The Yield Trap: Why I Sold Two High-Yield Option ETFs

Is Your 50% Yield Losing You Money? Here is Why I Traded "Fake Yield" for Real Growth.

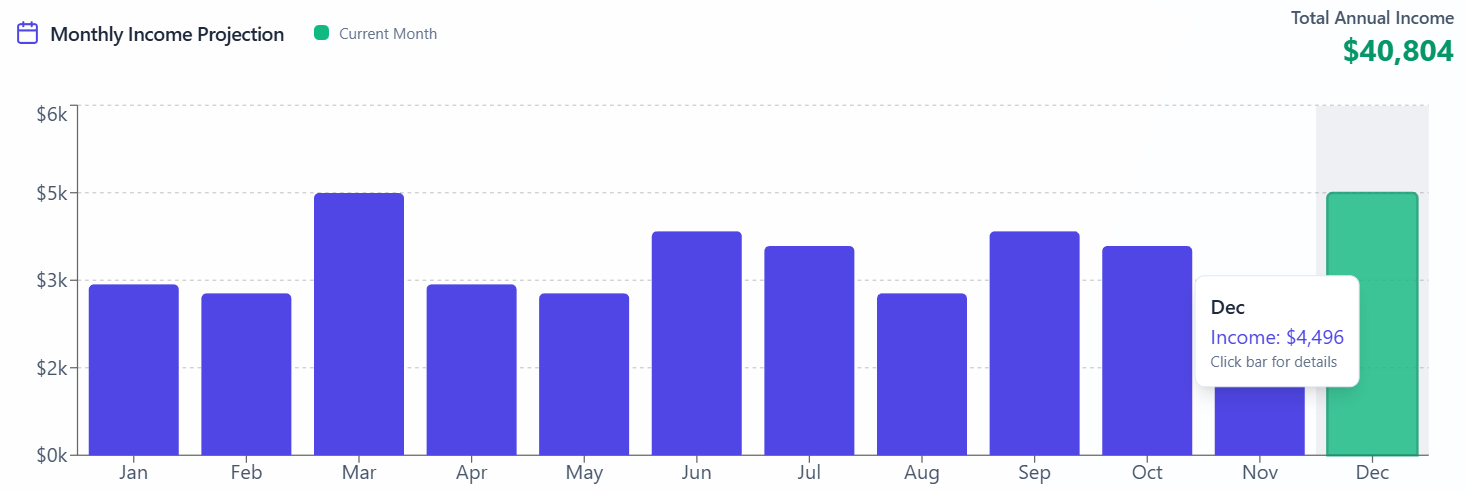

November Dividend Income Report: $3,142 Collected

November was a pivotal month for the portfolio. While the income remains strong at $3,142, the strategy has fundamentally shifted. I’ve now collected approximately $40K in dividends YTD. I anticipate that I will end 2025 with about $44,000 in total dividends collected.

For months, I have tracked the performance of various high-yield “Option ETFs.” These funds promise massive annual yields, sometimes exceeding 50% or even 100%. However, after analyzing the total return (Price Appreciation + Dividends), I realized that many of these positions were eroding capital faster than they were paying it back.

So to avoid you readers from seeing your capital erode, I wanted to share the exact details of how we can refine this system. Just to be clear, I STILL love dividends. I just want to shift to a more sustainable approach for all of us.

In this report, I am breaking down exactly why I sold popular funds like:

YieldMax Ultra Option ETF - ULTY 0.00%↑

YieldMax TSLA Option Income ETF - TSLY 0.00%↑

And why I started reallocating that capital into “boring” growth compounders like:

Amazon AMZN 0.00%↑

Mastercard MA 0.00%↑

Meta Platforms META 0.00%↑.

Total Income Breakdown

First, let’s look at the income. Despite the rotation out of these assets, the cash flow generated within my portfolio remains substantial.

However, a high payout is meaningless if your principal investment is shrinking every month. This is where a tool like Yieldly becomes invaluable, allowing you to track not just your income, but your portfolio’s overall health and projected growth.

👉 Want to track your portfolio’s true performance? Upgrade to Yieldly with a post-launch 5% discount.

The Problem: NAV Erosion

One of the most common questions I get is: “Why sell a fund that is paying you 50% yield?”

The answer is NAV (Net Asset Value) Erosion.

Many covered call ETFs cap their upside. When the underlying stock (like Tesla or Coinbase) rips higher, the ETF is capped. When the stock crashes, the ETF drops 1:1. In plain English, the upside movement of these YieldMax funds are capped, but the downside risk is not.

Over time, this creates a downward spiral in the share price. If a fund pays you $1.00 in dividends but the share price drops by $1.50, you have lost money.

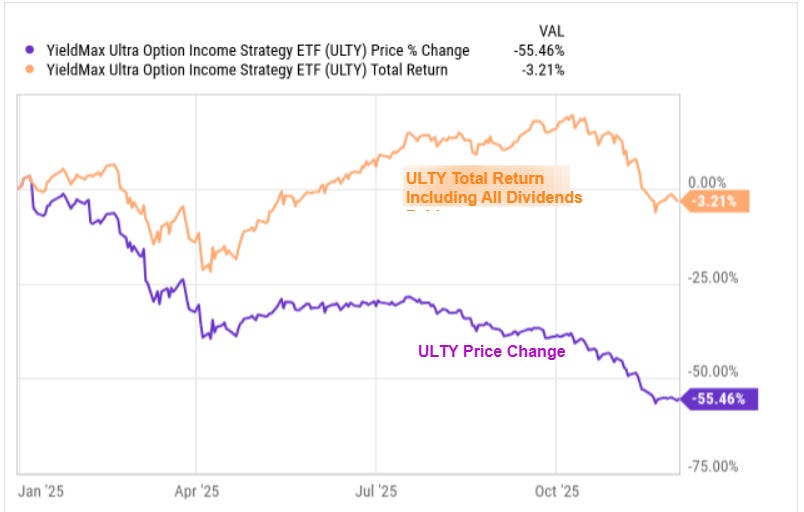

Therefore, funds like ULTY no longer make sense despite its high dividend yield of 77% and weekly payouts,

An important lesson is that a high dividend yield doesn’t automatically result in a high total return. So even if ULTY offers a dividend yield of 77%, you should not expect to actually collect 77% a year. We can refer to ULTY’s performance on a YTD basis below. The fund has seen its share price decline by a massive 55.46%. When including all dividends paid, the total return is still a loss of 3.21%. This concept is what is referred to as NAV erosion. ULTY has ultimately paid out more than it actually generates in income, leading to these large losses.

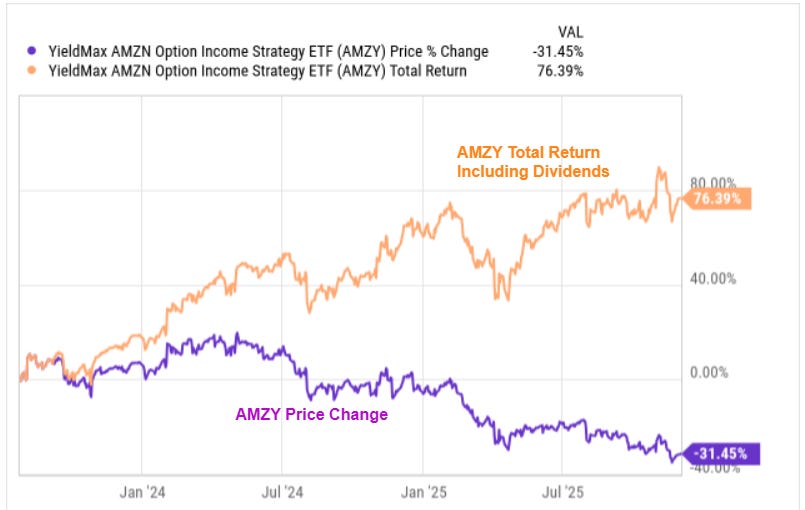

Ideally, we want the total return including dividends to outpace the share price decline. A successful example can be seen when looking at the performance of the YieldMax AMZN Option Income ETF AMZY 0.00%↑. AMZY offers a dividend yield that typically falls around 50%. We can see that AMZY’s share price has declined, but the total return including all dividends paid has outpaced. This means that AMZY has proven to be a successful addition within my portfolio.

The Shift: Selling Yield Traps, Buying Moats

I executed a major rotation this month. I sold out of the positions that were showing consistent principal decay and moved that capital into companies with wide competitive moats and actual earnings growth. Using the example above, AMZY has proven to be a success income position. However, the share price has still ultimately declined over time. So how do we offset this?

With growth.

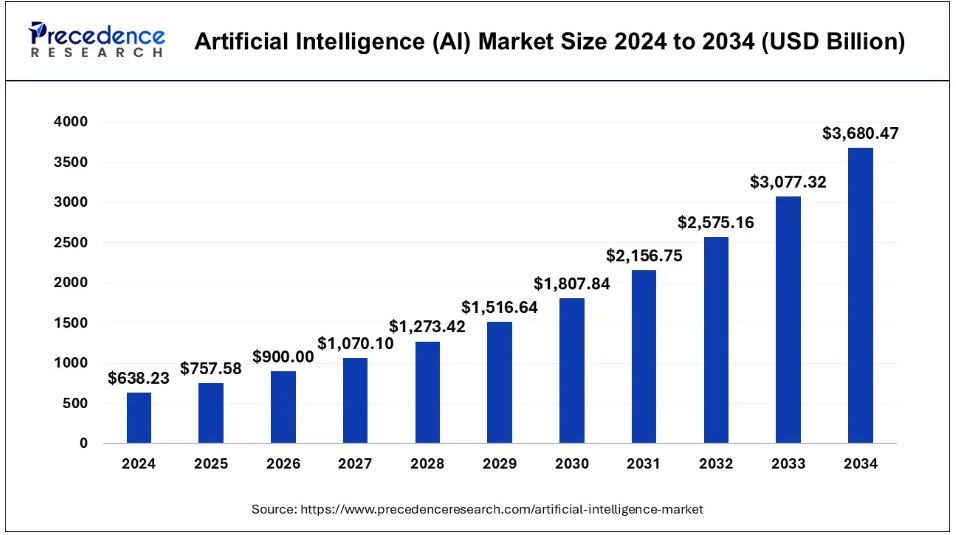

This is why growth is still an essential part of the strategy. I’ve chosen to capture growth through different technology holdings. The size of the AI sector is estimated to increase at a CAGR (compound annual growth rate) of 19.20% through 2034.

So how do we invest in the growth of AI?

By investing into high quality companies that will expand earnings over the next decade.

I choose to do so with opportunities that provide the most risk-adjusted return. These are the large-cap corporations that have the means to invest in the expansion of AI and they present the lowest risk:

Meta Platforms META 0.00%↑

Alphabet GOOG 0.00%↑

Microsoft MSFT 0.00%↑

Amazon AMZN 0.00%↑

ASML Holdings ASML 0.00%↑

While this is my chosen path, you may want to capture growth through different channels like Financials, Consumer Staples, or Real Estate. There is no ‘correct’ choice. The important thing is that we counteract these income positions with more traditional holdings.

Forward Outlook

Does this mean I am done with income investing? Absolutely not.

I still hold positions like QDTY 0.00%↑, YMAX 0.00%↑, and ARCC 0.00%↑, which have performed reasonably well. However, the “speculative” portion of my portfolio is shrinking. I am building a foundation that doesn’t just pay me today, but also grows for tomorrow.

The goal remains $100,000 in annual passive income. But I want that $100,000 to come from a portfolio that is worth more in 10 years, not less. Yieldly’s projection tools are crucial for visualizing this long-term growth and ensuring I’m on track.

My Next Moves:

Accumulate more META 0.00%↑ shares on any weakness.

Reinvest dividends from the remaining high-yielders into QQQM 0.00%↑ to capture the growth of the Nasdaq-100.

Search for more high quality income positions. I will add to QDTY 0.00%↑ on pullbacks.

The only Yield Max fund I currently own is CHPY. The rest of my funds are from Rex Shares, Kurv, and Roundhill. I did very well last year and am so far on track to beat the market again this year (we will see if I do it again). I think that the structure of the single stock YM funds are somewhat problematic. Less consequential in a Roth IRA, but quite devastating in a taxable account if things go bad. The risk-return proposition on the single stock ETFs are not favorable. I will say, however, that their target products are interesting.

Great article! How do you see the comparison on seeking alpha for change in price and total return?