Turn $100K Into $3,000 A Month In Dividends

A step-by-step blueprint to transform six figures into a full-time dividend income stream.

Most people assume you need millions to live off dividends. After all, if you’re only getting a 3% yield from blue chip stocks, $100K won’t even buy you $3,000 a year. That’s not enough to cover groceries, let alone rent or a mortgage.

But dividend investing isn’t limited to 3% yields. In fact, there are corners of the market where double digit payouts are the norm. The catch? You have to understand how they work and the risks involved.

If I had $100K to work with today, here’s how I’d structure it to potentially generate $3,000 a month, or $36,000 a year, in dividends.

The Reality Check

Let’s start with the math.

$3,000 per month equals $36,000 per year.

On a $100,000 portfolio, that’s about a 36% yield.

Now, I’ll be upfront: you’re not going to get there buying Apple, Microsoft, or Johnson & Johnson. Even so-called high yield dividend aristocrats top out around 4 to 5 percent. You will be taking on an elevated level of risk.

To hit 20 percent or higher yields, you need to look at income-focused vehicles such as covered call ETFs.

These aren’t the same as buying Procter & Gamble and forgetting about it. They trade growth potential for higher immediate cash flow. That’s the trade off, and it’s one you have to be comfortable with if you’re chasing this level of income.

The Core Strategy

If I wanted to take $100K and turn it into $3,000 a month in dividends, I’d focus on one of the few corners of the market that makes that possible: covered call ETFs.

Synthetic option ETFs take the traditional covered call concept and push it further. Instead of holding a basket of stocks and then selling call options against those positions, these funds use derivative contracts exclusively. In other words, they don’t actually own the underlying equities.

Here’s what happens: the ETF enters into swap or derivative agreements that mimic the performance of an index, such as the Nasdaq 100 or the S&P 500. At the same time, it systematically sells call options on that index to harvest premium income. Because the strategy doesn’t require holding the actual stocks, the fund can concentrate purely on generating cash flow from options.

The result is extraordinary yield potential. While a traditional covered call ETF might pay 12 to 20 percent annually, synthetic structures can often distribute 40 percent or more.

These are the sort of funds that helped propel my dividend income average up to $3,500 a month.

Over the next twelve months, I am expected to collect over $56,000 in dividends. This is a full time income and I am aiming to grow this above $100,000 eventually.

For reference, I post dividend reports at the end of every month!

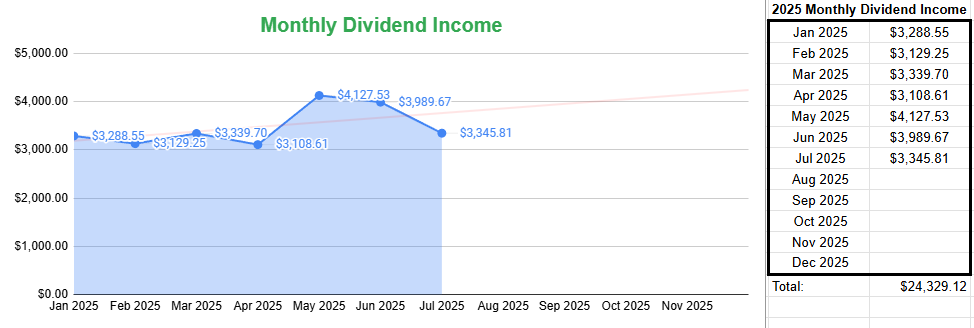

July 2025 Dividend Report

For the month of July, I’ve been able to collect $3,345 in dividend income. This was an increase of 7.6% from the prior quarter’s amount (April). I was able to passively increase my dividend income by reinvesting portions of the dividends received, back into different high-yield funds. This growth could have been more aggressive if I chose to roll dividends back into income positions, rather than growth.

This strategy comes with a major trade-off however. Since they don’t own equities, these funds don’t collect dividends from the underlying companies, nor do they benefit from capital appreciation if the market rallies. They are designed for one thing only: turning volatility into income.

Think of it like running a rental property business where you don’t own the houses, you just control the cash flow contracts. It’s leaner, riskier, and far more focused on extracting income than building long-term value.

The Math

Let’s put that in context.

$100,000 in the S&P 500 (SPY) at a 1.4% yield = about $1,400 per year in dividends.

$100,000 in a dividend ETF like SCHD at a 3.5% yield = about $3,500 per year in dividends.

$100,000 in a high-yield covered call ETF at 18% yield = about $18,000 per year, or $1,500 per month.

And in some cases, these funds pay closer to 20–24% yields, which would hit the target of $3,000 per month, or $36,000 per year.

That’s the difference between collecting a small supplement and actually covering a mortgage payment with dividends alone.

Covered Call ETFs vs. Rental Properties

In many ways, covered call ETFs function like rental properties but without tenants or toilets.

With real estate, you put up capital (a down payment), then collect recurring monthly rent. But that rental income comes with headaches: repairs, vacancies, property taxes, and leverage risk.

With covered call ETFs, you also put up capital, and instead of rent, you collect recurring option premiums that get paid out monthly. The “maintenance” is just the fluctuation of distributions, which rise and fall depending on market volatility.

Both approaches sacrifice something. With real estate, your property value might not always climb as fast as you’d like. With covered call ETFs, your stock portfolio won’t capture as much upside because you’ve sold that away in return for income.

But for someone who values cash flow now, covered call ETFs can play the same role as a rental property by turning capital into reliable monthly income.

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

The $100K Covered Call ETF Portfolio

Now let’s get into the specifics. If I had $100K and wanted to target $3,000 per month in dividends, here’s exactly how I’d allocate it across high-yield covered call ETFs.

Keep reading with a 7-day free trial

Subscribe to Dividendomics to keep reading this post and get 7 days of free access to the full post archives.