YieldMax Vs. Roundhill Weekly ETFs

Two ETF issuers are redefining how often investors get paid. Here’s how their weekly dividend strategies actually compare.

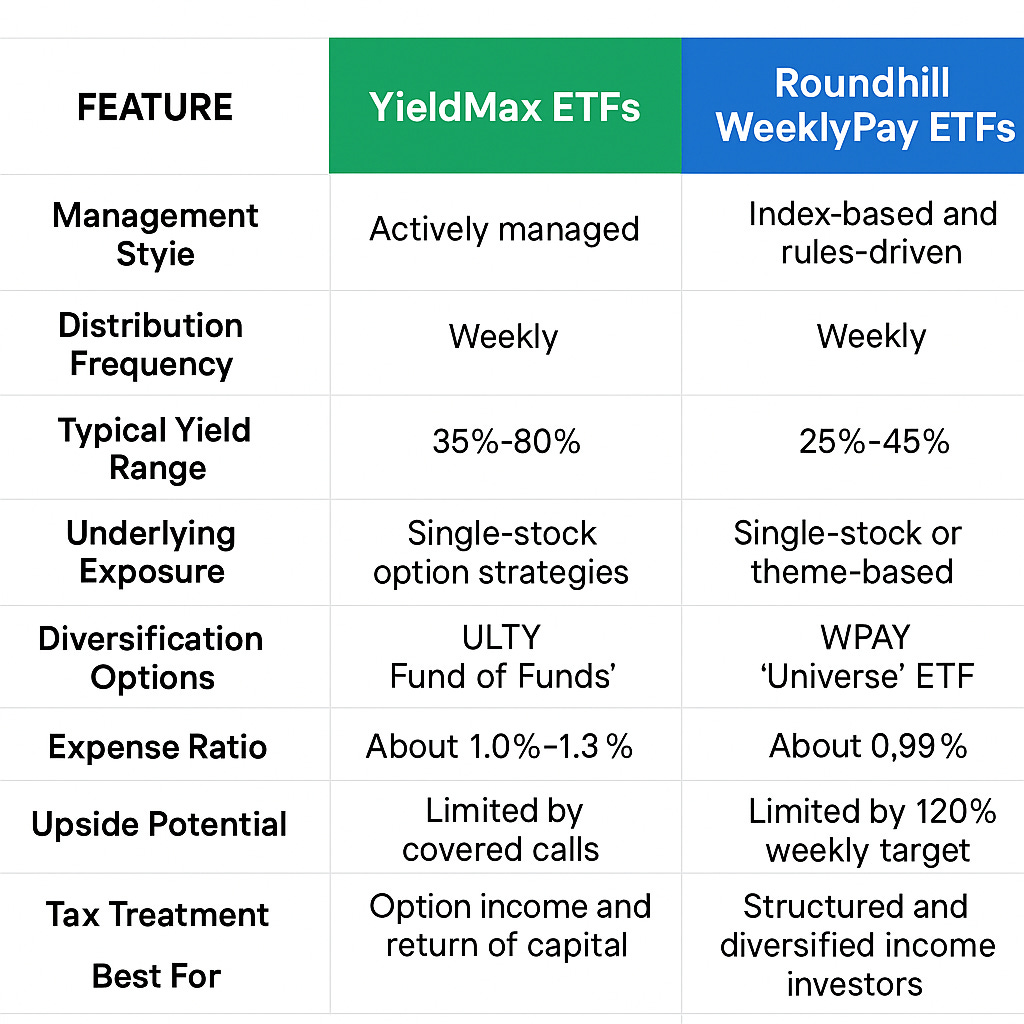

TL;DR - YieldMax and Roundhill are the two main players driving this trend, but their strategies differ in both structure and outcome.

👉YieldMax = higher yields, higher risk, more active management.

👉Roundhill = smoother performance, more predictable results, less volatility.

👉Both can play a role in a diversified Weekly Income Portfolio depending on whether your goal is maximum cash flow or steady total return.

The YieldMax Approach

YieldMax was the first to bring high-yield, single-stock option income ETFs into the spotlight. Each fund is tied to a specific company such as Tesla, Nvidia, or Amazon and generates income by writing covered calls on those stocks. However, most of the YieldMax funds don’t actually hold common shares of the equities they are writing options against, which is known as a synthetic option writing strategy.

These underlying companies are among the most volatile in the market, which means the options tied to them carry high premiums. YieldMax collects those premiums and distributes them to investors, often resulting in double-digit or even triple-digit annualized yields.

Today, nearly all of YieldMax’s products pay investors weekly. This means investors can begin seeing results in a matter of days rather than months. You can see the details around the recent shift below:

YieldMax Moves to Weekly Distributions — What It Means for Income Investors

YieldMax ETFs has announced a major update to its payout structure that will reshape how investors experience income from its suite of option-income funds. Beginning in mid-October 2025, all of YieldMax’s single-stock option income ETFs will transition from monthly to weekly distributions.

YieldMax funds are actively managed, which allows portfolio managers to adjust exposure and strike prices as conditions change. The drawback is that this constant activity can erode net asset value over time, especially during long bull markets when underlying stocks move sharply higher. YieldMax appeals most to investors who want to maximize short-term income and are comfortable accepting more volatility in exchange for that higher yield.

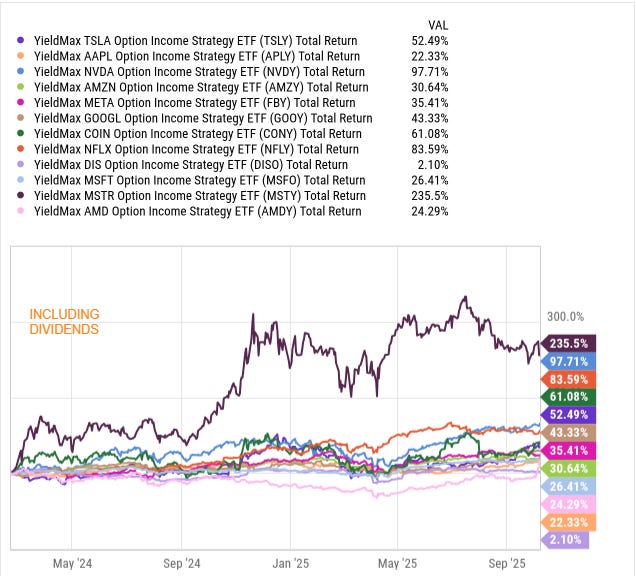

👉I pulled in the total return (including all distributions) of some of the most popular YieldMax ETFs that have the longest operating windows.

TSLY 0.00%↑ - APLY 0.00%↑ - NVDY 0.00%↑ - AMZY 0.00%↑ - FBY 0.00%↑ - GOOY 0.00%↑ - CONY 0.00%↑ - NFLY 0.00%↑ - DISO 0.00%↑ - MSFO 0.00%↑ - MSTY 0.00%↑ - AMDY 0.00%↑

So all of these funds would have provided a position total return when held over the last two years. So what’s the drawback to these funds? Well, they are known for the massive NAV erosion (share decline) over time.

👉Now here are the performance of those same ETFs, WITHOUT including all dividends paid. As we can see, they’ve ALL suffered from large share price declines.

The Roundhill WeeklyPay Lineup

Roundhill took a more systematic approach to the same idea of turning volatility into income. Its WeeklyPay ETF family operates under a transparent, rules-based framework that targets 120 percent of each stock’s weekly total return while distributing cash flow every Wednesday.

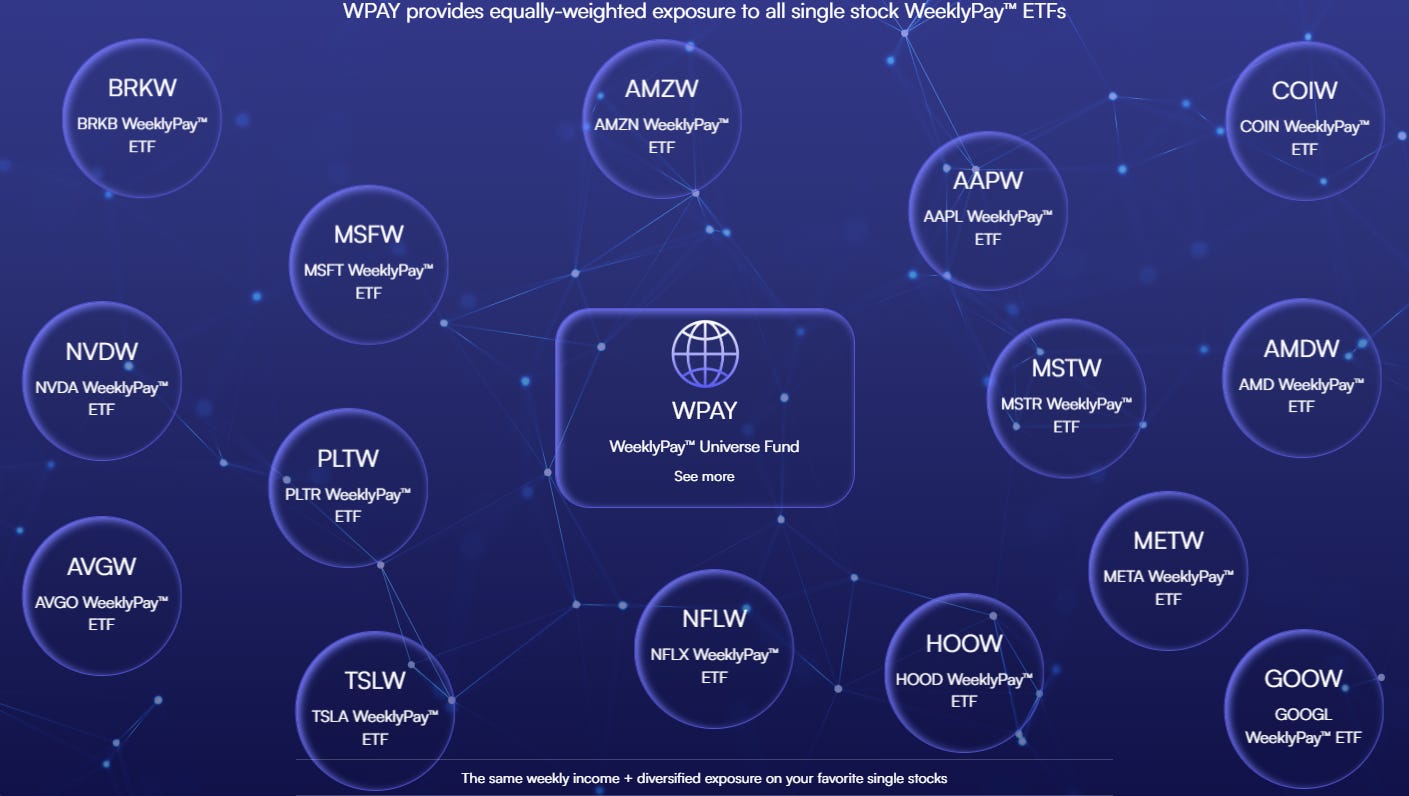

Rather than relying on active managers, Roundhill’s products follow clearly defined formulas designed to deliver consistency and diversification. The lineup includes the flagship Universe ETF that holds all WeeklyPay funds in equal weight, as well as specialized versions like AMZW 0.00%↑ for Amazon, MAGY 0.00%↑ for the Magnificent Seven tech giants, and YBTC, which converts Bitcoin’s volatility into income.

Roundhill’s funds typically yield between 25 and 45 percent depending on market conditions. Although that is somewhat lower than the highest-yielding YieldMax offerings, Roundhill’s structure helps preserve net asset value more effectively over time. The only problem is that the Roundhill funds have a much shorter operating history.

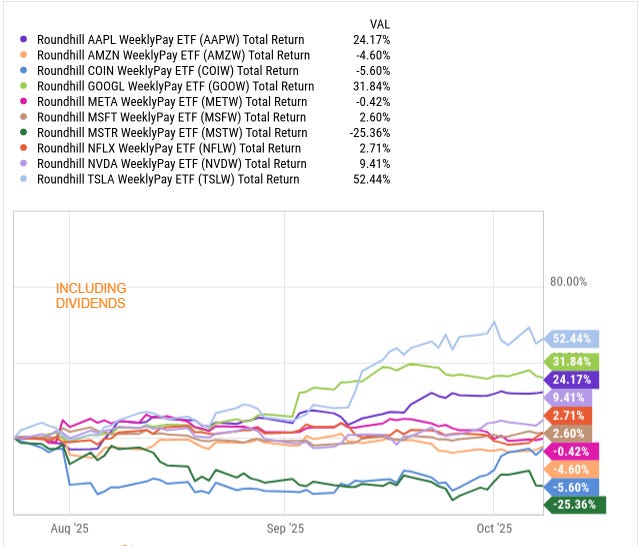

👉 Here is the performance of the Roundhill funds, INCLUDING all distributions paid.

AAPW 0.00%↑ - AMZW 0.00%↑ - COIW 0.00%↑ - GOOW 0.00%↑ - METW 0.00%↑ - MSFW 0.00%↑ - MSTW 0.00%↑ - NFLW 0.00%↑ - NVDW 0.00%↑ - TSLW 0.00%↑

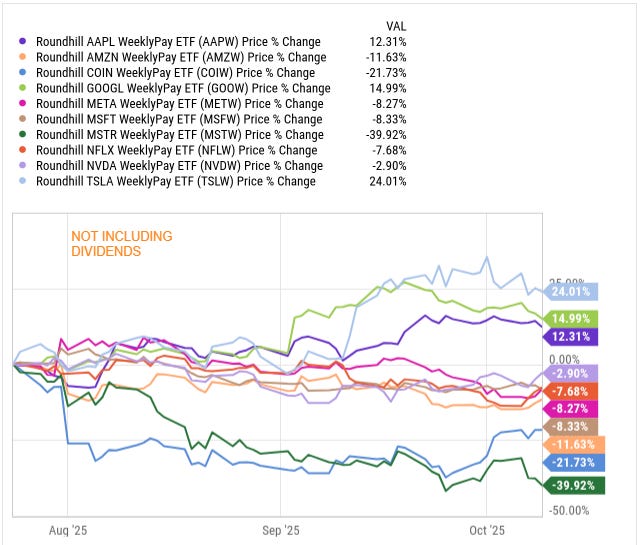

👉 Here is the performance of the Roundhill funds, NOT INCLUDING all distributions paid.

However, it’s incredibly hard to gauge how well these Roundhill funds are performing since their operating histories are so limited.

The benefit of Roundhill’s approach is predictability. Each fund automatically resets and rebalances, which eliminates the need for manual adjustments. Investors can simply hold their positions and collect steady weekly distributions.

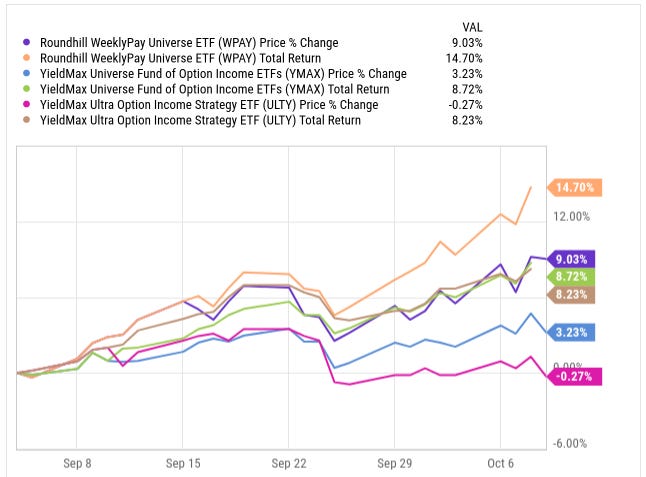

‘Fund of Funds’: ULTY, YMAX, WPAY

When we look at recent performance data, the differences between these two issuers become clear. The chart above tracks both price and total return for Roundhill’s WPAY alongside YieldMax’s ULTY and YMAX funds.

ULTY 0.00%↑ - YMAX 0.00%↑ - WPAY 0.00%↑

Over the past month, Roundhill’s WPAY has noticeably outperformed its YieldMax counterparts. WPAY delivered a total return of roughly 14.7%, with its price appreciation and distributions contributing nearly equally to that gain. In comparison, YieldMax’s ULTY produced about 8.2% in total return, while YMAX was close behind at 8.7%. On a pure price basis, WPAY also saw a stronger move higher, rising more than 9%, compared to flat or slightly negative results for ULTY.

This trend highlights one of the key distinctions between the two approaches. YieldMax funds tend to deliver exceptionally high yields but with limited upside and greater NAV drag over time. Roundhill’s WPAY, while offering a slightly lower yield range, captures more consistent total return by maintaining exposure to a broader basket of weekly-paying ETFs. The equal-weight structure of WPAY allows it to benefit from top-performing components like AMZW and MAGY without the same degree of single-stock concentration.

Discounted Annual Plan

✅ 10% off forever, even through future price increases – Lock in a discounted subscription rate. Exclusive access to all articles, buy & sell alerts, dividend income reports, occasional portfolio updates, and more.

3-Month Access + High-Yield Guide

✅ High-Yield Option ETF Guide + 3 months paid access – Your starting point for building predictable monthly income. 30+ different high-yield funds included.

Key Trade-Offs

YieldMax’s strategy focuses on maximizing income. It accepts greater volatility and the possibility of net asset value erosion in exchange for higher payouts. Roundhill’s structure aims for steadier returns and more predictable income, sacrificing some yield to achieve smoother long-term results.

Both issuers rely on complex derivatives to generate cash flow and both cap upside potential. They cater to investors who prioritize income frequency over capital appreciation. Choosing between them ultimately depends on your tolerance for volatility and your preference for active versus systematic management.

Quick question: is your system appropriate for retirees?

👀 👀