in three distinct environments.

1. Bull Market

In a roaring bull market where stocks rip 20% higher in a month, KYLD will lag. This is the “cost” of the strategy. When the fund sells a call option, it effectively agrees to sell its winners at a specific price. If a holding like AMD explodes upward by 15%, KYLD might only capture 5-8% of that move because they sold the upside potential in exchange for guaranteed cash flow today.

2. The Bear Market (Crash) 📉

In a downturn, KYLD offers a partial buffer, but not total protection. Because the fund owns the actual shares, your portfolio value will drop if the market crashes. However, the massive option premiums act as a shock absorber. If the market drops 10%, the 3% cash premium collected that month helps offset the blow, meaning KYLD might only drop 7%.

The Risk: Equity Exposure. Do not mistake this for a bond fund. It has real equity downside risk and can lose value in a recession.

3. The Sideways Market (The “Chop”) ↔️

This is the “Goldilocks Zone” where KYLD truly shines. In a flat market where traditional stocks do nothing (0% gain), KYLD investors can still generate significant returns. The fund extracts value from “Time Decay”—meaning as long as the market doesn’t crash, you get paid simply for holding the position.

The Advantage: You are converting “waiting time” into “paid time,” generating returns when other investors are stagnant.

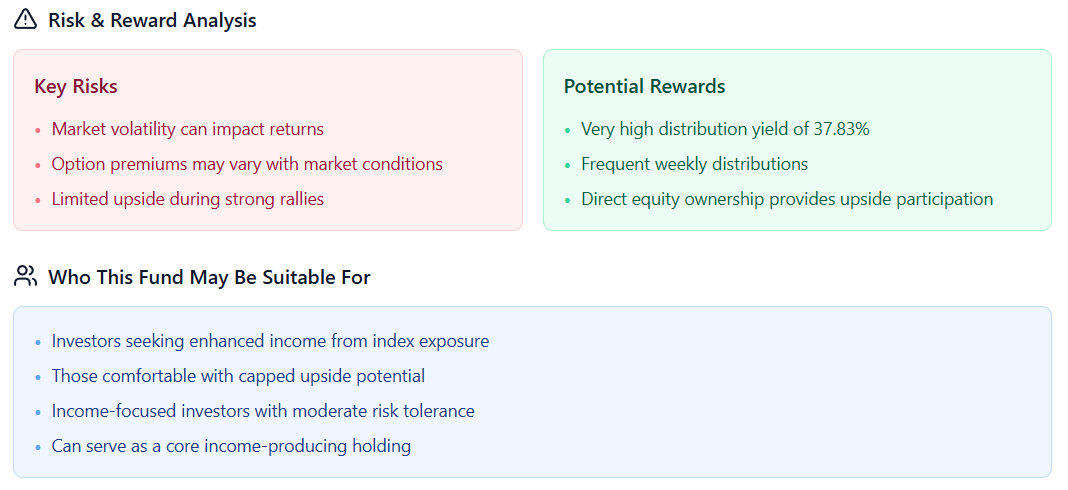

👉 The High Yield ETF Database clearly defines who this sort of fund may be suitable for.

Tax-Free Dividends (Almost)

The most powerful feature of KYLD isn’t just how much it pays, but how it pays it. According to the latest Section 19(a) Notice from January 2026, 99% of the fund’s fiscal year-to-date distributions were classified as “Return of Capital” (ROC). This distinction changes the math entirely for high-income earners.

If you earn dividends from a standard bond fund or REIT, that money is typically taxed as “Ordinary Income.” For high earners, that means losing up to 37% of every payout to the IRS immediately.

Return of Capital is different.

The IRS views ROC not as “new profit,” but as the fund handing you back part of your original investment, whether or not this is actually the case. This means you receive the cash flow today, but you do not report it as taxable income on your return for this year. It is effectively tax-deferred cash flow.

There is no free lunch; there is only deferred lunch. When you receive ROC, you must lower your “Cost Basis” in the stock. For example, if you buy a share for $25 and receive $5 in ROC dividends, your new tax basis becomes $20 per share.

The magic happens when you eventually sell the stock years down the road. Because your basis is lower, you will show a larger capital gain. However, this allows you to effectively convert what would have been “Ordinary Income” (taxed at up to 37%) into “Long Term Capital Gains” (taxed at 15% or 20%). You keep significantly more of your money, and you get to decide when to pay the tax by choosing when to sell.

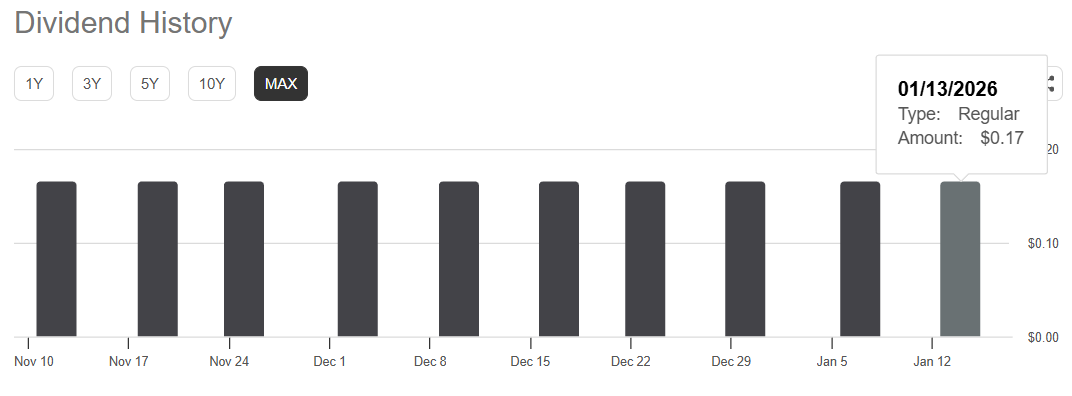

Lastly, KYLD has been able to keep dividends exactly the same since the fund’s launch. Payouts have remained at $0.17 per share.

The Takeaway

KYLD is a specialized "volatility harvester" designed for investors who prioritize immediate cash flow over maximum growth. By employing a covered call strategy on a unique mix of tech stocks and inflation hedges, it generates a massive ~37% annualized yield paid out weekly, making it a powerful engine for flat or choppy markets. While this strategy trades away upside potential during bull runs, its true edge lies in its tax efficiency; with 99% of distributions classified as Return of Capital, it allows high earners to defer taxes on their weekly "paychecks," effectively converting ordinary income into future capital gains.

Did not know about it. Thanks for letting us know.

Amazing! Thank you, Cain!🙌🏼