Worried About Buying Stocks at the Top? Here’s How Dividend Investors Stay Safe

From reliable dividends to high-quality growth, here’s how to stay safe near market highs.

Market indexes continue to hover near all time highs, which has caused all of these gurus to start predicting doom. Every headline made it sound like stocks have nowhere to go but down. There are folks overlaying the chart from 2008’s market crash, onto the current market. They are trying to draw similarities that indicate markets will experience a similar crash.

red line = 2025

blue line = 2008

But here’s what I learned: the people who actually build lasting wealth don’t wait for the perfect entry. They build strategies that work whether the market is making new highs or sliding lower. That’s exactly where dividends come in.

Dividends flip the script. Instead of worrying about whether the market is due for a correction, you are collecting steady income regardless of what the index is doing. While traders stress over every dip, dividend investors get paid to wait.

The real question isn’t “Is this the top?” The real question is “How do I structure my portfolio so I can stay safe and keep collecting income even if it is?”

I collected nearly $4K in dividends in August. I will share how I am reallocating that capital to put myself in a position to ride out any risks of a market pullback.

August 2025 Dividend Report

For the month of August, my dividend portfolio paid me $3,991.11 in dividend income. On a year-to-date basis, I’ve now collected over $28,000 in passive income with dividends. I aim to accumulate $100,000 annually in dividends and I want you to join me on the journey. This is money that I didn’t have to actively work for and doesn’t include capital earned through other business ventures.

Macroeconomic Data Doesn’t Indicate A Crash Is Likely

Whenever markets push toward all-time highs, the biggest fear investors have is that we’re sitting on the edge of another crash. The headlines feed into this narrative because fear sells. But when you look at the actual data, it paints a much calmer picture.

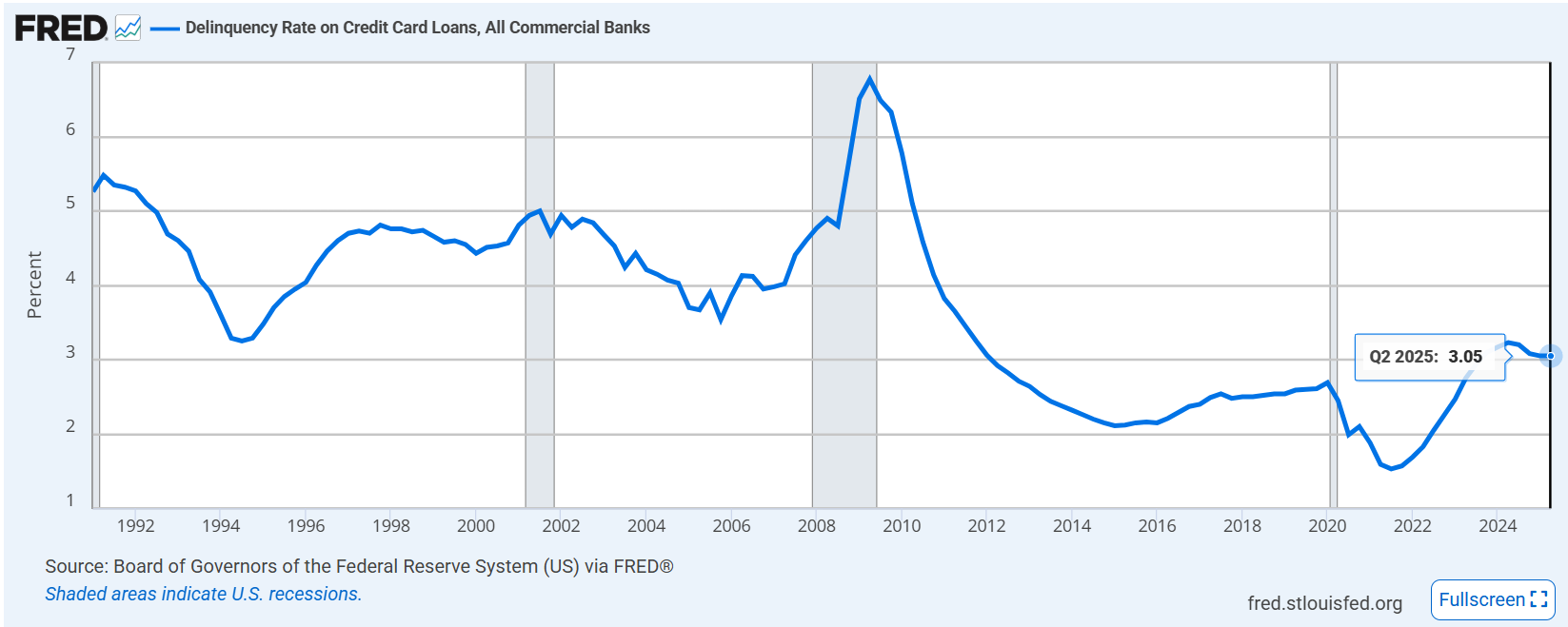

Start with delinquencies. At just over 3 percent, delinquency rates on credit card loans remain historically low. To put that into perspective, they were nearly double this level during the financial crisis of 2008–2009. Even as interest rates climbed and borrowing costs increased, consumers have continued making payments. That tells us two important things: household balance sheets are healthier than many assume, and banks aren’t seeing the kind of stress that usually precedes a major downturn.

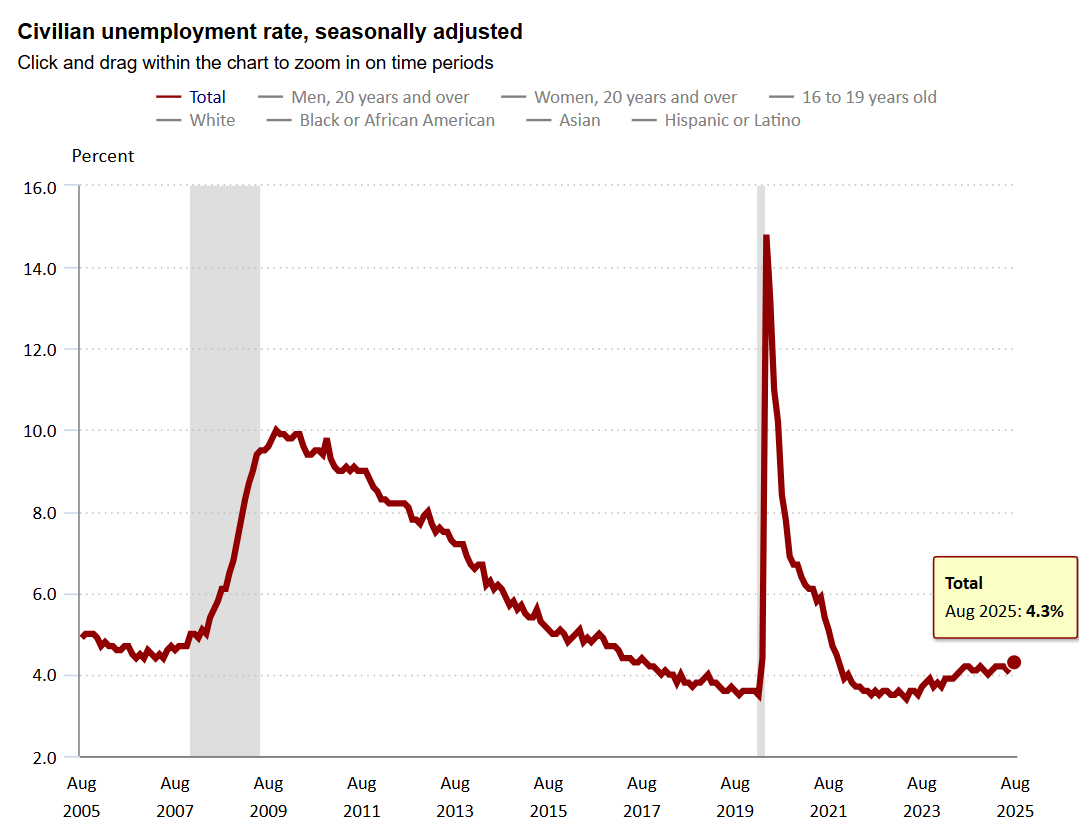

Now look at the US unemployment numbers below. The rate currently sits just over 4 percent, a touch higher than the post-pandemic lows but still firmly in the range of a healthy labor market. Unemployment only becomes a serious red flag when it climbs past 6–7 percent and stays there. Right now, the labor market remains resilient, with job openings still plentiful across many industries. That resilience means wages continue to flow, consumer spending remains intact, and businesses still have the ability to support earnings.

Combine these two signals: low delinquencies and low unemployment, and you get a very different conclusion than the doom-and-gloom headlines suggest. Instead of teetering on collapse, the economy looks more like it’s stabilizing at a steady pace.

For dividend investors, this backdrop is critical. It means corporate cash flows are not under severe stress, which supports ongoing dividend payouts. In fact, many companies continue to raise dividends because they have the earnings power and balance sheet strength to do so. This is why market volatility should be seen as noise rather than an existential threat. A steady economy with manageable consumer debt and strong employment provides the foundation that dividend strategies thrive on.

What Kind of Dividend Companies to Focus On

Essential Service Providers

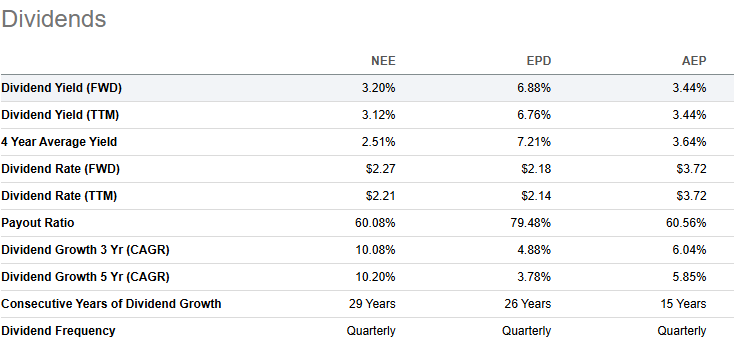

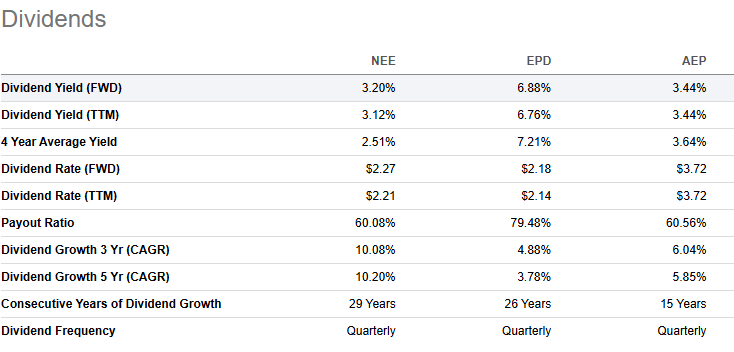

Utilities, telecoms, and infrastructure firms that provide must-have services. These are businesses that provide services that are essential to our quality of life. Things such as water, electric, fuel, transportation, etc. Their revenues are steady no matter what the market does. Here are some of my personal favorites.NextEra Energy NEE 0.00%↑

Enterprise Products Partners EPD 0.00%↑

American Electric Power Company AEP 0.00%↑

The Utilities Select Sector SPDR Fund ETF XLU 0.00%↑

High-Quality Business Development Companies

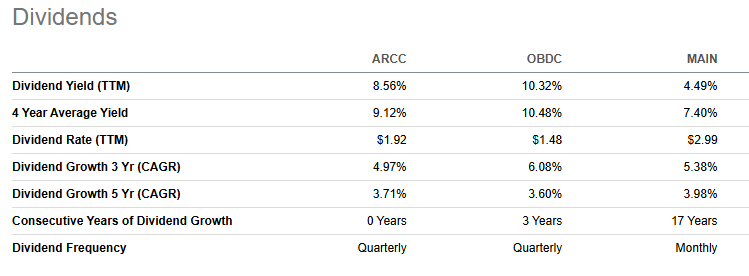

Firms like ARCC or well-managed income funds that generate above-average yields but have proven track records of protecting NAV and paying through different cycles. Business Development Companies are firms that lend out money to businesses looking to expand operations. In return, they collect interest income from these loans and pay out a portion of this income to shareholders as a dividend. Here are some of the BDCs that I currently hold. BDCs tend to have much higher dividend yields.Ares Capital ARCC 0.00%↑

Blue Owl Capital OBDC 0.00%↑

Main Street Capital MAIN 0.00%↑

Dividend Growers

Even if the market pulls back, companies with long histories of increasing payouts (think consumer staples, healthcare leaders, or “dividend aristocrats”) offer protection against inflation and volatility.Microsoft MSFT 0.00%↑

Apple AAPL 0.00%↑

Broadcom AVGO 0.00%↑

Coca-Cola KO 0.00%↑

PepsiCo PEP 0.00%↑

Target TGT 0.00%↑

Verizon VZ 0.00%↑

General Dynamics GD 0.00%↑

Johnson & Johnson JNJ 0.00%↑

Covered-Call Funds / Option Income ETFs

In sideways or choppy markets, these can shine because they generate income from volatility itself, providing cash flow even when prices stagnate. So even if markets decline, these funds may be better suited to navigate the uncertainty. I recently shared an article talking about these option ETFs. You can check that out below.

If you’re serious about building steady, predictable cash flow from dividends, this guide is the best place to start.

I’ve put together a curated, research-backed list of WEEKLY & MONTHLY paying option ETFs, designed to help you create reliable income every single month:

✅ ETFs that actually pay WEEKLY and monthly, not quarterly

✅ Estimated yields commonly above 30%. Dividend yields can be as high as 100%.

✅ My top picks for consistent income engines

✅ Includes newer, high-yield option income funds from the YieldMax suite, Roundhill, NEOS, Kurv, and Goldman Sachs

The Dividend Safety Checklist

Whenever I analyze a dividend-paying stock or fund, I run it through a quick checklist. The goal is simple: make sure the income is not just high, but reliable. Chasing yield alone is a recipe for disappointment. Here are the four pillars I look at:

*Paid plan discount ending 9/11/25

1. Payout Ratio

How much of a company’s earnings are being returned to shareholders as dividends. A healthy payout ratio is usually under 75% for stocks, though certain funds and REITs can run higher. The key is making sure earnings comfortably support distributions.

2. Dividend Coverage

For funds, I check net investment income (NII) or funds from operations (FFO) against the dividends paid. If coverage sits above 100%, the distribution is safe. If it drops below that, there’s a chance the payout could be cut.

3. NAV Stability

Closed-end funds and option ETFs live or die by how well they preserve net asset value (NAV). A declining NAV can mask unsustainable payouts. If NAV is flat or growing, it’s a green flag.

4. Leverage Levels

Leverage refers to the level of debt that a company uses to amplify earnings. Leverage can amplify returns, but it also magnifies losses. I prefer funds with moderate leverage (10-20%) that is mostly fixed-rate, so rising interest rates don’t erode income.

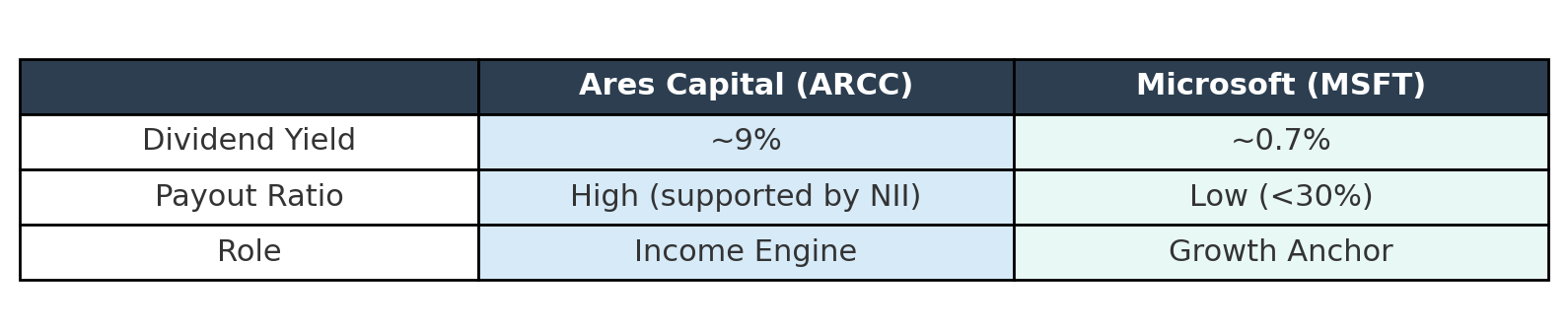

Income Today, Growth Tomorrow

When you structure a dividend portfolio, it helps to think in terms of two roles: the income engine and the growth anchor. Ares Capital (ARCC) and Microsoft (MSFT) are perfect examples of this balance.

ARCC represents the income engine. With a yield near 9% and distributions supported by net investment income, it pays you generously in the present. Its portfolio of senior secured loans and conservative management make that income relatively stable, even during choppy markets. ARCC’s job is simple: to deliver consistent cash flow that can be used as spendable income or reinvested elsewhere.

MSFT, on the other hand, is the growth anchor. Its payout ratio sits below 30%, meaning most of its massive earnings are reinvested back into the business. The dividend itself is modest, but it grows steadily year after year, compounding into meaningful income over time. Microsoft’s AAA credit rating and fortress balance sheet make it one of the safest long-term dividend growers in existence.

Together, ARCC and MSFT illustrate how to build a portfolio that isn’t dependent on timing the market. ARCC funds your lifestyle today, while MSFT quietly builds wealth for tomorrow. That combination is how dividend investors stay safe at market highs: they get paid in the short term without sacrificing the future.