The One Stock Every Dividend Investor Should Own for the Next Decade

A real example of how adding Mastercard strengthens my equity and lowered my margin burden.

Most people know me for dividend investing. It is the core of almost everything I build. But one thing I do not talk about enough is the role that growth plays in an income focused strategy and how it reduce the burden of margin debt. Growth is not the opposite of dividends.

👉 Growth is the force that strengthens the foundation your dividends sit on.

Mastercard is one of the clearest examples of a stock that does exactly that. It is not the highest yielder in the world, but it compounds wealth at a pace that makes your entire portfolio healthier, more resilient, and easier to manage. Especially if you use margin.

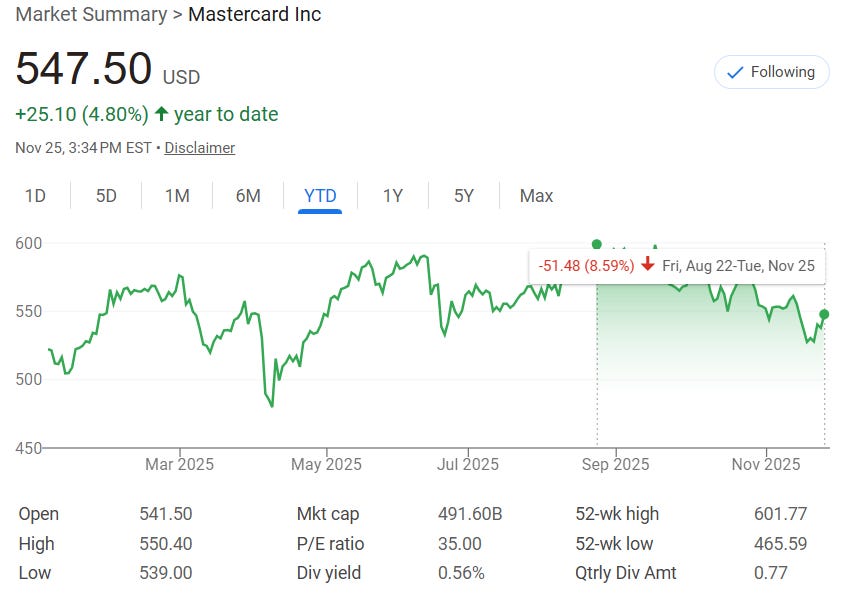

Mastercard MA 0.00%↑ is marginally up 4.8% YTD, but has pulled back roughly 8.6% from its all-time highs. For me, this is a good opportunity to initiate a position.

👉 With the holidays coming up, consider gifting a subscription!

Growth Is Happening At A Pace Most Companies Dream Of

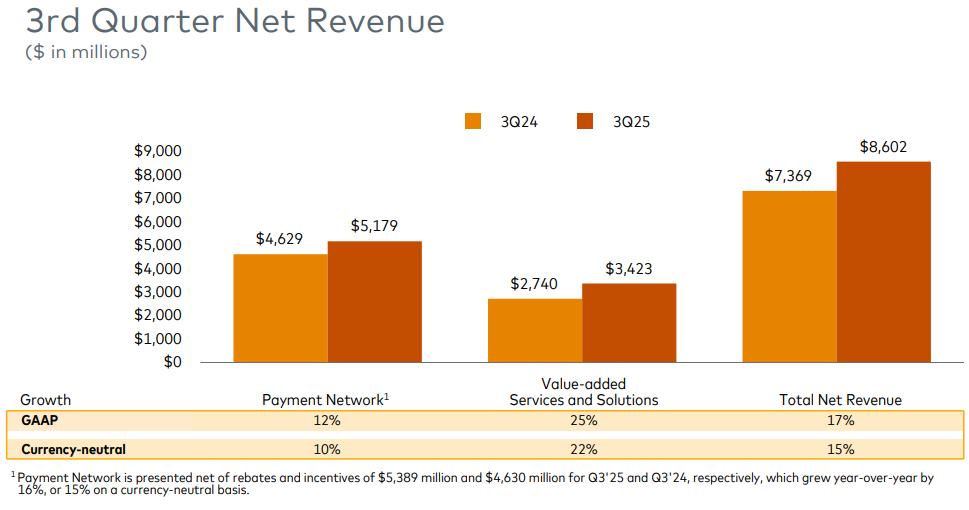

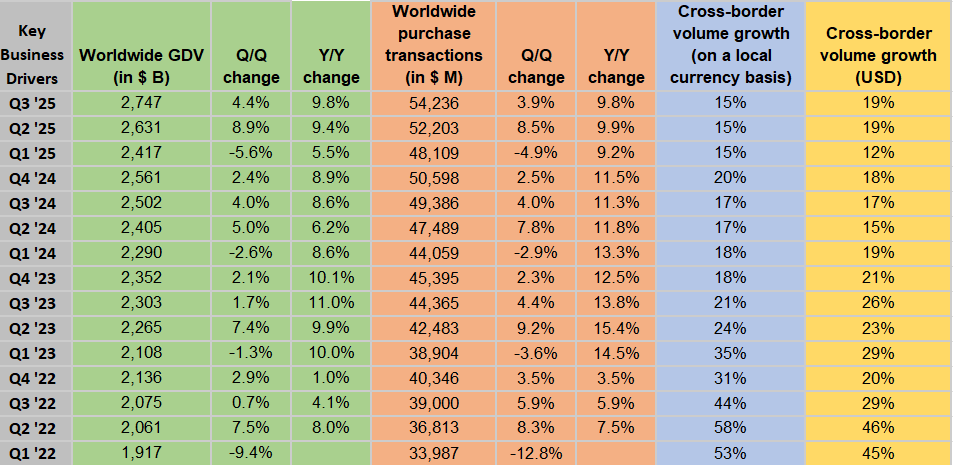

Mastercard’s most recent quarter looked like a company that hasn’t lost a step. Revenue grew almost 17% and EPS came in ahead of expectations. When you look under the surface, the strength becomes even clearer. Gross dollar volume increased, purchase transactions climbed, and cross border activity continued its powerful recovery. Cross border spending has always been one of Mastercard’s highest margin categories, so that strength matters.

This tells me something simple. Consumers are spending. Travel is healthy. Digital payments continue to expand. Mastercard is doing more than just participating in these trends; It is one of the companies shaping them.

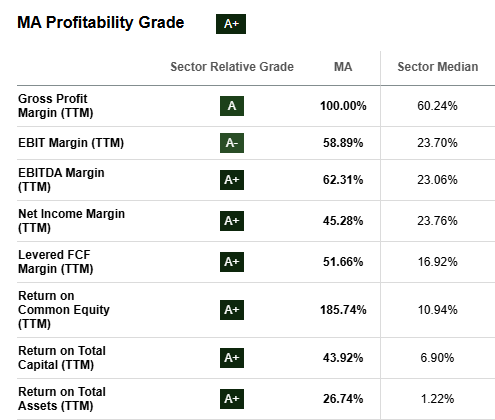

Mastercard’s profitability metrics are crushing the rest of the financial sector. As we can see below, MA is simply earning cash hand over fist.

Revenues and Gross Profit has steadily increased year over year, for the last decade. All in all, I anticipate Mastercard to deliver an annual growth between 12% - 15% over the next five years.

The Dividend Story Is Strong

While I was able to juice my dividend income up to $50,806 annually using high risk income funds, the foundation of my portfolio was built on companies like Mastercard. So while the starting dividend yield is very low at 0.5%, there is virtually no risk to the dividend being cut.

Here are the simple facts about Mastercard’s current dividend strength:

The dividend payout ratio is EXTREMELY low at 18.9%.

Cash generation is strong.

Dividend growth has been consistent for well over a decade.

Profitability is so high that the company can continue raising the payout for many years without stress.

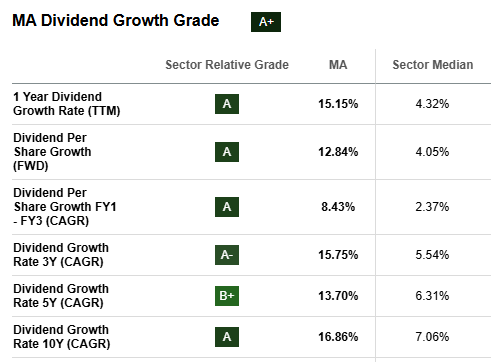

Looking at the screenshot below, we can see that Mastercard has averaged an annual dividend raise of 16.86% over the last DECADE. Can you imagine receiving such a large double-digit raise from your job every year for a decade straight?

A lot of people overlook companies like Mastercard because the yield is tiny. What they forget is that dividend income grows faster when the underlying equity grows faster. You are not buying a stream of income. You are buying a machine that becomes more valuable every year and gives you a little more income each time it does.

However, I clearly want to state that I am holding Mastercard for its growth potential.

Growth reduces margin pressure and stabilizes your income engine

This is something I want more dividend investors to understand. Growth stocks are not just nice to have. They directly reduce the burden of margin.

Here is why.

As a growth name like Mastercard appreciates, your account equity rises. When your equity rises, your loan to value improves. When your loan to value improves, your margin interest becomes less heavy on your portfolio and your risk declines. All of this happens naturally in the background.

A stable compounder like Mastercard makes your whole income system safer and more flexible. Your yield stocks provide cash flow. Your growth stocks provide strength and stability. When the two work together, you get the best of both worlds.

Here’s a very simply breakdown using my own numbers as an example:

👉 I currently have ~$48,000 in margin debt and across all my accounts I have a blended equity of 84% in my portfolio.

Let’s just say that I hold Mastercard and the position appreciates over time.

Example:

84% equity in my portfolio

Imagine a scenario where my Mastercard position increases by $10K in unrealized gains.

Based on my portfolio size, that unrealized gains will increase my equity

In return, this reduces the overall burden that my margin has.

So even though Mastercard isn’t directly paying down my margin, the growth reduces the overall weight of my margin usage since the value of my portfolio is rising.

For now, I’ve initiated a starting position and plan to grow this over the next several months. I have a 12-month price target of $585.

Visa V 0.00%↑ Comparison

Visa and Mastercard are almost identical businesses, so investors often try to compare them as if one must clearly outperform the other. The truth is more balanced.

Visa grew United States payment volume slightly faster this quarter, but Mastercard continued to lead in value added services. Visa is closing some of the gap. Mastercard is expanding in other areas. On the whole, both companies remain exceptionally strong.

What matters most is that Mastercard’s long term growth drivers have not changed. The shift away from cash continues. International travel keeps growing. Digital wallets and e commerce expand every year. And Mastercard is positioned to benefit from all of it.

This quarter was not a sign of decline. It was a reminder that both networks remain incredibly dominant.

Stablecoins Are Not An Immediate Threat

Stablecoins are digital tokens that are designed to hold a steady value, usually by being backed one to one by real world assets like US dollars or short term treasury bills. They allow people to move money quickly on blockchain networks without the price volatility of traditional cryptocurrencies.

Stablecoins attract headlines, but what matters is adoption. Right now, adoption is tiny compared to the global payments market. Most stablecoin activity happens within the crypto ecosystem rather than in the commercial world where Mastercard operates every day.

Even if stablecoins grow, merchants will still need fraud prevention, cybersecurity, tokenization, data analytics, and dispute resolution. These are all services that Mastercard already excels at and continues to invest in. Unless merchants suddenly do not care about security or compliance, Mastercard will remain a central player in global payments.

This transition will take many years. Mastercard has time. And it is already building products that sit on top of new payment technologies rather than getting pushed aside by them.

The long term picture remains incredibly strong

When I step back and look at Mastercard as a whole, the story becomes simple.

This is a business that grows consistently in the mid teens. It is one of the most profitable companies in the world. It produces an enormous amount of free cash flow. It raises its dividend year after year. And it benefits from global shifts that will continue for decades.

It also happens to be a perfect companion to your income generating positions because it strengthens your margin profile and increases your account equity consistently. I remain long Mastercard. I plan to stay long. And I think the next decade is still full of growth for the company and for anyone who owns it.

Ok I just did the math with this with 10k

invested for this vs S&P. Over the last 20 years. I can’t believe how much of a huge difference it was and better to own MA with a small amount contributed. 1k a year after the fact and you are over 1M+ with a small amount invested

What about the new deal that MC and V made with their retailers? Vendors can refuse to accept high rewards cards.