The Dividend Math That Wall Street Hides

Why compounding dividends create lasting wealth long after stock price growth fades.

Wall Street sells excitement and speculation. It promotes the next hot stock, the next market rally, and the next story that promises to make investors rich overnight. What rarely makes the headlines is the quiet math that has built more lasting wealth than any of those flashy trades: dividends.

Dividends do not get the same attention because they are not dramatic. They appear quietly, a few dollars at a time, without fanfare. Yet behind those steady payments is a compounding engine that most investors never truly see. Reinvested dividends, rising yield on cost, and favorable tax treatment can transform small checks into a stream of income that keeps growing long after the excitement of a stock chart fades.

This is the side of investing that Wall Street rarely highlights. It is not flashy, but it works. And it is the reason dividends remain one of the most reliable paths to financial independence.

The Growth Obsession vs. The Income Reality

Wall Street loves to focus on growth. Analysts issue price targets, investors chase momentum, and financial media highlights companies that could double or triple in value. Growth is exciting. It creates headlines and draws attention. But over the long run, growth alone does not always create lasting wealth.

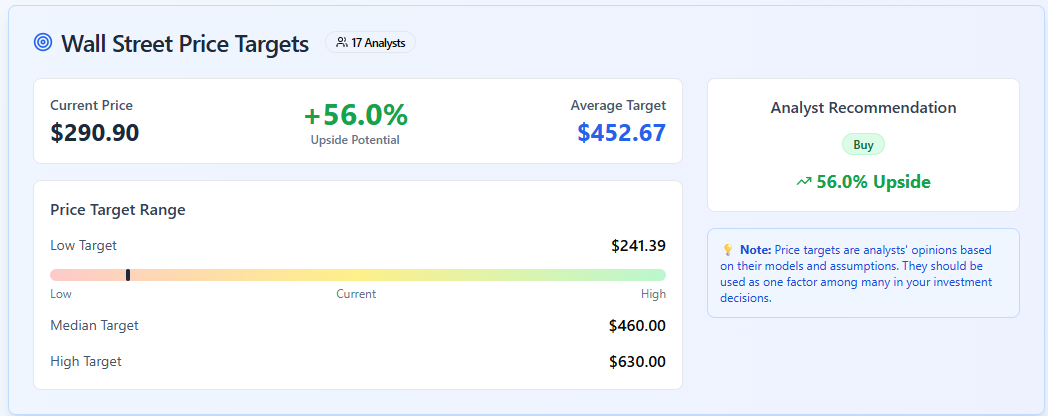

For instance, a quick search of Duolingo DUOL 0.00%↑ on Yieldly, tells us that the stock is extremely undervalued according to Wall Street analysts’ estimates. Yieldly indicates that there is an estimated 56% upside from the current price level. The highest price target indicates that there’s a potential upside of over 100%. This is why I’ve begun accumulating shares on DUOL.

👉 Get a 10% pre-launch discount on the Yieldly dashboard, forever! Offer ends on October 15th. Yieldly is launching on October 30th.

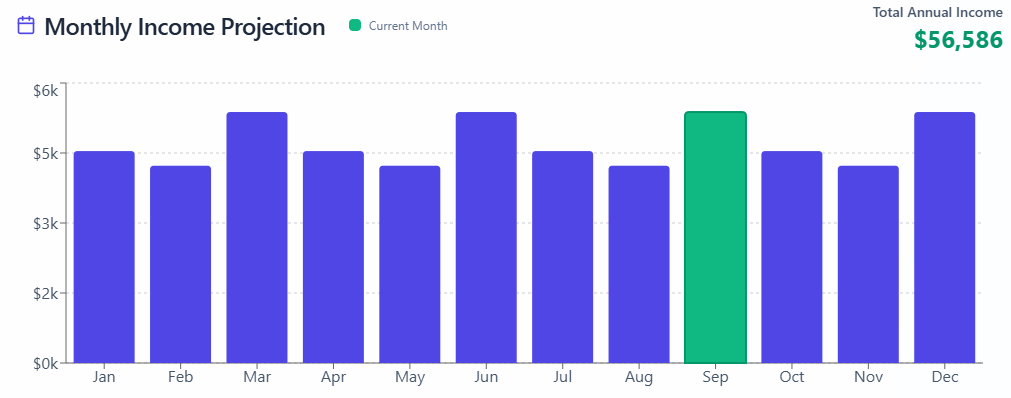

However, focusing on income is different. Dividends may not create the same buzz, but they represent tangible results that cannot be argued with. A stock price can swing wildly from one year to the next, but a dividend payment deposited into your account is real and immediate. Over time, those payments add up in ways that surprise most investors. This is why I take a hybrid approach, as outlined in my latest portfolio update. I now collect an estimated $56.6K in annual dividend income, according to Yieldly.

Consider two paths.

One investor buys a fast-growing stock that doubles in price over ten years.

Another investor buys a slower-growing dividend payer that steadily increases its payout during the same period.

The first investor ends up with a higher account balance, but no income unless they sell shares. The second investor owns a portfolio that now produces a stream of cash flow that can fund expenses, be reinvested, or serve as a safety net.

The difference is subtle in the short term but dramatic over decades. Price growth looks good on paper, but dividend income creates the kind of stability that builds financial independence. By creating a second income stream with dividends, you don’t need to actively sell off your wealth to fund retirement.

Yield on Cost

When you first buy a dividend stock, the yield may look modest, perhaps three or four percent. But as the company raises its payout, your personal yield relative to the price you originally paid rises. A stock that once paid you three percent might be paying ten percent on your original cost a decade later.

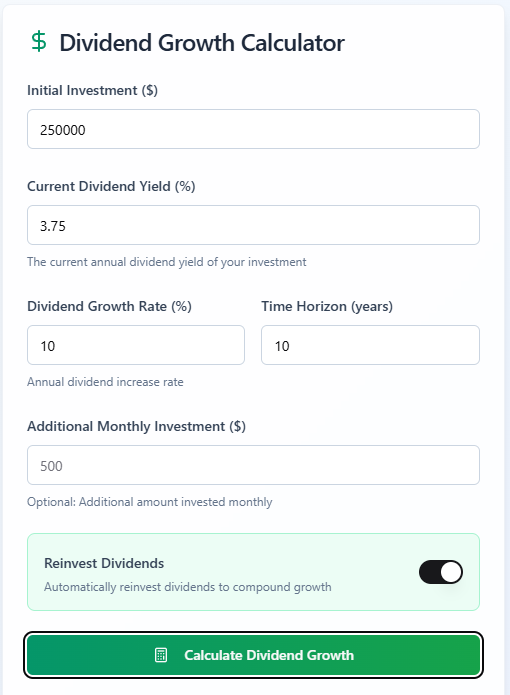

I’ll demonstrate an example with the tools included within the Yieldly Dashboard.

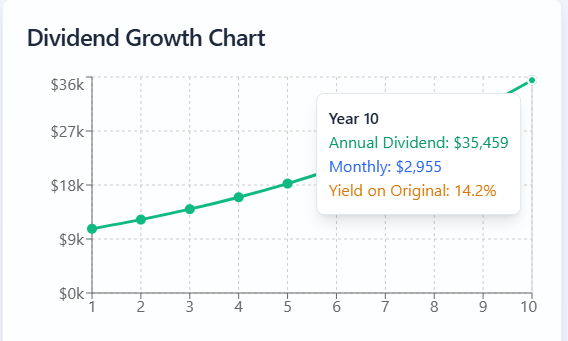

Let’s imagine that an investor is nearing retirement and has $250K in their account. They can allocate this to a dividend ETF like SCHD, which offers a starting dividend yield of 3.75%.

$250K x 3.5% dividend yield = $8,750 per year in dividend income on year 1.

However, SCHD has been able to provide an annual dividend raise of about 10% over the last decade. By simply remaining invested, you would see your dividend income substantially increase over the years if you reinvested your dividends back into SCHD. The result?

In year 10, your annual dividend income would now be over $35K on your original investment, without you adding an extra capital during this time frame. This would be an extra ~$3,000 per month, which is extremely useful for a retiree.

According to Yieldly, you would now have an average yield on cost of 14.1% of your invested capital. Over a ten year span, you would’ve collected over $208K in dividend income, meaning your position size would be nearly double the initially invested amount of $250K.

👉 Get a 10% pre-launch discount on the Yieldly dashboard, forever! Offer ends on October 15th. Yieldly is launching on October 30th.

Tax Treatment

Unlike wages, many dividends are taxed at favorable rates. For some investors, qualified dividends are taxed at zero. For others, the maximum rate is capped at twenty percent. This means more of your income stays in your pocket, further accelerating compounding.

This is the side of dividends that does not appear on a price chart. It is not as exciting as a breakout stock, but the math quietly compounds in ways that surprise even seasoned investors. Here are 3 high-yield funds that pay out tax-efficient dividends.

3 High-Yield Funds That Pay Out Tax-Efficient Dividends

Most people think about investing in terms of returns, meaning what percentage they can earn on their money. But what really matters is what you actually keep after taxes.

I utilize this strategy to collect tax-efficient income within my portfolio. This income has been used for a wide variety of things in my life, including traveling.

Case Study Comparison

To see how the math plays out in practice, consider two investors who each put ten thousand dollars to work.

Investor A: buys a growth stock that doubles in price over ten years. Their account is now worth twenty thousand dollars. On paper, the result looks impressive, but there is no income. The only way to access the gains is to sell shares, which reduces the future growth potential.

Investor B: chooses a dividend stock that starts with a three percent yield and grows its dividend by six percent per year. After ten years, the stock price has appreciated modestly, bringing the account to around fifteen thousand dollars. But here is where the math shifts. The annual dividend income has nearly doubled. Investor B is now earning more than nine hundred dollars per year in cash flow. If those dividends were reinvested along the way, the income stream would be even larger.

The difference between the two paths is subtle at first. Investor A looks wealthier on paper. But Investor B owns an income-producing asset that keeps paying without requiring a sale. Over time, the compounding effect of reinvested dividends and rising payouts allows Investor B’s portfolio to catch up and eventually surpass Investor A’s in real-world utility.

3-Month Access + High-Yield Guide

✅ High-Yield Option ETF Guide + 3 months paid access – Your starting point for building predictable monthly income. 30+ different high-yield funds included.

How to Use This Hidden Math

Start by choosing assets that let compounding do the heavy lifting. Then make reinvestment the default until you reach a cash-flow goal.

Pick the right sources of income

Focus on durable cash generators with a history of paying and raising dividends.

Look for consistent free cash flow, moderate payout ratios, and manageable debt.

Favor businesses or funds that have a clear policy for dividend growth.

Aim for a balanced yield profile

Core growers for reliability and rising payouts over time.

Select high yield positions to accelerate cash flow, sized carefully to manage risk.

Include at least one monthly payer if predictable cash flow matters to you.

Automate the compounding

Turn on dividend reinvestment for your core positions.

Revisit annually to decide whether to keep reinvesting or start taking cash.

Track the metrics that matter

Yield on cost to see personal income growth.

Dividend growth rate to gauge future cash flow.

Payout ratio and coverage to monitor sustainability.

Five year history of payments to avoid serial cutters.

Use a simple cash-flow target

Pick one bill to replace with dividends.

Convert it to an annual target.

Divide by your portfolio’s current yield to estimate needed capital.

Example: a 1,200 dollar annual target at a 4 percent portfolio yield requires about 30,000 dollars allocated.

Rebalance with intention

Trim positions whose dividend growth stalls or whose payout ratio rises too far.

Add to names that keep raising payouts and meet your quality rules.

Keep position sizes within risk limits so one cut does not derail your plan.

Want a more in-depth guide? I put together the Dividend Income Blueprint to give you the ultimately framework to creating a powerful dividend portfolio.

Conclusion

The math behind dividends rarely makes headlines, but it is the quiet force that builds lasting wealth. Growth can make an account statement look impressive, but dividend income turns that paper value into real cash flow. Reinvestment, yield on cost, and favorable tax treatment all work together to compound your results in ways that are easy to overlook but impossible to ignore once they take hold.

This is why dividends matter. They are not just an add-on to growth. They are a system for creating income that builds independence year after year. Wall Street may not highlight it, but you can use it to your advantage starting today.

If you found this helpful and want to see the specific funds and stocks that put this math into practice, consider joining as a paid subscriber. The strategies are simple, but the results can change the way you build wealth.