Top 10 Stock Picks for 2026: The Ultimate Growth & Income Watchlist

The exact growth stocks I’m buying to multiply wealth, and the income funds I’m using to pay the bills.

Most investors are forced to choose a side. You are either a “Growth Investor” chasing the next AI rocket, or a Dividend Investor settling for slow, steady 4% yields.

I believe that is a false choice.

In 2025 I deployed a hybrid strategy by aggressively buying high-conviction infrastructure plays while simultaneously harvesting volatility for weekly cash flow. The result?

I generated $43,000 in annual passive income and outperformed the broader market while doing it.

This article is my playbook for 2026.

I have selected 10 high-conviction tickers that represent the perfect marriage of capital appreciation and cash flow velocity. The first five are the “Growth Engines” designed to multiply your net worth. The second five are the “Income Generators” designed to pay your bills while you wait. When you combine them, you create a flywheel effect: using your growth profits to buy more income, and using your income to buy more growth.

👉 For Paid Subscribers: You are getting the tools to track it.

The Yieldly Dashboard: My personal tool for tracking dividend velocity and projected income.

The High Yield Database: Instant access to the highest-rated income funds, filtered by risk and tax efficiency.

Custom Video Summaries of all articles going forward.

Buy alerts when I add shares to these companies.

👉 Consider upgrading to get instant access to these investment tools, as well as all products and dashboards released in the future. 2 more pre-launch discount spots available.

Let’s look at the portfolio.

Part 1: The Growth Engine

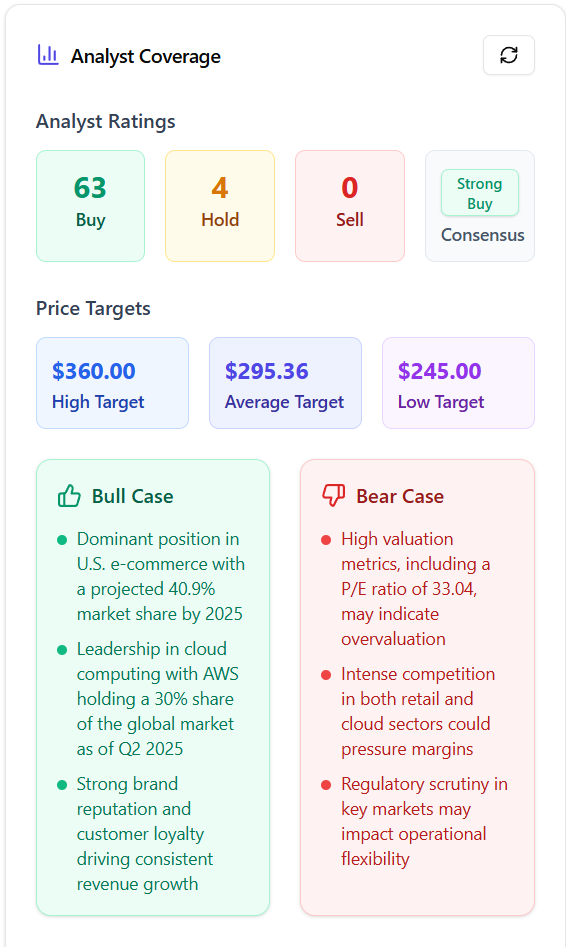

1. Amazon AMZN 0.00%↑

I believe that Amazon will eventually be worth $10 Trillion in our lifetime.

Amazon remains the undisputed backbone of the modern internet. As we move deeper into 2026, the “Cloud 2.0” thesis is fully materializing. Corporations are shifting from testing AI models to deploying them at enterprise scale, which directly benefits AWS (Amazon Web Services). Unlike its retail business, which operates on thin margins, AWS is a high-margin profit engine that is expected to drive the bulk of the company’s earnings growth over the next 12 months.

2026 EPS Projection: Estimates hover around $7.21 - $7.87, driven by efficiency gains in logistics and cloud acceleration.

Projected Growth: Earnings are forecast to grow by roughly 15-16% annually.

The Yieldly Dashboard estimates there to be a ~50% upside from the current price level. Amazon has become one of my largest positions and I plan to continue accumulating as long as the price remains below $240 per share.

2. AST SpaceMobile ASTS 0.00%↑

This is the “high-risk, high-reward” play of the portfolio. AST SpaceMobile is successfully transitioning from a concept to a commercial utility provider. With its BlueBird satellites now operational, 2026 is the pivotal year for revenue ramp-up. The company is uniquely positioned to partner with major telecoms (like AT&T and Verizon) to eliminate dead zones, effectively turning every smartphone on earth into a potential customer without requiring new hardware.

Revenue Outlook: Analysts project massive top-line expansion, with estimates of 45%+ annual revenue growth as commercial service goes live.

The Risk/Reward: While EPS may remain negative during this scaling phase (est. -$0.66), the catalyst is the flipping of the switch on commercial revenue.

ASTS is now up more than 60 % since I issued a buy alert about a month ago.

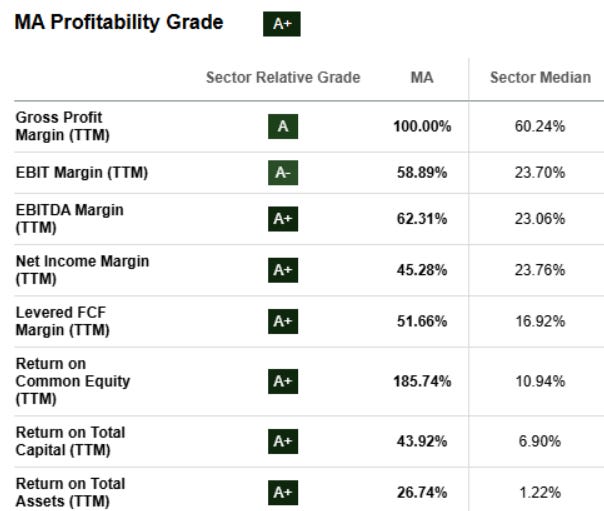

3. Mastercard MA 0.00%↑

Mastercard is the “steady hand” that balances the volatility of tech stocks. The company continues to benefit from the secular war on cash and the expansion of high-margin services like cybersecurity and data analytics. Even in a fluctuating economy, global transaction volumes are resilient. Mastercard effectively operates as a royalty on global GDP, making it one of the safest compounders to hold for the long term.

2026 EPS Projection: Consensus estimates sit at approximately $15.67, reflecting its dominant market position.

Growth Rate: The company has maintained a reliable EPS CAGR of ~16% over the last three years.

Mastercard continues to demonstrate excellent earnings growth, free cash flow growth, and profitability metrics.

4. Bloom Energy ($BE)

I issued a buy alert on this one and it’s not up more than 54% since then. However, I believe that Bloom energy can be a multi-bagger. We’re looking at a company with the potential to 5x over the next few years.

Data centers are the new oil fields, and they are running out of power. Bloom Energy is the “pick and shovel” play for the AI energy crisis. As utility grids struggle to keep up with the gigawatt-demand of AI server farms, Bloom’s solid-oxide fuel cells offer a plug-and-play solution for on-site power generation. The backlog for these systems is growing rapidly as tech giants seek energy independence from fragile public grids.

Growth Catalyst: 2026 EPS is projected to jump by nearly 78% YoY, significantly outpacing industrial peers.

Profitability: The company is moving from growth-at-all-costs to profitability, with margins expanding as manufacturing scales.

As demand for AI data centers grow, Bloom is directly positioned to capitalize on this.

👉 Consider upgrading to see the full list!

Not ready to upgrade? That’s fine. New free subscribers will still unlock access to the following perks:

✅ ETF For Beginners Dashboard

✅ A List Of Dividend Growth Legends

✅ 50+ Monthly Paying Dividend Stocks

Okay let’s move on…

Keep reading with a 7-day free trial

Subscribe to Dividendomics to keep reading this post and get 7 days of free access to the full post archives.