What If Your Portfolio Paid You More Than Your Job?

The Mental Shift That Changes Everything & How To Get There Step By Step

Most people never ask this question because they don’t even know that it’s a possibility.

What if your portfolio paid you more than your job? Not someday. Not at retirement. Right now.

Imagine checking your account and seeing cash deposits that cover your rent, your groceries, your life. And imagine that money showing up without a boss, without a schedule, without needing permission. That’s the shift I experienced when my investments started generating more income than I used to earn at my job.

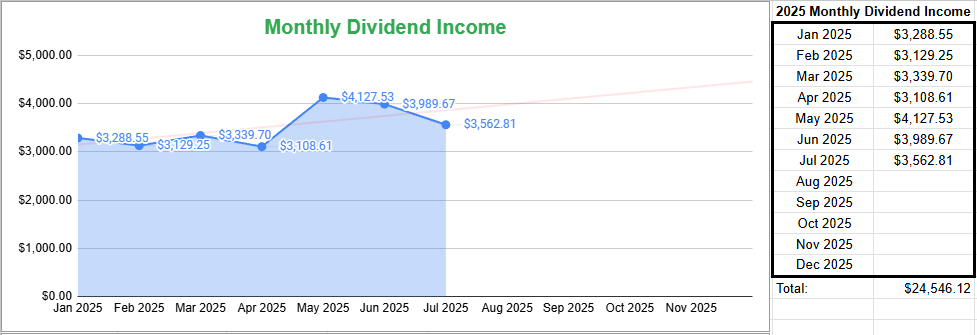

For the month of July, I was able to collect $3,562 in dividend income. This income grants me more control… If you are interested in this kind of practical wealth-building strategy, consider becoming a paid subscriber for deeper breakdowns and weekly income tools.

Control of my time. My schedule. My decisions.

We’re taught to trade time for money. But what if you could flip that equation and build income that works while you sleep. I want to walk you through the mindset behind income freedom. What if I’m able to grow my dividend income stream up to $10,000 a month? Then $20,000. Then $30,000. What would you do if you had an extra $30,000 a month?

I’ll show you the math, the milestones, and the exact types of assets I used to turn my portfolio into a paycheck. Because once you stop depending on work to pay your bills, everything about your life starts to change.

For paid subscribers only, I’ll be sharing my exact dividend income and holdings allocation at the end of every month.

The Problem with Traditional Thinking

From the time we are kids, we are trained to think like workers. The programming started in the classroom. The programming taught you to remain overly patient with your goals. The programming taught you how to suppress your emotions and ambitious because ‘good things take time’. Yet, we have grown adults who are impatient with everything else in their life: their relationships, raising children, mild inconveniences like traffic.

Go to school.

Get a job.

Trade your time for a paycheck.

Save what is left.

Maybe retire at sixty five if everything goes right.

Even most investors think this way. Hell, most people think this way.

They build portfolios that focus on growth with no real plan for income. They are told to wait. Keep saving. Let compounding do the work and one day, they might be able to draw down a few percent each year and call it retirement. Pathetic.

The Math Behind Replacing Your Paycheck

Financial freedom is not magic. It is math.

To stop relying on a job, you need your investments to generate enough income to cover your core expenses. That is it. No guesswork. No spreadsheets full of projections. Just a few clear targets.

Here is how I break it down.

$500 per month can cover groceries or utilities

$1,000 per month can handle rent in a modest city

$2,000 per month gets you close to covering basic living expenses

$3,000 to $4,000 per month gives you real autonomy

$5,000 per month and beyond means work becomes optional

Let’s say you want to generate $3,000 per month, or $36,000 per year. With a yield of 12%, which is achievable using a blend of option ETFs, high yield funds, and strategic leverage, you would need around $300,000 allocated.

If your yield is higher like 18 to 20%, that same dividend income could come from just $180,000 to $200,000.

That is not pocket change, but it is a far cry from the idea that you need one or two million dollars saved before you can think about living off your portfolio. The key is efficiency. You do not need to retire in the traditional sense. You just need to make your portfolio work harder than you do.

When you start measuring your income in weeks or even days instead of quarters, you can begin building a real alternative to your paycheck.

But that model is broken. It relies on one thing that is never guaranteed: time.

People tend to think their job is their only reliable source of income, and they treat investing as a future plan. But income does not have to be delayed. With the right strategy, it can become your primary engine. The moment you stop seeing your job as your lifeline and start viewing your portfolio as a cash machine, everything shifts.

The First Time My Portfolio Paid More Than My Paycheck

There was no applause. No fireworks. Just consistency over 7 years of quietly putting money away into my brokerage account. My first job out of college paid me $3,000 a month. This year I’ve been able to average a monthly dividend income of $3,500 a month.

It feels unreal.

Not because the number is massive, but because of what it means. My money is now working harder than I was only a few years ago. I am no longer dependent on an employer. I am not trading my hours for income. I created something that could run with or without me.

Highest Quality Option ETFs You Can Use To Build Passive Income Forever

Generating consistent passive income is a cornerstone of long-term financial independence. While traditional dividend stocks and bonds have long been favored, the evolution of Exchange Traded Funds (ETFs) has introduced innovative strategies, particularly those leveraging options, to deliver enhanced income streams.

For some people, it starts small. Maybe your portfolio covers your rent for the first time. Maybe it pays your car insurance. Maybe it covers a vacation without touching your savings. Then it snowballs. You start to see money differently. You start to think in systems instead of labor. You stop chasing promotions and start buying more time.

The funny thing is that the number is less important than the feeling.

Even if you are earning just one hundred dollars a month from your investments, that is one hundred dollars you did not have to work for. That is leverage. That is freedom starting to grow.

The 5 Income Tools That Replaced My Paycheck

Replacing your paycheck is not about guessing. It is about using the right tools.

You need assets that generate consistent, high yield income and not just capital appreciation. Here are the tools I use to create weekly and monthly cash flow.

These 5 Types of High Yield Dividend Stocks Can Pay You Monthly

The traditional advice used to work. Save diligently. Buy blue-chip stocks. Withdraw four percent a year and live comfortably in retirement. That used to be enough. But in today’s world, it is no longer a reliable strategy.

1. Option Income ETFs

These funds use covered calls or synthetic option strategies to produce yield. Many pay weekly. Some target single stocks like Tesla or Apple. Others track the S&P 500 or Nasdaq. The key is that they monetize volatility and pass the premiums on to you.

2. Business Development Companies

BDCs like MAIN or ARCC lend to small and mid-sized businesses and pass through nearly all their earnings as dividends. Yields can range from 9 to 14 percent. They are excellent for monthly income and can be more stable than option funds in certain market conditions.

3. Preferred Stock and REIT Funds

These offer exposure to steady income through real estate and preferred equity. They are ideal for adding durability to your yield stack, especially when paired with more aggressive instruments.

4. The Dividend Wheel

This is the strategy I use to take weekly payouts and roll a portion into long term growth. Instead of spending every dollar, I allocate some toward positions in companies like Google and ASML. This creates a flywheel effect — income funds growth, and growth fuels more income.

5. Strategic Use of Margin

Used carefully, margin can boost your income without requiring new capital. The idea is to borrow against your existing positions at low rates and use that to buy more income-producing assets. This adds risk, but when done correctly, it accelerates the process.

None of these tools are perfect in isolation. But when combined, they can turn a passive portfolio into an active source of real income. That is how I designed mine, not for retirement, but for freedom now.

The Psychological Shift

When your portfolio starts paying you more than your job, the numbers are only part of the story. The real change happens in your mind.

You stop waking up with pressure. You start making decisions differently. You no longer ask, "Can I afford this?" You ask, "Do I even want it?"

You become harder to control. You become more selective with your time. You work on things because they matter, not because you need the money. I was able to quit jobs simple because I didn’t feel like working them anymore. That kind of power gives you the ultimately confidence boost that you can do anything you want. I can pour all of my time into whatever endeavor that I want and there’s no longer a job getting in the way of my time. No more useless meetings and team calls.

This shift is what financial independence is really about. It is not about sitting on a beach doing nothing. It is about operating from a place of strength.

When you rely on a job, every choice you make is filtered through risk.

What if I get fired?

What if I cannot take time off?

What if I do not get the raise?

What if this spreadsheet is wrong?

When your income comes from your portfolio, those questions disappear. You are no longer working to survive. You are building because you want to.

This is not just financial freedom. It is mental freedom.

Once you experience it, you will never think about money the same way again.

What To Do Next

You do not need to wait until you have a six figure portfolio to start building income. You can begin now, even with a few hundred dollars.

Here is what I recommend.

Start with one payout.

Find a weekly or monthly paying ETF and track the income. Feel what it is like to get paid without working for it.

Stack your income.

Add a second fund that pays on a different day. Then a third. Build toward a rhythm of income that shows up predictably.

Here's How To Get Paid A Dividend Every Day

Most investors wait months to collect dividends. Some only see cash a few times a year. But there is a smarter way to invest if your goal is regular income.

Track your progress.

Keep a monthly total of how much your portfolio pays you. Watch that number grow. Celebrate every milestone — even the first ten dollars.

Reinvest for speed.

Use part of your income to buy more shares or build long term growth positions. That is how you turn income into wealth.

Stay consistent.

This is not a get rich quick strategy. It is a freedom engine. The more you fuel it, the more your time becomes your own.

Most people will never experience what it feels like to get paid without clocking in. But you can. And once you do, you will never go back.

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

Super informative and exactly what I’ve been looking for! Thank you!

This is a great post and easy to follow! Keep up the great work, Cain! I see some Pho in your future! LOL!