2 Funds That Offer Dividend Yields Above 10%

Collect Tax Free Dividends From These Two ETFs

I collected a five figure sum in dividends last year. A meaningful chunk of it never showed up as taxable income when I filed, because of one line buried in the tax documents that most income investors skip past:

👉 Return Of Capital.

Two funds are at the center of this. One is already in my portfolio, and I gave it a buy rating months ago. Since that post, the position is now up 14%. With the estimated growth of the AI Data Center market, I think this first position will continue to do very well.

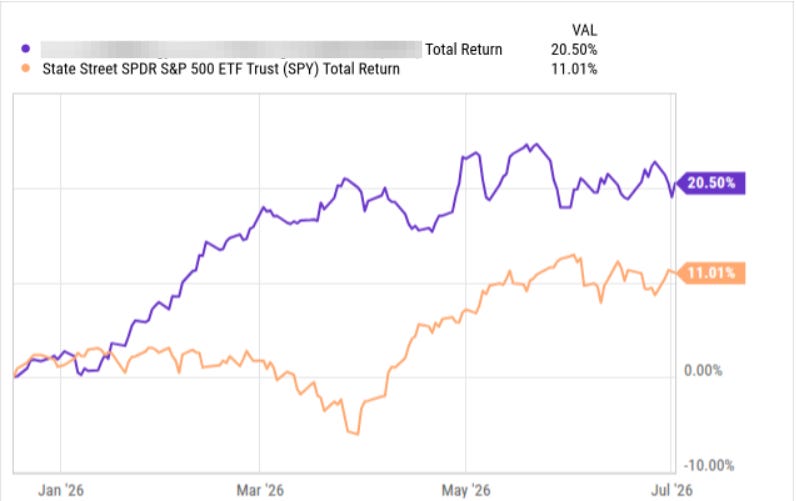

Since its inception, fund #1 has outperformed the S&P 500 index by a wide margin. However, the fund’s history here is VERY short so keep that in mind.

The second fund is brand new, and I am watching it closely before deciding whether to add it. This second fund offers a 13.5% dividend yield, while issuing those payouts on a monthly basis.

Today I want to walk through how both of them actually work, why the IRS treats their payouts differently than a normal dividend, and why that distinction is worth understanding before you chase any high yield fund.

Both funds classify most of their monthly distributions as return of capital, not ordinary income.

One fund has years of real distribution history behind it, and it is the one I actually own. The other launched in May 2026 and was engineered for this outcome from day one, but I have not added it yet.

Return Of Capital

Return of capital is a tax classification and it get’s a bad rep. Traditionally, return of capital is usually defined as when a fund fails to produce enough income to support dividends, so it pays you that dividend by returning your capital back to you.

However, this isn’t always true.

A fund can generate plenty of real economic income and still have some or all of a distribution classified as ROC, because of how that income is treated for tax purposes rather than how much of it actually exists. Depreciation on physical assets, the tax treatment of certain option contracts, and timing differences between when income is earned and when it is recognized for tax reporting can all push a distribution into ROC territory even when the fund’s underlying earnings fully support the payout.

When any portion of a distribution gets classified this way, the IRS treats it as a return of your own invested capital instead of taxable income, and lowers your cost basis instead of taxing you on it right away.

Here is the simple version. You buy shares at $10. The fund pays you $1 classified as ROC. Your cost basis drops to $9. You owe nothing on that dollar today. When you eventually sell, your gain gets calculated against that lower basis, which means the tax bill shows up later, and potentially at the more favorable long term capital gains rate instead of your ordinary income rate.

That is the entire mechanism. Cash in your account today, tax bill deferred, sometimes for years, sometimes permanently if the shares get passed to an heir and receive a stepped up basis at death.

The part most people get wrong is assuming ROC means the fund is quietly handing back your own money because it has nothing else to pay you with. Sometimes that is true, and it is worth checking. But in the two funds I am covering today, the ROC comes from the structure itself, not from a shortfall.

I am going to name both funds below and break down exactly how each one earns its ROC treatment. Paid subscribers get the tickers, my actual entry price in the fund I own, and the specific reason I have not added the second one yet.