Wall Street Has You Brainwashed About Retirement.

A silent shift in the market just broke the old rules. Here is how dividend investors are buying back their time today.

A silent shift in the market that reveals a massive problem, and what it means for your financial freedom.

For decades, the ultimate American financial finish line was perfectly defined. You just needed one million dollars. The advice was simple: buy an S&P 500 index fund SPY 0.00%↑, wait thirty years, hit that seven figure milestone, and you are completely safe.

While this strategy is still valid for hitting that 7-figure market, I believe it just isn’t good enough.

Inflation is quietly eating the dollar alive. The cost of housing, food, and energy has fundamentally detached from standard wage growth. A million dollars in an S&P 500 fund simply does not provide the purchasing power it did ten years ago. If you try to live off the traditional 4% rule today, a million dollars gives you about $40,000 a year to spend for the rest of your life. Unless you want to live in the middle of Arkansas, this won’t work.

The long term promises of traditional retirement are still being sold to you, but they have been moved to second place behind immediate financial survival.

Wall Street is telling you: this is a cash flow environment now. And the people who still treat it like a thirty year waiting game are going to keep wondering why their massive net worth feels utterly useless in the real world.

Wall Street Has You Brainwashed

I hear the constant defense of the traditional S&P 500 strategy every single day. We are all carrying some version of this index fund brainwashing.

But let us look at exactly why Wall Street pushes this specific narrative so hard. They want you to blindly set up an automatic transfer into a broad index fund and never look at it again for thirty years. Why? Because institutions collect steady, predictable management fees the entire time your money sits locked in their ecosystem.

Do not get me wrong. Parking your money in a broad index is a highly efficient way to invest. It takes zero thought, zero effort, and over a long enough timeline, the market generally goes up. For the average person who wants to completely ignore their finances, it is a fine default option.

But efficient does not mean it is the best way to invest.

A 10% gain on a digital brokerage statement does not help you when your cost of living skyrockets and you have zero cash to pay for it without selling your actual shares. When you park all your money in a pure growth index, you are giving up total control of your cash flow. You are locking your wealth in a vault and handing Wall Street the key.

If you actually want to buy back your time before you turn sixty five, you have to break the programming. You need an income stream you actually control, one that scales up to meet your real world expenses today, instead of paying an institution to hold your money hostage for decades.

Three Types Of Assets That Actually Perform

I have been watching this closely, and if you want to build a “Fire Me” fund that survives inflation, you need to step outside the standard S&P 500 box. You cannot just pick one strategy. You need three distinct engines working together:

1. The Tech Growth Engine

I know I just spent an entire section warning you about the trap of pure growth index funds. But let us be brutally honest. You absolutely need tech in your portfolio. Historically, the technology sector has consistently outperformed the broader market, and it is the primary asset class that keeps your growth momentum rolling through every bull market. You can choose from the highest quality Mag 7 companies, which I believe to be:

Amazon AMZN 0.00%↑

Meta Platforms META 0.00%↑

Nvidia NVDA 0.00%↑

Microsoft MSFT 0.00%↑

Alphabet GOOG 0.00%↑

I personally hold most of these companies because I believe these to be the leaders. Outperforming the market and beating the estimated annual returns of 10% doesn’t have to be complicated.

However, The Invesco QQQ Trust QQQ 0.00%↑ gives you direct, aggressive exposure to the Nasdaq 100. It captures that relentless momentum and ensures your overall net worth keeps expanding fast enough to outpace inflation, while the rest of your portfolio prints the actual cash you live on.

2. The Monthly Cash Printer

You cannot pay for gas with the theoretical value of QQQ. You need an actual cash printer. This is where the Goldman Sachs Nasdaq-100 Core Premium Income ETF GPIQ 0.00%↑ comes in. GPIQ holds those exact same tech companies, but it uses a covered call strategy to generate a massive, double digit yield paid out to you every single month. It literally turns tech sector volatility into usable cash.

I previously published an article dedicated to GPIQ if you want to learn more.

Highest Quality Option ETFs You Can Use To Build Passive Income Forever

Generating consistent passive income is a cornerstone of long-term financial independence. While traditional dividend stocks and bonds have long been favored, the evolution of Exchange Traded Funds (ETFs) has introduced innovative strategies, particularly those leveraging options, to deliver enhanced income streams.

3. The Real Asset Hedge

When inflation hits, physical commodities and infrastructure get incredibly expensive. You want to own the toll roads of the energy sector. The NEOS MLP & Energy Infrastructure High Income ETF MLPI 0.00%↑ tracks master limited partnerships that physically move and store oil and gas. These are hard assets that generate massive cash flows, providing a huge, double digit yield and a perfect defensive shield when the cost of living spikes.

Your investments are not standalone lottery tickets. They are connected pieces of a bigger picture that builds a cash flow snowball over time.

I recently issued a buy alert on MLPI. Since then, the stock has provided monthly cash flow and outperformed the S&P 500.

Buy Alert!🚨 How To Get 15% Yields From The Energy Crisis

There is one transaction we all participate in, whether we like it or not.

Your Action Plan For Tomorrow Morning

Do not just read this and go back to blindly funding your 401(k). I want you to log into your brokerage account tomorrow morning and run a simple audit. Look at your total portfolio value, and look at your annual dividend income.

If your yield is sitting at 1.5%, you are completely exposed to inflation. You need to start reallocating capital into cash flowing assets today.

Get a shortcut on your investing journey with this starter guide. You can get the dividend starter bundle so that you can skip the mistakes that I made on my way to $40,000 a year in passive dividend income.

👉 Here is what’s included:

✅ The Dividend Blueprint (ebook)

A step-by-step guide showing how I structure my portfolio, grow monthly cash flow, and reinvest for long-term income.✅ Monthly Dividend Map

50+ hand-picked tickers that pay monthly so you can ladder your income all year long.✅ Dividend Tracker (Google Sheet)

The exact spreadsheet I use to track yield, forward income, reinvestment, and portfolio growth.✅ Dividend Growth Legends: 50+ Stocks

50 stocks that have an established history of dividend increases.✅ List of ETFs for Beginners To Start With

The monthly practice that changes everything

I know what some of you are thinking. “I cannot live on dividends right now. I do not have enough invested.”

You do. You just have not built the habit yet.

Great investors treat tracking their forward dividend income as a practice. It is a way to notice progress, collect momentum, form discipline, and sharpen their mindset.

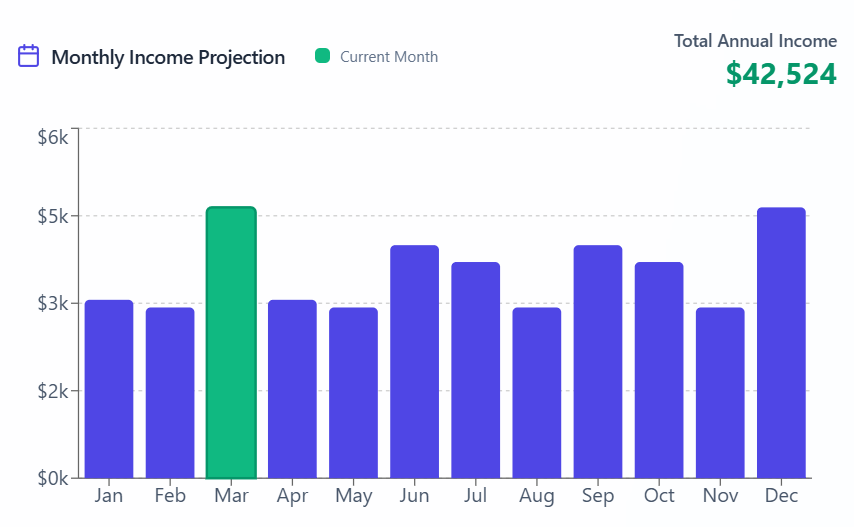

I track my monthly dividends with the Yieldly Dashboard. I am estimated to collect more than $42K in dividends this year.

👉 Unlock Access To Yieldly By Upgrading Your Membership. Yieldly allows you to track your monthly dividend income.

Your dividend tracker can be exactly that for you. Three or four minutes a month logging your new payouts. Seeing that your portfolio now covers your Netflix subscription. Noticing that next month, it will cover your water bill. You start to feel like you actually own your time, because you do.

The Real Shift

The most important change does not happen in the broader economy. It happens in your head.

It is the exact moment you stop treating your portfolio like a distant retirement vault and start treating it like a replacement paycheck. When you finally get that first dividend deposit that covers your electric bill, the entire game changes. You stop hoping for a safe retirement and start actively buying back your time today.

Stop letting Wall Street hold your money hostage. Start building your cash flow engine today.