UnitedHealth Group Is Undervalued: A Blue-Chip Bargain In Plain Sight

UnitedHealth Is Under Pressure But That’s Exactly Why It’s a Buy

UnitedHealth Group UNH 0.00%↑ has entered one of the most attractive valuation ranges in over a decade. After a multi-week selloff driven by headline risk, leadership changes, and earnings uncertainty, the stock is now trading at a price that long-term investors should not ignore.

Despite recent turmoil, the company remains one of the most essential businesses in the American economy. It has strong cash flow, a wide economic moat, consistent dividend growth, and exposure to nearly every corner of the healthcare system.

Investors willing to look past short-term fear may be rewarded with long-term value.

A Massive Healthcare Machine with Two Engines

UnitedHealth operates through two primary business lines:

UnitedHealthcare provides insurance coverage to more than 51 million members across individuals, employers, and government programs such as Medicare and Medicaid.

Optum delivers healthcare services directly, including pharmacy benefit management, patient care, data analytics, and health tech infrastructure.

In the first quarter of 2025 alone, UnitedHealthcare generated over 84 billion dollars in revenue with more than 5 billion in earnings. Optum brought in over 63 billion dollars in revenue and 3.9 billion in earnings.

Together, these units generated over 148 billion dollars in a single quarter. The margins were slightly compressed due to a spike in medical care usage among older Americans, but profitability remains high.

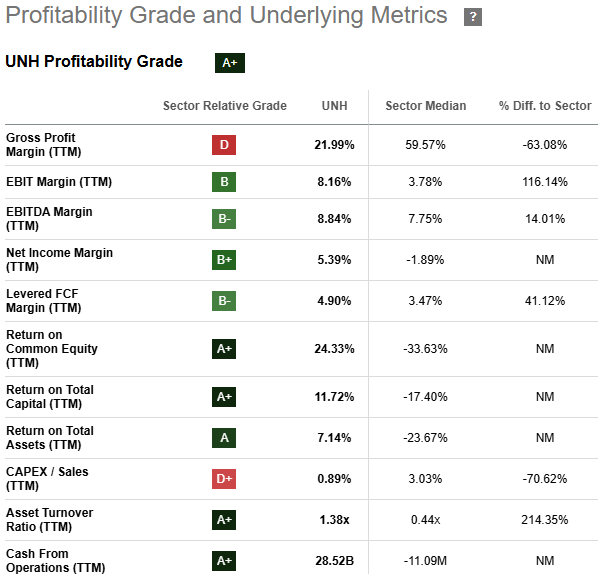

Key Profitability Metrics

EBIT Margin:

UNH delivers an EBIT margin of 8.16%, more than double the sector median of 3.78%. This indicates strong operational control in a heavily regulated industry.EBITDA Margin:

At 8.84%, UNH outperforms the sector’s 7.75%average, showing healthy core profitability before non-cash expenses and taxes.Net Income Margin:

With a 5.39%net income margin versus a sector median of negative 1.89%, UNH stands out in turning revenue into real earnings.Free Cash Flow (FCF) Margin:

The company’s levered FCF margin of 4.90% is 41% higher than the sector median, which underscores its ability to turn profits into usable cash.Return on Common Equity:

UNH posts a 24.33% ROE, far above peers, earning it an A plus grade. This level of capital efficiency speaks volumes about management’s skill.Return on Total Capital:

UNH’s 11.72% return on capital reflects strong reinvestment dynamics and disciplined asset use.Return on Total Assets:

At 7.14%, UNH again beats the sector by a wide margin, confirming its ability to extract value from its asset base.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

Short-Term Trouble Sparked a Massive Pullback

The headlines have not been kind. The Department of Justice is investigating Medicare claims. Bill Ackman accused the company of aggressive earnings practices. The CEO resigned. Analysts slashed near-term earnings forecasts. And share prices plunged by more than 50% over five weeks.

But not everything is negative.

Stephen Hemsley, the former CEO, stepped back in and purchased 25 million dollars worth of stock. That insider move triggered a short-term rally and helped stabilize investor sentiment.

While the outcome of the DOJ probe remains uncertain, the market has already priced in a heavy dose of pessimism. This may be a case where fear is overstated and opportunity is being overlooked.

Valuation Has Reached Extreme Lows

By most metrics, UnitedHealth is now a bargain.

Current forward price-to-earnings ratio is around 13

Ten-year average price-to-earnings is closer to 23

Intrinsic value estimates range between 450 and 470 dollars per share

The stock recently traded between $302 and $316 per share.

Even under a more bearish forecast where earnings fall to 17 dollars per share, the stock would still be trading around 17 times earnings, which is far from distressed.

The market appears to have overcorrected.

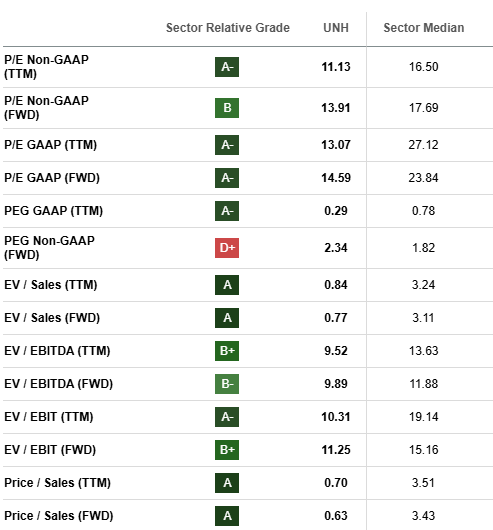

Looking at UnitedHealth Group’s valuation against the broader healthcare sector, it is clear the stock is trading at compelling levels on nearly every major metric.

Price-to-Earnings (P/E):

UNH trades at a trailing twelve-month P/E of 11.13 and a forward P/E of 13.91, compared to sector medians of 16.5 and 17.69 respectively. On a GAAP basis, the forward P/E is just 14.59, well below the sector median of 23.84. These figures suggest the market is pricing in more risk than long-term fundamentals justify.

PEG Ratio:

While the trailing PEG ratio is very favorable at just 0.29, the forward PEG of 2.34 is slightly above the sector median of 1.82, reflecting tempered growth expectations amid regulatory uncertainty. This metric may normalize once investor confidence returns and the earnings outlook stabilizes.

Enterprise Value Metrics:

UNH’s enterprise value relative to sales and EBITDA are both extremely attractive. EV to Sales is 0.84 versus a sector median of 3.24. Forward EV to Sales drops further to 0.77. These deep-value readings highlight how undervalued the business is based on its revenue base. EV to EBITDA sits at 9.89, which is well below the sector average of 11.88.

Earnings and Sales Multiples:

On an EBIT and EBIT forward basis, UNH trades at 10.31 and 11.25 times earnings, respectively, compared to sector medians of 19.14 and 15.16. Price to sales metrics tell the same story — UNH trades at just 0.70 times trailing sales and 0.63 times forward sales, compared to a sector median of 3.43.

Overall, UNH is priced significantly lower than the sector across nearly every meaningful valuation metric. While some of this may reflect temporary uncertainty, the depth of the discount provides a strong margin of safety for long-term investors.

Fundamentals Are Still Rock Solid

Despite recent weakness, UnitedHealth's fundamentals are strong:

Ten-year compound annual EPS growth rate is 12.9%

Dividend growth has averaged 15% per year

Five-year average return on equity is nearly 24%

Return on invested capital is just under 16%

Debt-to-equity ratio remains well below 1

Gross margins are declining slightly but remain stable

The current ratio is below 1, indicating short-term obligations need monitoring but not alarm

This is a company that continues to produce strong earnings, return capital to shareholders, and maintain one of the strongest brands in the healthcare sector.

While UnitedHealth Group faces short term pressure from regulatory scrutiny and higher medical claims, the broader macro backdrop may ultimately work in its favor. According to research by PwC, commercial healthcare spending is expected to reach its highest level in over thirteen years. This projected surge is not just cyclical. It is driven by a deeper structural shift in how healthcare is being consumed, funded, and prioritized.

Tailwinds Behind the Trend

Several forces are contributing to the projected rise in healthcare expenditure:

Rising drug costs and inflation are pushing overall healthcare bills higher

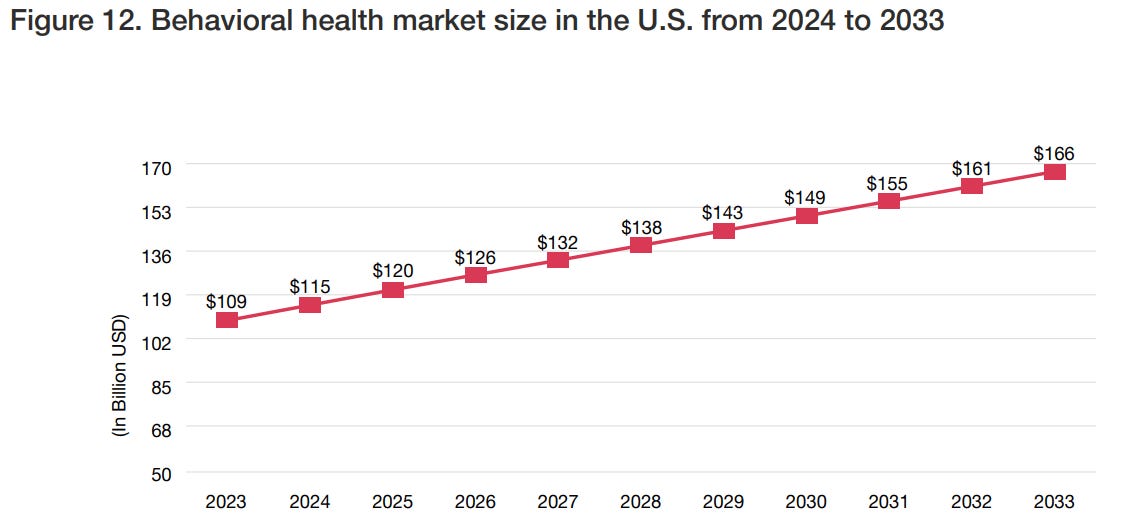

Greater acceptance and expansion of behavioral health services, which are expected to reach 166 billion dollars by 2033

A cultural shift toward preventive care and wellness, particularly among younger generations

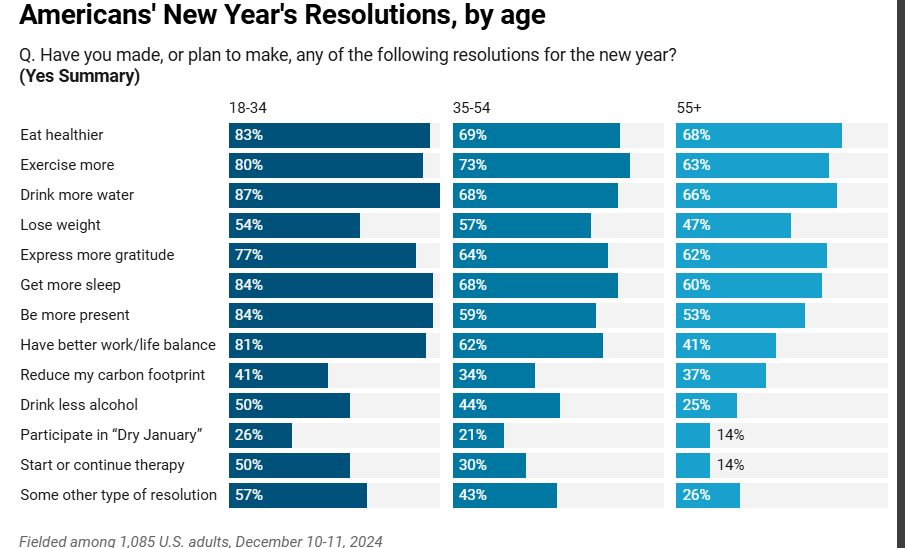

This transformation is visible in consumer behavior. A recent IPSOS poll shows that younger Americans are increasingly focused on health related goals such as eating better, exercising more, and staying hydrated. The majority of top New Year’s resolutions across all age groups now center around health, indicating growing demand for wellness services, diagnostics, and access to care.

Why This Matters for UnitedHealth

As the largest health insurer and one of the most vertically integrated healthcare companies in the United States, UnitedHealth is positioned to capture and scale with this trend. Its Optum segment in particular is aligned with high growth categories such as data driven care delivery, pharmacy benefit management, and behavioral health solutions.

In short, the rising tide of healthcare spending will not just support UnitedHealth’s current model. It could expand its addressable market significantly. As spending increases and more Americans seek care across a wider spectrum of services, UnitedHealth’s scale and reach will likely become even more valuable.

Dividend Strength and Longevity

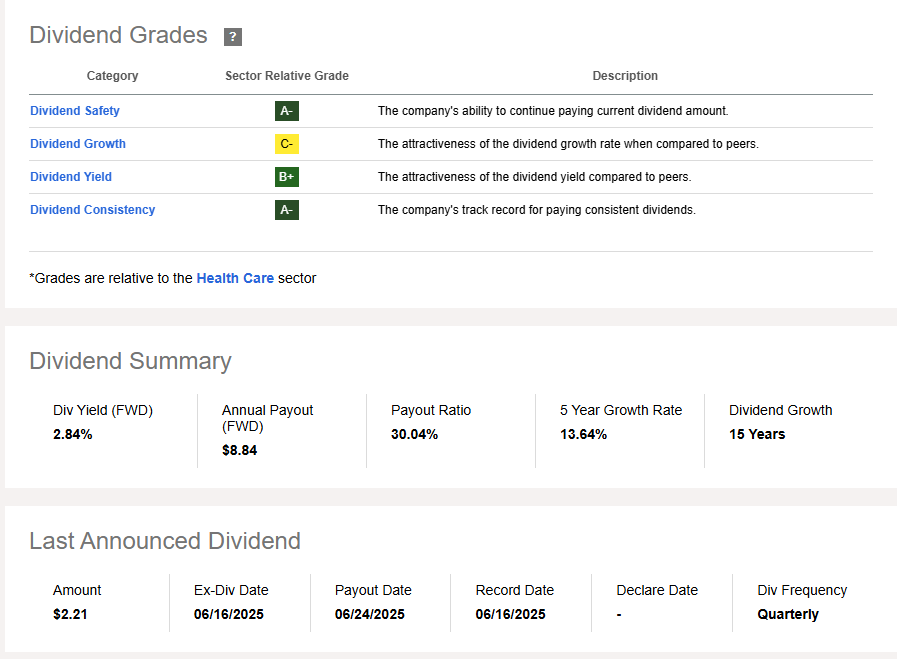

UnitedHealth Group continues to be a standout dividend payer in the healthcare sector, combining safety, consistency, and respectable growth. With a forward dividend yield of 2.84% and a 30% payout ratio, the dividend is not only sustainable but also leaves ample room for continued growth and reinvestment in the business.

The company currently pays an annualized dividend of $8.84 per share, broken into quarterly payments of $2.21, with the most recent ex-dividend date on June 16, 2025 and the payout scheduled for June 24, 2025.

Here’s how UNH scores across several key dividend categories relative to its healthcare sector peers:

Dividend Safety:

The dividend is well-covered by earnings, with no risk of cuts based on current fundamentals.Dividend Consistency:

UnitedHealth has now increased its dividend for 15 consecutive years, showing a strong commitment to returning capital to shareholders.Dividend Yield:

While not the highest-yielding stock in the market, its yield is attractive given the company’s defensive business model and long-term reliability.Dividend Growth:

The one weaker point is relative growth. The five-year dividend growth rate stands at 13.64%, which is solid in absolute terms but slower compared to some higher-growth peers in the sector. Nonetheless, the growth rate remains well above inflation and signals a reliable upward trend.

Risks Are Real but Manageable

Yes, there are risks. The DOJ investigation may result in fines or future compliance requirements. The recent increase in Medicare Advantage care utilization caught management off guard. The company also faces political risk and regulatory pressure in a sector that often draws criticism.

But the fundamentals have not been broken. These risks, while real, appear to be more headline driven than structural. And based on the current valuation, the market seems to be pricing in a worst-case scenario that may never come to pass.

Final Thoughts

UnitedHealth Group remains a dominant force in healthcare. It offers a rare combination of scale, recurring revenue, consistent earnings, and long-term growth.

While the stock may continue to see near-term volatility, investors who are patient and long-term oriented now have the chance to buy one of the best-managed companies in the industry at its lowest valuation in more than ten years.

This is not a trade. It is a long-term investment opportunity backed by fundamentals, margin of safety, and a business that millions of Americans rely on every day.

Always invest in crooked companies.

They do great!