BUY ALERT🚨: UBER Is 40% Undervalued

Record profits, 20%+ growth, $2.3 billion in quarterly free cash flow, and a stock near its 52-week low.

Imagine a business that just did all of this in 90 days.

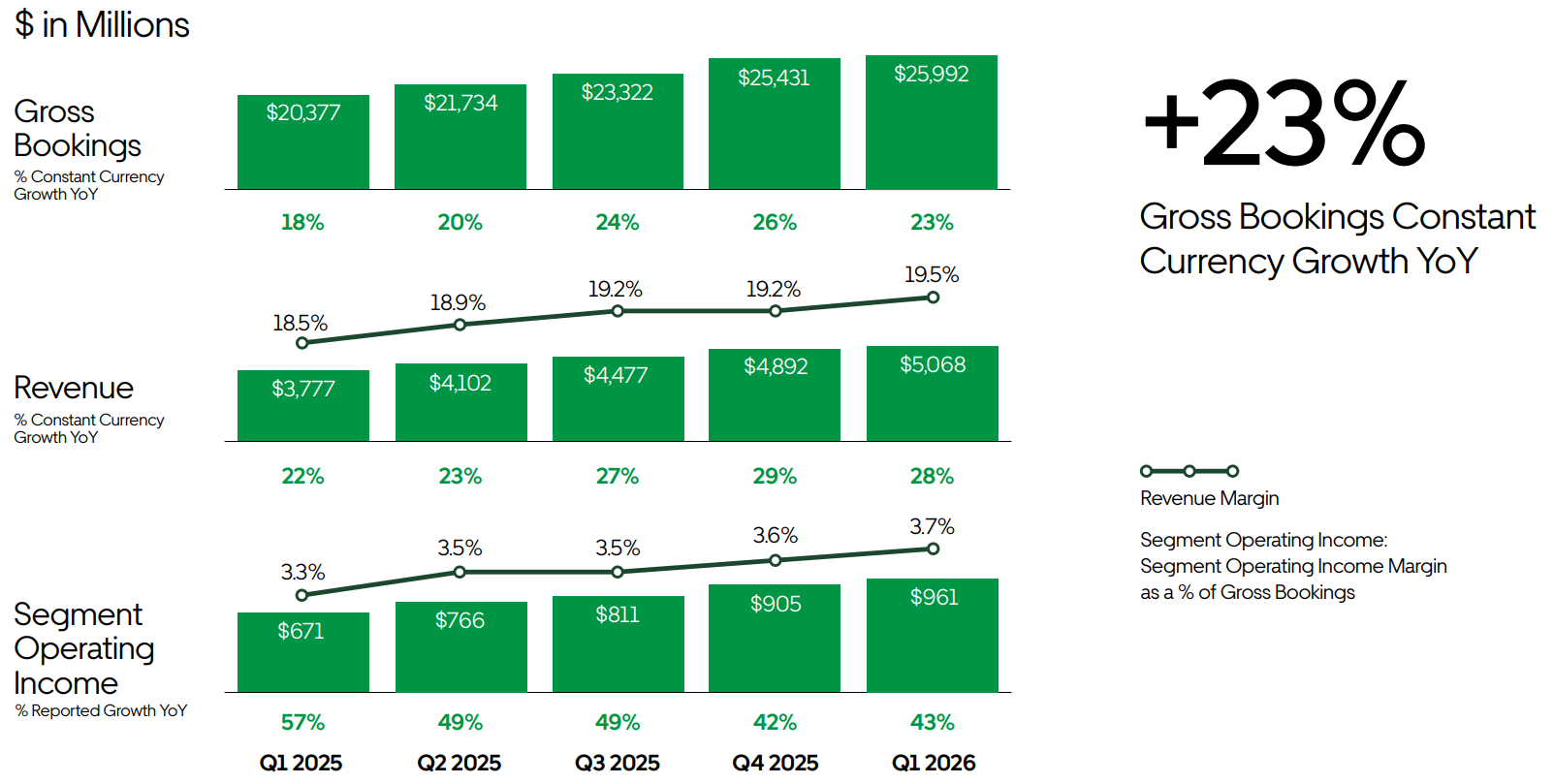

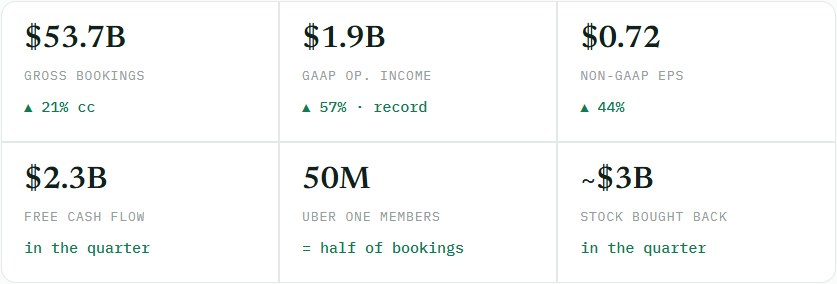

It grew its bookings 21%. It posted record operating profit. It generated $2.3 billion in free cash flow. It bought back roughly $3 billion of its own stock. It crossed 50 million paying members in a loyalty program that now drives half of everything it sells.

Now imagine that same stock is trading near its lowest point in a year, while Wall Street secretly stamps it with a Strong Buy and price targets that sit 45% to over 100% above where it trades today.

That is not a hypothetical. That is a real company, reporting real numbers right now, and the market has decided to price it like a melting ice cube because of one fear that I believe is wildly overblown.

I just started a position. I am in for $4,000 today, and I plan to build it up toward $10,000 as more capital comes in, adding on weakness. This is not one of my weekly income funds. It is a growth-at-a-discount play funded with the cash flow my dividend portfolio throws off, the dividend wheel in action.

I am going to name the stock and show you exactly why the market is wrong. Then, for paid members, I break down the partnership that ties this to a second stock I hold, the full numbers, Wall Street’s targets, my own price target, and how I am building the position. Let’s get into it.

👉 My two buy alerts from the beginning of June are now up more than 25%.

The Setup: A Leader Priced Like a Loser

Here is the mechanism behind the mispricing, because once you see it you cannot unsee it.

The entire market has fixated on a single story: that a new wave of technology is about to make this company obsolete. The narrative is so loud that it has completely drowned out the fundamentals. And the fundamentals are not just fine. They are accelerating.

This company runs a platform that almost everyone reading this has used. It operates in more than 70 countries. It has two enormous business engines, and the one investors ignore is actually growing faster and is almost completely immune to the very disruption everyone is panicking about.

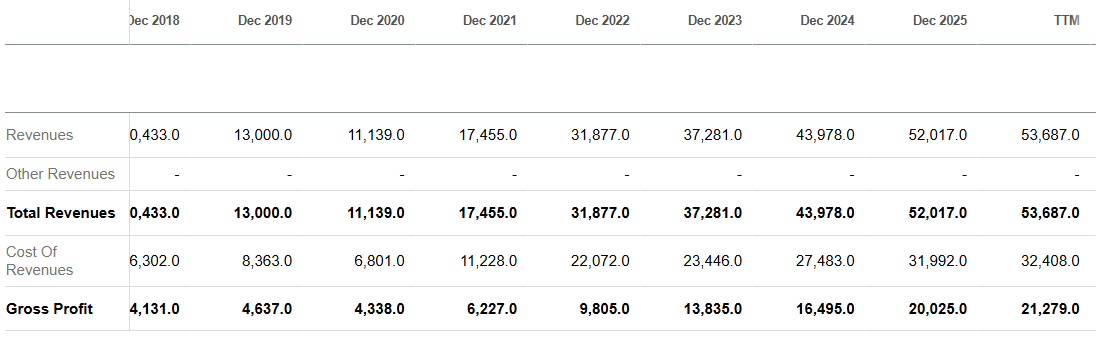

The bear case says the core business gets eaten alive by automation over the next several years. The filings say bookings are compounding north of 20%, profit is scaling at more than twice the rate of revenue, and the company is so flush with cash it is aggressively buying back its own shares at these depressed prices.

So you have a profitable, cash-generating, share-shrinking market leader being valued as if its best days are behind it. That gap between perception and reality is exactly where the biggest returns come from.

And here is the part almost nobody is pricing in. This company is not fighting the technology that supposedly threatens it. It is positioning to become the toll road that every version of that technology has to drive through. Let me name it and show you.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor.

Uber Technologies (UBER)

The company is Uber Technologies UBER 0.00%↑, and as I write this it is trading in the low $70s, near its 52-week low, down on the year while the broader market is up.

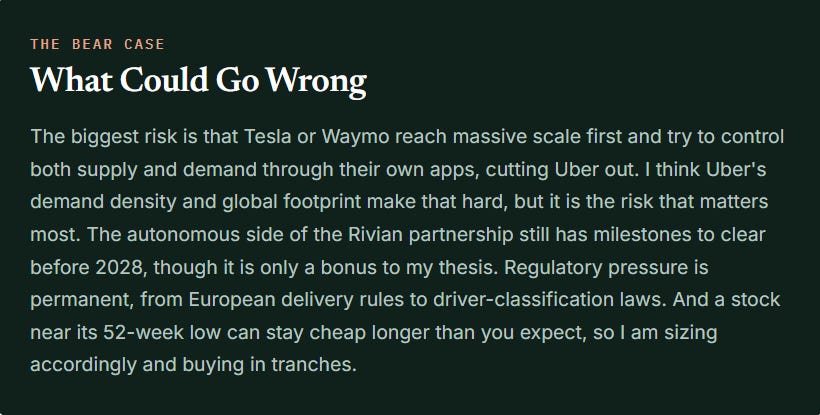

The reason is simple and, in my view, wrong. The market has decided that self-driving cars from the likes of Waymo and Tesla will make Uber irrelevant. The logic goes that once robotaxis scale, nobody needs Uber’s network of drivers, so the business gets disrupted into the ground.

I see it the opposite way. Uber does not need to build the winning robotaxi. It needs to own the customer. In a world where dozens of companies are racing to build autonomous fleets, the supply of self-driving cars becomes fragmented and commoditized. When supply gets commoditized, the power flows to whoever controls demand. And Uber controls demand at a scale almost no one else on earth can match: 199 million monthly active users and 3.6 billion trips in a single quarter.

Uber has already signed up more than two dozen autonomous partners and plans to facilitate robotaxi trips in as many as 15 cities globally by the end of 2026. Instead of being the victim of the AV era, Uber is setting itself up to be the demand layer that every fragmented fleet plugs into. The robotaxi makers supply the cars. Uber supplies the riders. Guess who keeps the customer relationship.

That alone is the reason this stock should not be sitting near a 52-week low. But it is the next part that made me actually open my wallet, and it ties Uber directly to a second stock I already own.

The Numbers: Firing on All Cylinders

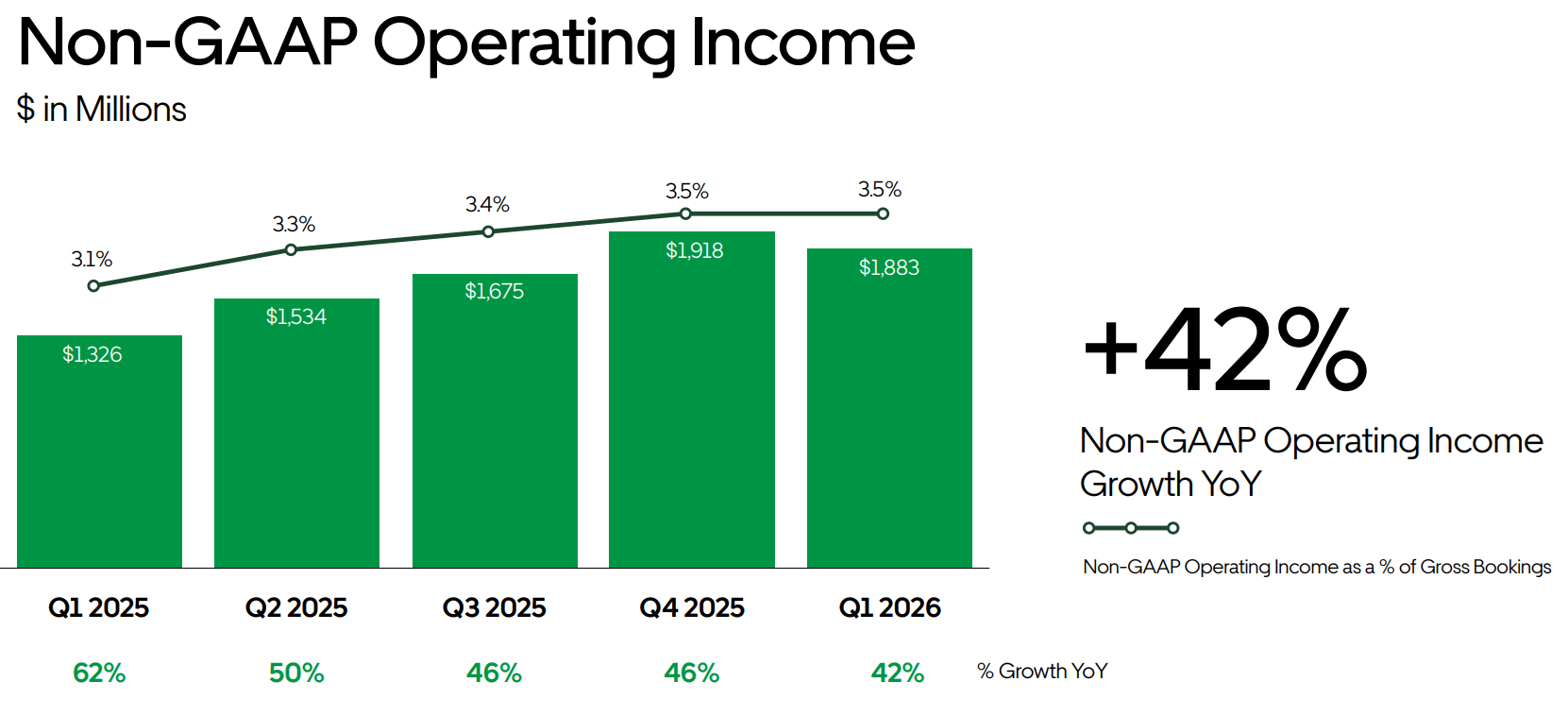

One thing to clear up, because it is the trap scaring people off. Uber’s headline GAAP net income came in at just $263 million, which looks like a collapse versus a year ago. It is not an operating problem. That number absorbed a $1.5 billion non-cash hit from marking down the value of Uber’s equity investments. Strip out that accounting noise and the operating business is the strongest it has ever been. The market is anchoring on a scary headline and missing the machine underneath it.

And remember those two engines. Delivery is now growing faster than ride-hailing, its segment profit jumped 43% in the quarter, and it is almost entirely unaffected by the AV fear. Even in a worst-case world where robotaxis pressure mobility, Uber has a second high-margin engine that keeps compounding. Management guided Q2 bookings to as much as $57.75 billion with EPS up to $0.82, so the momentum is not slowing.

The Upside: Wall Street’s Targets and My Own

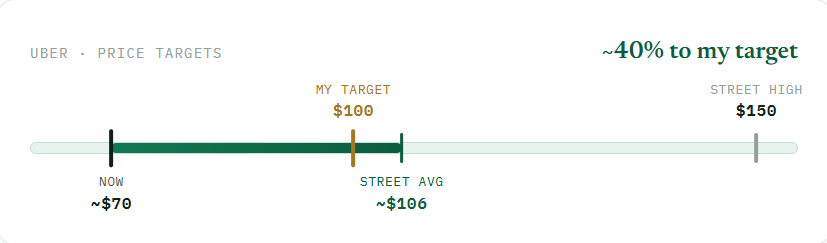

This is where the risk/reward gets loud. Uber carries a consensus Strong Buy, with an average target around $104 to $108, the bulls at $115 (Tigress) and $125 (Guggenheim), a Street high of $150, and even the most bearish target near $75 sitting above today’s price.

Here is my own call: I think Uber is a $100 stock, and I think it gets there within about 12 months.

The catalyst is the one the bears are ignoring. Right now capital is crowded into the AI and memory-chip momentum trade, chasing the same handful of names. That rotation does not last forever. When it cools, money comes looking for profitable, reasonably valued compounders, and Uber is sitting right there near a 52-week low with record operating profit and $2.3 billion of quarterly free cash flow. A move from the low $70s to $100 is roughly 40% upside, and I believe that re-rating happens inside a year as the market remembers this business exists.

A Complementary Kicker: The Rivian Angle

There is one more reason I like this trade, and I want to be clear that it is a bonus, not the basis of my position.

I also own Rivian RIVN 0.00%↑, and the two companies have a robotaxi partnership worth up to $1.25 billion, with Uber set to deploy up to 50,000 autonomous Rivian R2 robotaxis exclusively on its platform. Rivian has now started producing the R2 and first deliveries are rolling out, so this is no longer a paper concept. The autonomous version still has milestones to clear before those robotaxis hit the road around 2028, which is why I treat the deal as long-dated optionality rather than a near-term driver.

But it is a nice kicker. If it plays out, the same trend pays both of the positions I already hold, and my Uber thesis stands completely on its own without it. The cheap, profitable, cash-gushing core business is the reason I bought. Rivian is just a bonus I get for free.

How I Am Playing It

Started with $4,000, building toward $10,000 as more capital comes in, adding on weakness near these 52-week lows.

The cheap, profitable, cash-generating core business is the reason to own it today.

Anchor on the $100 target over 12 months, and let the buybacks and free cash flow pay me to wait if it takes longer.

Treat the robotaxi optionality, including the complementary Rivian angle, as upside I am barely paying for.

This is a different kind of position than my weekly income funds, and that is the point. I use the income those funds generate to accumulate high-conviction names like this one when the market hands them to me at a discount.

Bottom Line

The market is paying me to buy a dominant, profitable, cash-gushing platform at a discount because it is afraid of a disruption that Uber is positioning to profit from. Wall Street sees 45% to 100% upside. I see a $100 stock within 12 months, with a Rivian kicker that pays my other position too.

I am a buyer. $4,000 to start, building toward $10,000 on weakness.