I Put $12,000 Into Two Stocks Last Month. Here’s Why.

Two contrarian bets I'm making right now, and exactly why I made them

Most people wait until a trade is obvious before they make it. By then, the easy money is already gone.

The two positions I’m breaking down today are not obvious. I haven’t seen anyone else provide in-depth analysis on them.

One has a reputation it hasn’t fully shaken. The other is still burning cash at a rate that makes conservative investors flinch. Neither of them would show up on a screener looking for clean, safe, low-risk compounders.

I bought them because I think the market is still pricing both of these companies for what they used to be, not for what they are becoming. And in my experience, that gap between perception and reality is exactly where the real money gets made.

I put $8,000 into the first position and $4,000 into the second. I sized them differently because the risk profiles are different. But I have genuine conviction in both.

Before I get into the thesis, I want to set some context. If you’ve read my work on the AI transition and the four stages of where value accumulates in a technology shift, the mental framework I’m using here will feel familiar. If you haven’t, I’d recommend starting there first.

The rest of this article is for paid Dividendomics subscribers. If you want the full thesis, the bull and bear cases, and exactly how I’m thinking about sizing and time horizon on both positions, join below.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor

Position One: Robinhood Markets (HOOD)

Why I Bought

I came into Robinhood HOOD 0.00%↑ with a fair amount of skepticism. For a long time, the story felt thin. A meme stock app with a checkered regulatory history, a gambling-adjacent reputation, and a business model that critics had spent years trying to dismantle.

When I started paying closer attention to the numbers and the product roadmap, I stopped seeing a meme stock app. I started seeing a financial platform in the middle of a genuine transformation, one where the market hasn’t caught up to the reality of what this business is becoming.

That’s when I decided to get in.

The Bull Case

The most important thing to understand about Robinhood right now is that the revenue story has fundamentally changed. For years, the company was almost entirely dependent on Payment for Order Flow, a single revenue stream that critics correctly identified as fragile and regulatory-vulnerable. That’s not the business anymore.

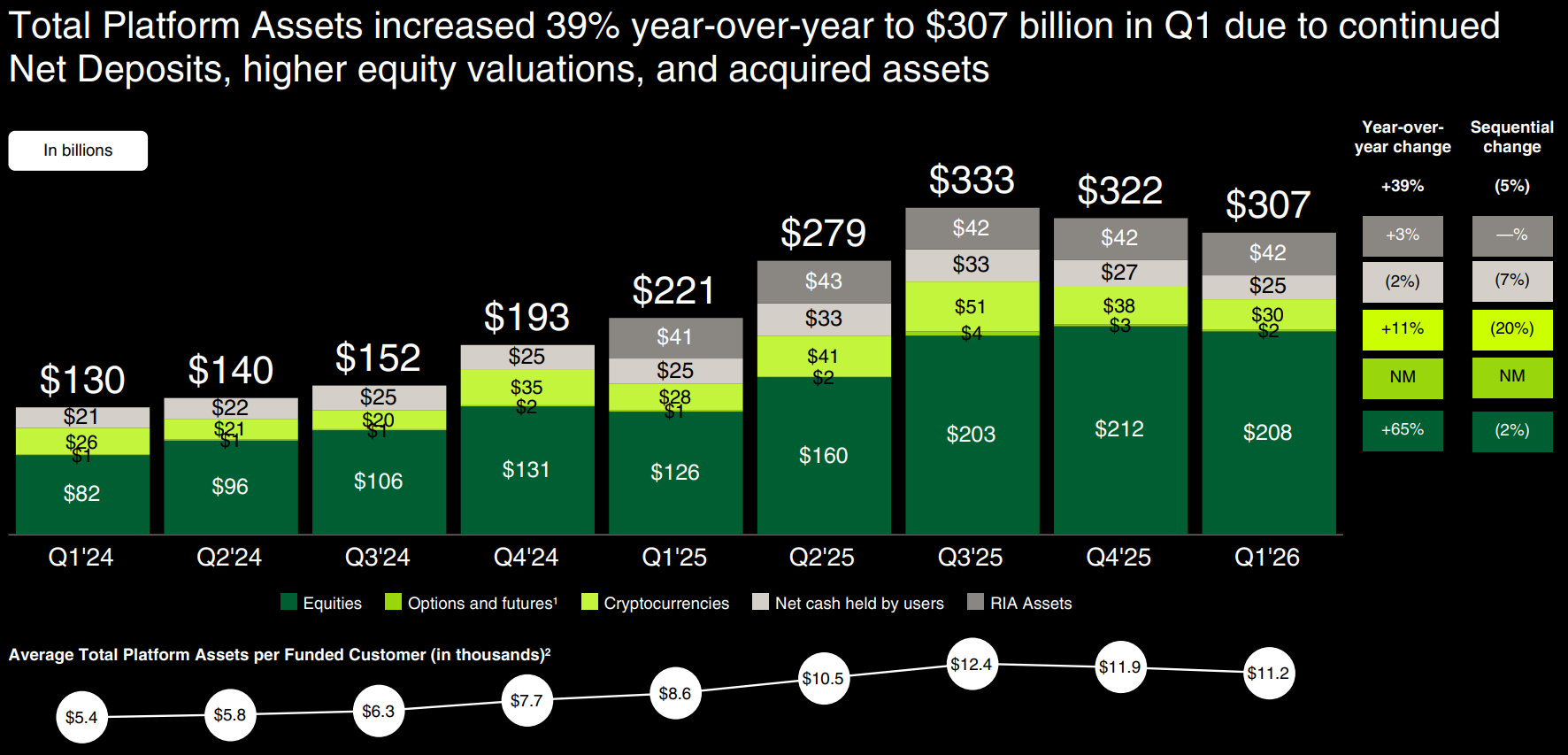

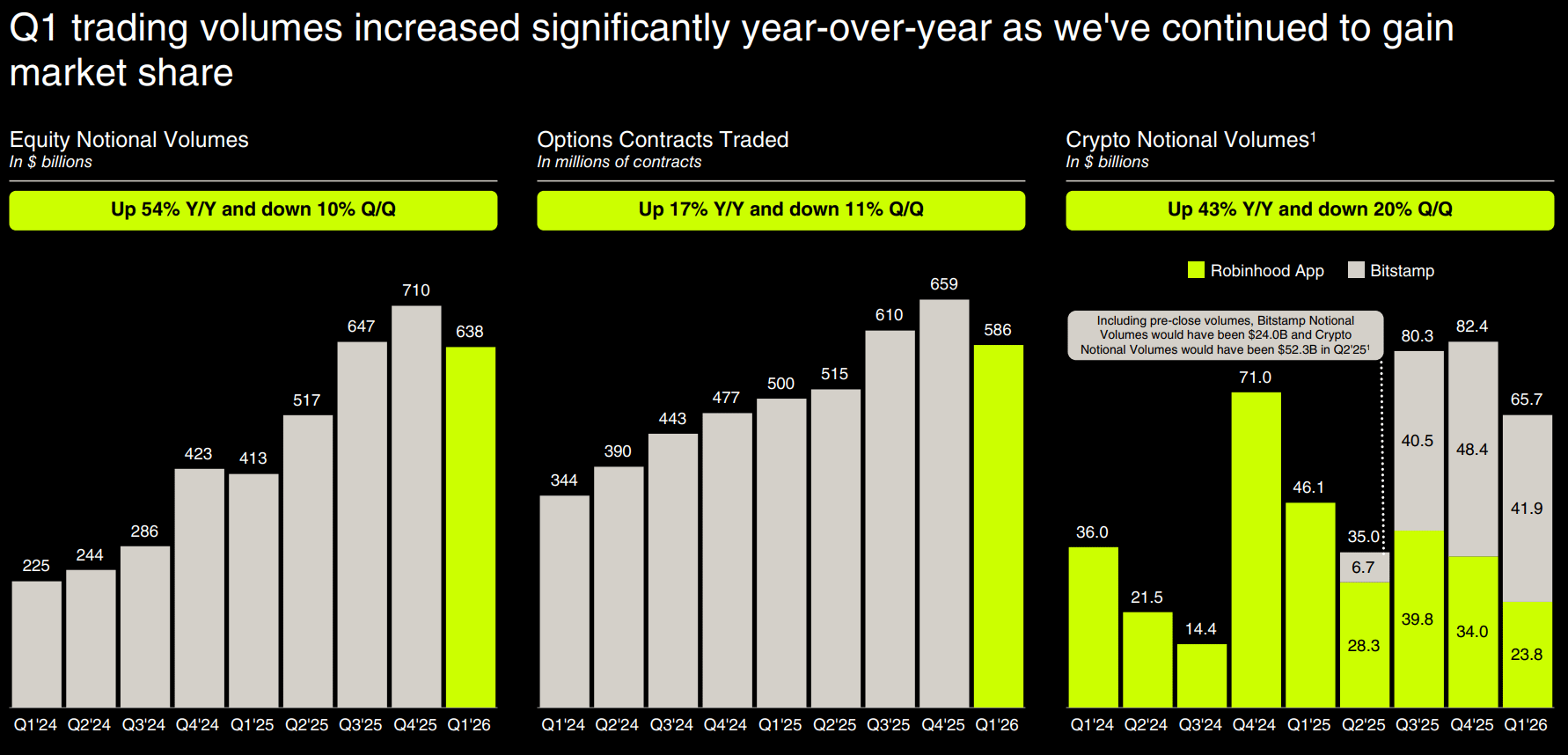

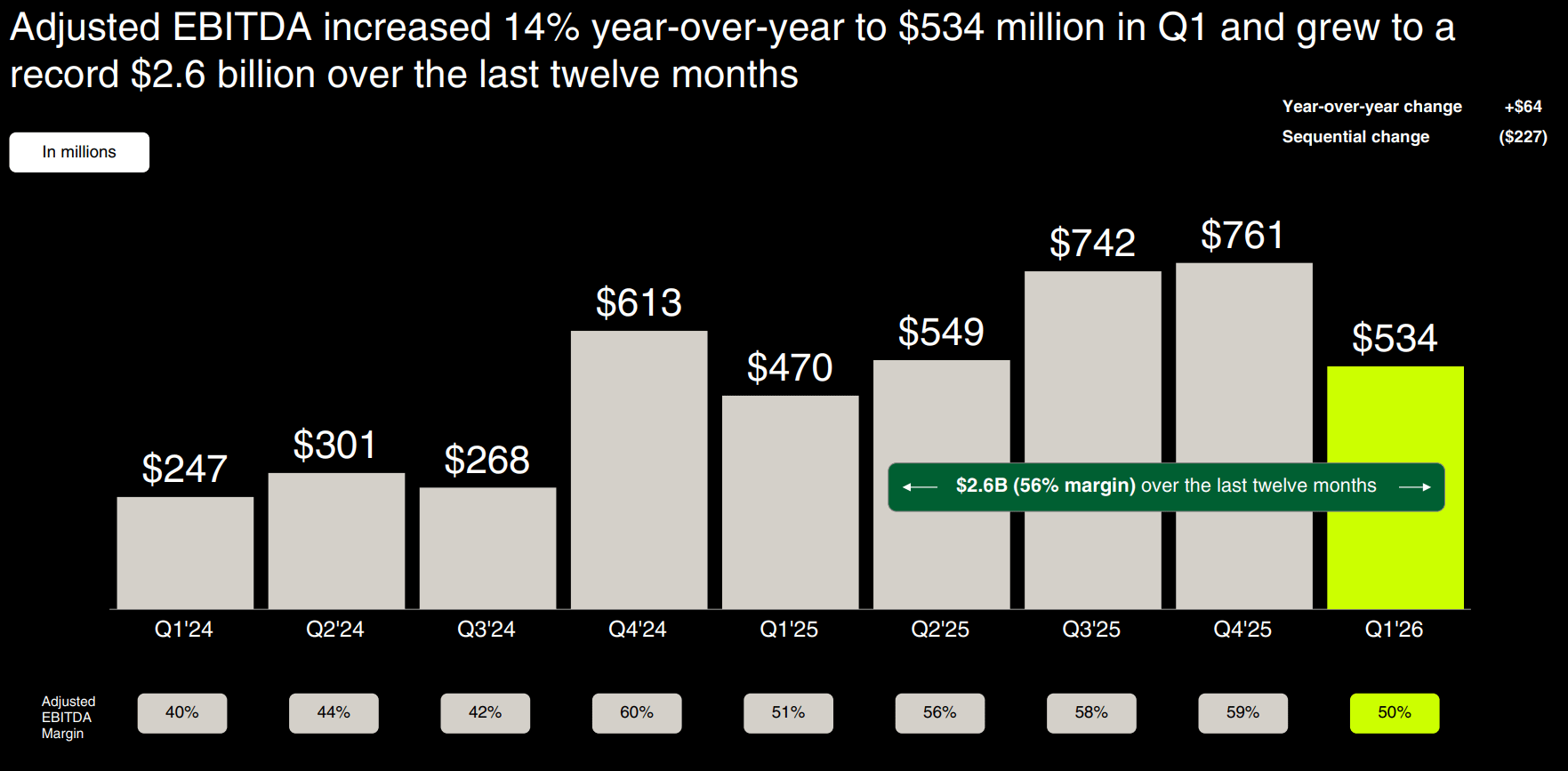

2025 was a year that made the pivot undeniable. Full-year revenues came in at $4.5 billion, a record, with diluted EPS of $2.05, also a record. Revenue doubled year-over-year in Q3 alone. Net deposits hit $68 billion for the year. These are not meme-stock trading numbers. These are the numbers of a business that has found real, durable traction across multiple product lines.

What’s driving it? Four distinct revenue pillars that have replaced the single-point-of-failure model:

Transaction-based revenue across equities, options, and crypto

Net interest income that has grown substantially as the cash management business scaled

Robinhood Gold subscriptions sitting at 4.2 million subscribers by early 2026, up 76% year-over-year

Growing financial services layer that includes credit cards and international products.

The Gold Credit Card alone deserves attention. Offering 3% cash back across all categories, it hit 600,000 users by end of 2025. That is a financial product with genuine stickiness that is pulling users deeper into the Robinhood ecosystem and away from legacy institutions.

That is the broader strategic play here, what management calls the Financial SuperApp. The vision is a single platform where a customer handles their investing, trading, spending, saving, and banking needs all in one place. The bet is that Robinhood’s mobile-first, high-yield, low-friction environment wins the loyalty of younger generations, particularly the Gen Z and Millennial cohorts who are set to inherit an estimated $84 trillion in wealth over the next decade.

The 3% IRA match, for example, pulled over $26 billion in retirement assets away from legacy institutions in 2025 alone. Legacy firms have not meaningfully responded because they can’t. Their cost structures and institutional cultures make it nearly impossible to compete on those terms.

Internationally, Robinhood is pushing hard too. UK ISAs launched in early 2026. Crypto perpetual futures went live in Europe. The acquisition of Bitstamp gave the company genuine global crypto infrastructure. Management has announced Asia-Pacific expansion plans through acquisitions in Indonesia, signaling that the addressable market thinking here is not limited to the United States.

The company is also buying back stock aggressively, $173 million in early 2026 alone, with a $1.5 billion total repurchase authorization. When management buys back that much of their own stock, they are telling you something. I believe them.

The Bear Case

I don’t want to gloss over the risks, because they’re real.

The most significant one is that a meaningful portion of Robinhood’s revenue still depends on trading volumes, and trading volumes are highly sensitive to market conditions. When volatility subsides and retail interest cools, this shows up fast. Q4 2025 crypto revenue dropped 18% sequentially in a softer market environment. That is the kind of number that reminds you the business still has cyclical exposure.

Regulatory risk is perennial. Robinhood’s history with regulators is not clean, and the PFOF debate hasn’t fully resolved. An unfavorable regulatory shift could still impair the transaction revenue model in ways that are difficult to model in advance.

And then there is competition. The legacy brokerages are not standing still. Charles Schwab and Fidelity still manage trillions in assets and are building modern platforms. Robinhood wins the incremental deposit battle today, but staying ahead requires continuous product execution with no meaningful stumbles.

My Take

I put $8,000 into Robinhood because I think the market is still pricing this like a trading app with a regulatory cloud over its head. The reality is a diversified financial platform with multiple high-growth product lines, a clear strategic vision, aggressive management conviction expressed through buybacks, and a demographic tailwind that is just beginning to play out.

The valuation will only make sense in hindsight, once the SuperApp narrative becomes impossible to ignore. I would rather own it now, while the skeptics are still loud.

Position Two: Rivian (RIVN)

Why I Bought

Rivian RIVN 0.00%↑ is a harder story to tell, and I want to be honest about that upfront. This is not a company that is printing money. Net losses are still enormous. Cash burn is real. The path to profitability runs through a vehicle launch that hasn’t fully happened yet and a scale-up that requires things to go right.

And yet. I bought 300 shares at roughly $13 a piece.

Here is why: there are certain moments in the lifecycle of a capital-intensive business where everything that came before is essentially table-stakes losses, the cost of earning the right to play at scale. I think Rivian is at the inflection point right before that game actually starts.

The R2 is the catalyst. And the data we have on where this business stands going into that launch is, frankly, more encouraging than I expected when I started digging.

The Bull Case

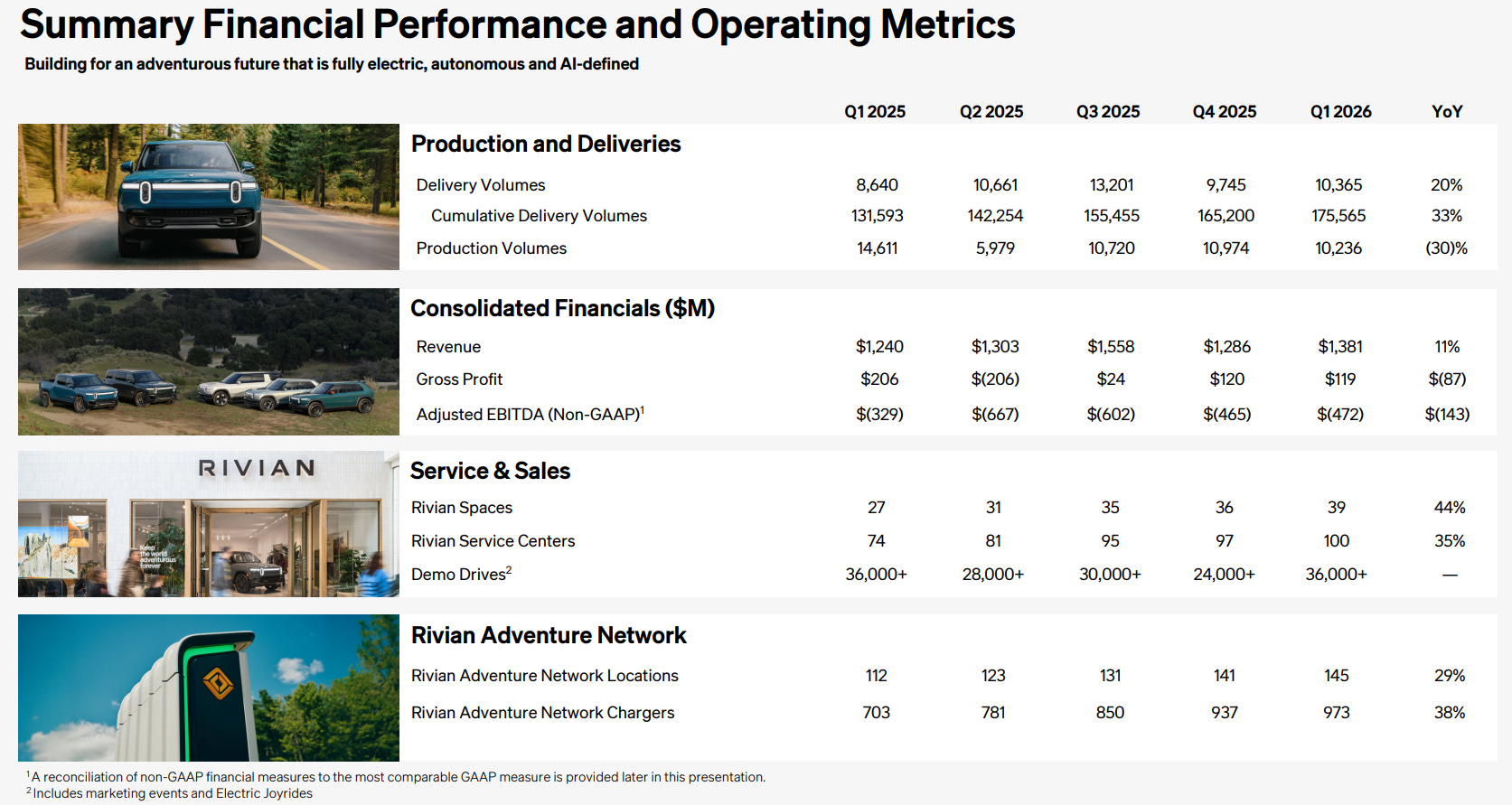

Start with what has already happened. Rivian achieved its first full year of consolidated gross profit in 2025, $144 million. That sounds modest against the backdrop of $3.6 billion in net losses, but in the EV startup world, crossing the gross profit threshold is a structural milestone. It means the vehicles are no longer being sold at an operating loss at the unit level. The underlying economics of the manufacturing business are beginning to work.

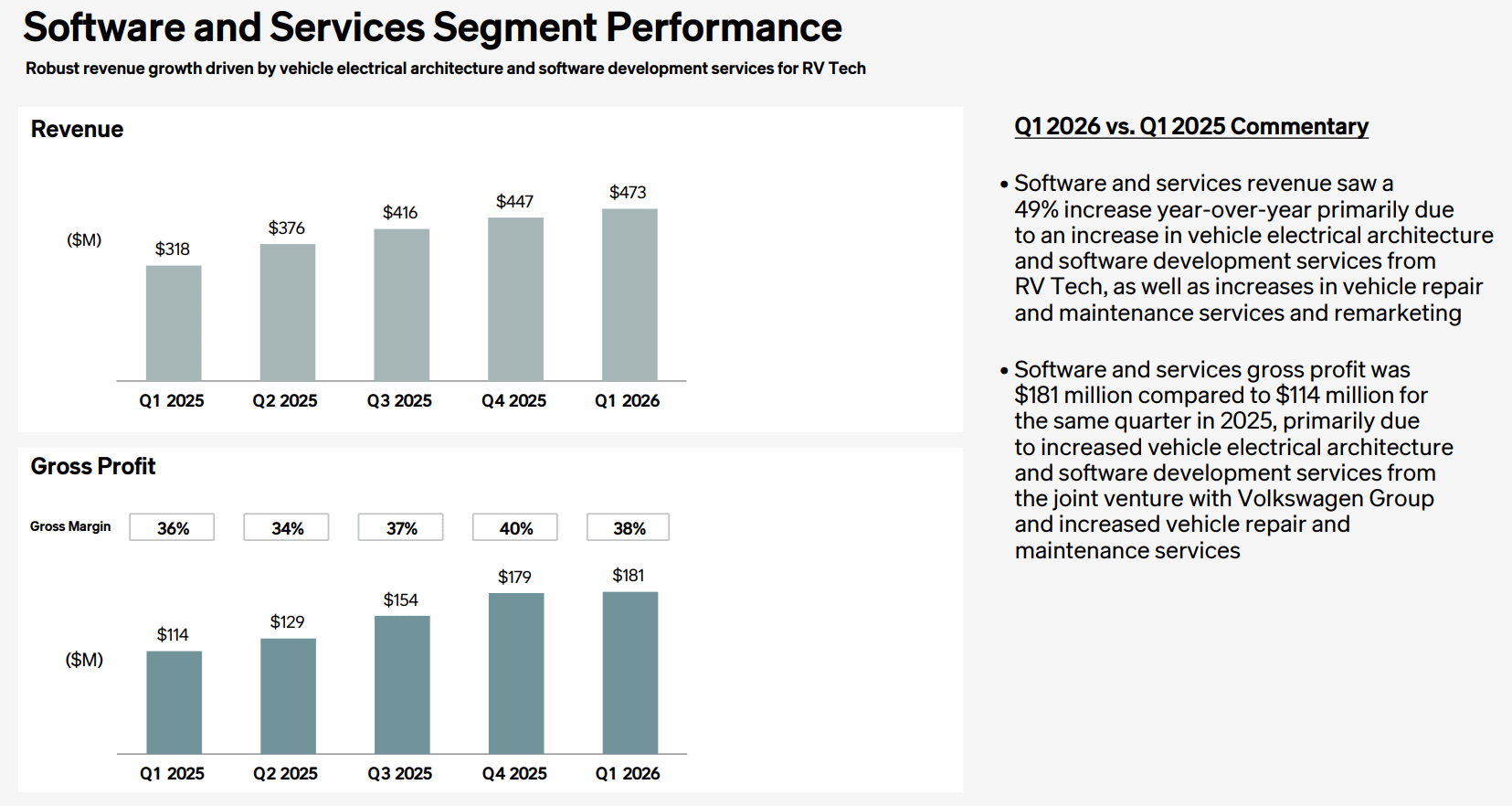

The software and services segment deserves specific attention. That business went from $7 million in gross profit to $576 million in a single year, driven by the Volkswagen joint venture and growing services revenues. This is the emergence of a high-margin, recurring revenue layer sitting on top of the vehicle business. If it continues to scale, it changes the entire financial profile of the company over the medium term.

The Volkswagen partnership is a genuine strategic asset, not a press release. VW committed roughly $5.8 billion to the joint venture, with funding tranches tied to Rivian hitting specific financial milestones, meaning Rivian has already earned real capital by executing. VW’s supply chain expertise, global distribution relationships, and manufacturing knowledge represent resources that Rivian couldn’t build independently in any reasonable timeframe. When a large incumbent writes a check of that size, it is telling you something about what they believe lives inside this company’s technology stack.

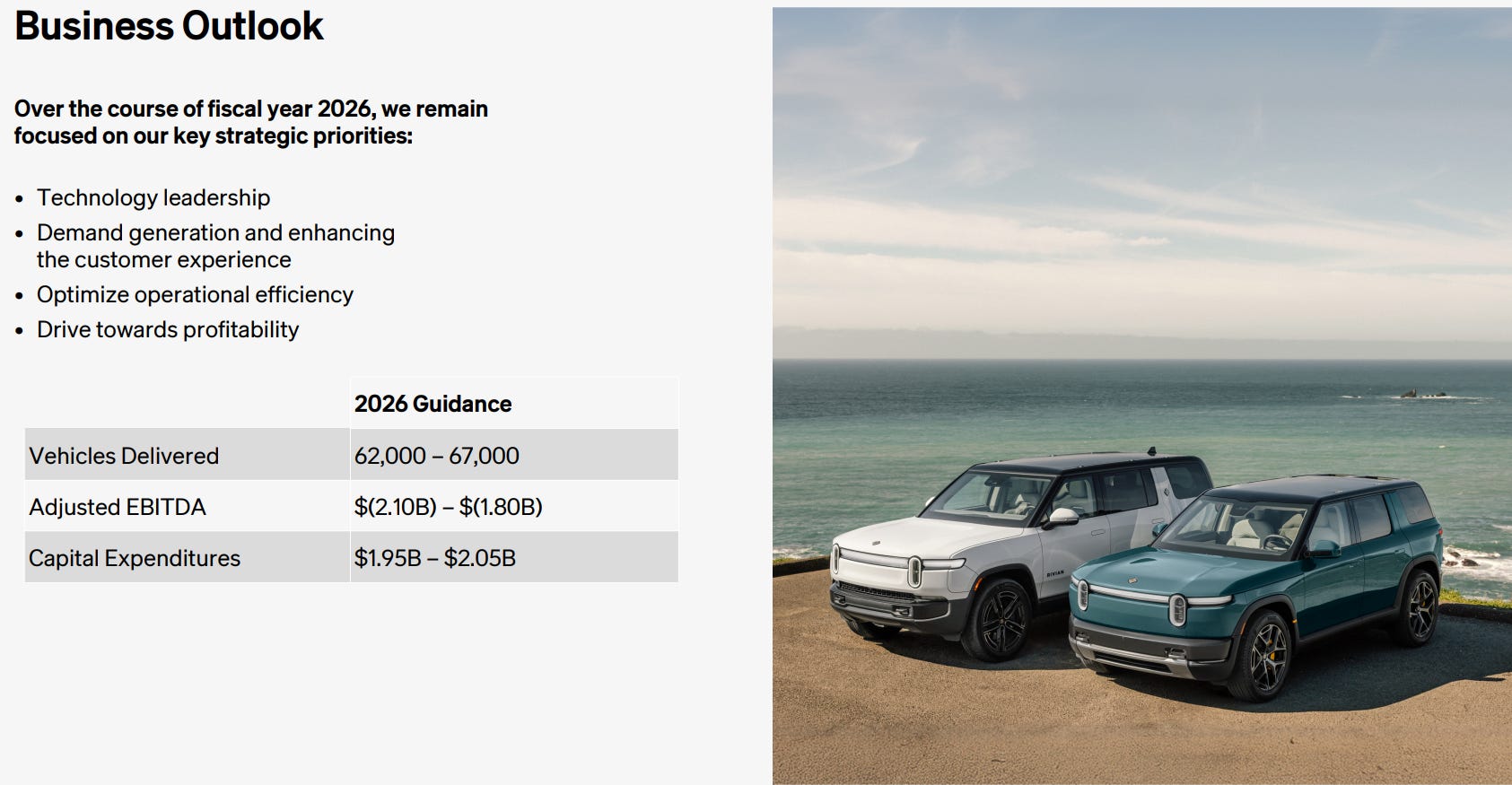

The R2 is the demand catalyst that everything else depends on. Priced around $45,000, it targets the mass-market compact SUV segment, a far more addressable market than the $70,000+ R1T and R1S trucks that have defined Rivian until now. Deliveries are expected to begin in Q2 2026, and early pre-production reviews have been notably strong. The bill-of-materials cost is projected at roughly $32,000, a meaningful improvement over current models driven by simplified design and shared components.

The factory picture supports the scale story in physical form. Rivian’s Normal, Illinois plant has been upgraded to 215,000 units of capacity. The planned Georgia facility, backed by a $4.5 billion government loan, is expected to add approximately 400,000 units of capacity in phases, with first vehicles targeted by end of 2028. That is the infrastructure of a real automaker, not a startup.

On the technology side, the December 2025 Autonomy and AI Day revealed the RAP-1 Autonomy Processor, an in-house chip program, alongside an autonomous driving platform and an AI-driven in-car assistant. The company also spun out Mind Robotics, an AI-enabled industrial robotics venture. The technology being built for these vehicles has applications that extend well beyond transportation.

Macro tailwinds are building quietly too. California’s Clean Fuel Reward program through 2030 supports commercial EV demand. Proposed USMCA changes that favor U.S.-content EVs with domestic manufacturing footprints put Rivian in a structurally better position than imported competitors. Rivian builds in America. That matters more today than it did eighteen months ago.

The Bear Case

The bear case on Rivian is simple to state and genuinely serious: cash burn is enormous, the R2 has to execute, and if it doesn’t, the losses compound in a way that eventually forces a dilutive capital raise.

Free cash flow was negative $2.5 billion in 2025. Adjusted EBITDA guidance for 2026 is still a loss of $1.8 to $2.1 billion. Capital expenditures for 2026 are nearly $2 billion. Rivian ended 2025 with $6.1 billion in cash and short-term investments. The run rate makes clear this company needs the R2 to generate real revenue at real volumes, and it needs to happen without major production hiccups.

Analysts have already flagged that R2 initial pricing came in higher than originally signaled, and volume targets are aggressive for a company that has never manufactured at mass-market scale. A production stumble or a demand miss could significantly delay the path to positive EBITDA.

The Volkswagen joint venture has also reportedly hit software coordination turbulence, with some internal timelines at VW shifting. How that ripples into Rivian’s technology roadmap and cash disbursements is worth watching closely.

And competition is not static. Tesla’s Model Y still dominates the segment Rivian is targeting. Ford and Hyundai have competitive products at similar price points. Rivian’s brand is powerful within its outdoor adventure niche, but expanding into mass-market territory is a genuine product and marketing challenge, not just an engineering one.

My Take

I bought 300 shares because I believe the R2 launch is one of those inflection moments that, if it goes right, makes everything that came before it look like a compelling entry point. The gross profit milestone, the software revenue ramp, the Volkswagen backing, the technology roadmap. All of it points to a company that is further along than the stock price reflects.

This is a patient capital position. I am not expecting a straight line. I’m expecting volatility, skeptics, and at least one quarter that rattles me. But I think the risk-reward is right at these prices for an investor with a two to three year time horizon.

Closing Thoughts

These two positions have almost nothing in common at the surface level. One is a fintech platform. The other is an EV manufacturer. But underneath, they share the same structure: businesses at inflection points, priced for their histories rather than their futures, where the patient investor has a real edge over the market’s shorter time horizon.

I’ve been wrong on stocks before. I will be wrong again. But when I look at the evidence on both of these, I feel more conviction than discomfort.

That’s usually a good sign.

This is not financial advice. These are my personal positions and my personal analysis. Do your own research, know your risk tolerance, and size accordingly.

Long HOOD, Long RIVN at time of writing.