How To Build A Portfolio That Eventually Produces $5K A Month

A step-by-step framework for turning capital gains into consistent monthly cash flow.

Most people spend their entire lives trading their most precious resource, time, for a paycheck. They wake up, commute, and work to build someone else’s dream, only to repeat the cycle the very next day. This is the “linear trap.” In a linear life, if you stop working, the money stops flowing. The problem usually isn’t a lack of hard work; it is a lack of leverage. If you only earn money when you are physically present, you have a hard ceiling on your freedom.

The world’s wealthiest individuals do not rely on linear effort. They build systems where one unit of input produces exponential output.

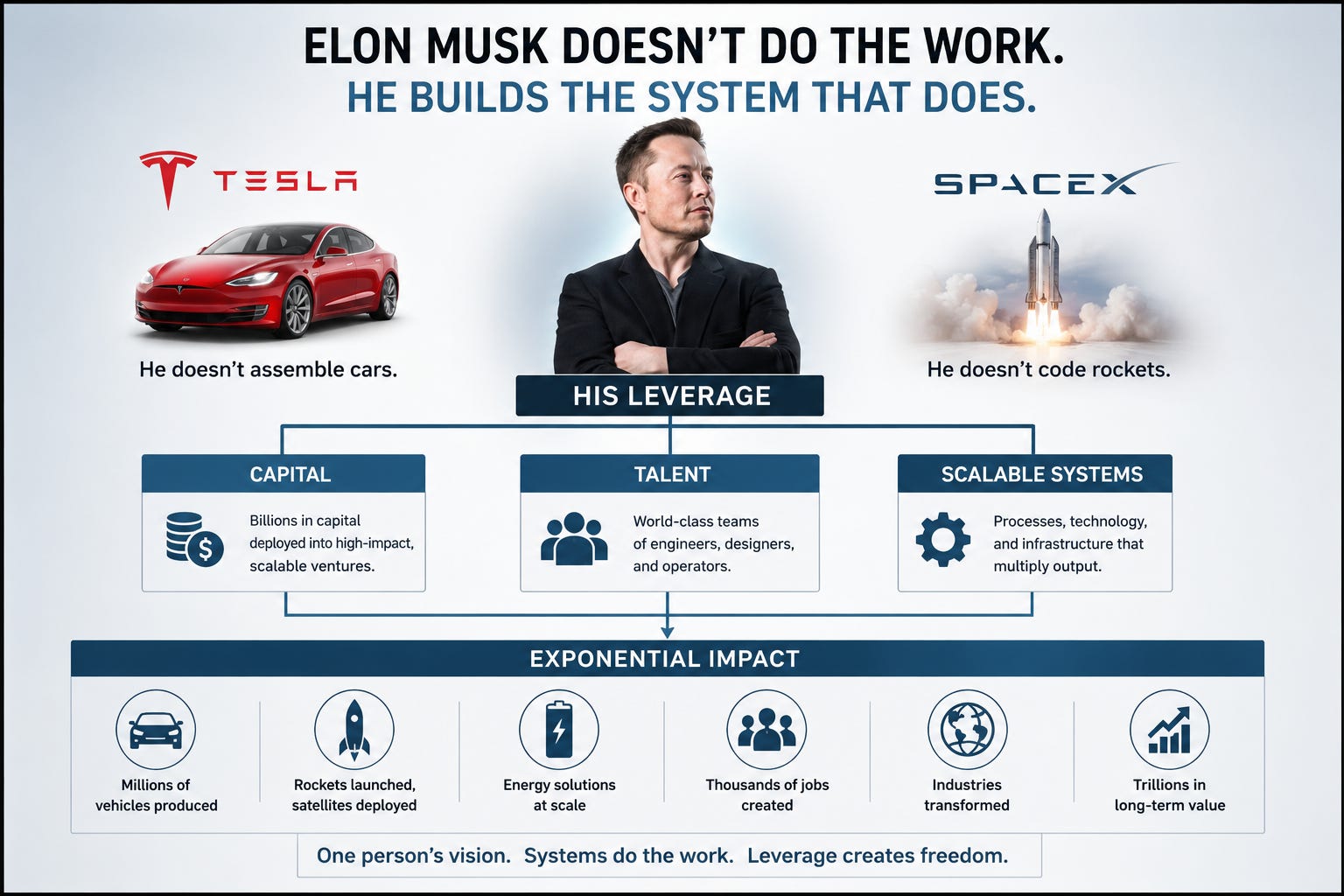

Take Elon Musk. He is not assembling cars at Tesla or coding at SpaceX. His leverage comes from capital, talent, and scalable systems. He scales those business and it creates wealth for shareholders. More creates more.

This concept is a lot easier to apply to the ultra rich. However, it’s also a universal truth for all of us.

Leverage generally falls into four categories:

Capital

Labor

Technology

Existing Assets.

The key shift is moving from doing more work to owning systems. When you own assets such as stocks, businesses, or intellectual property, your income is no longer tied to your time.

In this article, I want to highlight the actual blueprint that you can follow to get rich and accumulate wealth. I will breakdown how much money you need and how to position yourself to fire your job. I will also share the exact portfolio allocation that has been back tested to provide superior results.

More Creates More

It is undeniably difficult to get rich, but it is remarkably easy to stay rich. This is because having a lot of money allows you to easily create more with a lot less risk.

Want to create $100,000 from $0? It requires massive effort, time, and risks.

Want to create $100,000 from $500,000? It simply requires a 20% return with little risk or involvement. The S&P 500 is up more than 26% over the last year.

Think of your financial journey like trying to move a massive, heavy boulder at the top of a hill. To get it to move even a single inch, you have to lean into it with every ounce of strength you have. You sweat, your muscles ache, and for a long time, it feels like nothing is happening.

But a strange thing happens once that boulder starts to roll.

Once it gains momentum, gravity begins to do the work for you. Soon, the boulder is moving faster than you could ever push it. Eventually, it picks up so much speed that it becomes an unstoppable force of nature.

I’ve started to see this take place in my own life. Because I’ve grown my pool of invested assets, my wealth compounds at a rate faster than what I can personally contribute.

Building Your First $100k

This is the hardest part of the blueprint. Depending on your age, family obligations, career, and income, this part of the journey is the longest.

If the goal is to reach $5,000 a month in dividends, you have to accept a hard truth: The first $100,000 is hard. At this stage, your investment returns are irrelevant. If you have $5,000 invested and the market has a “great” year and goes up 10%, you made $500. That’s not going to change your life. At this phase, your savings rate is your only real engine.

To build an engine capable of reaching escape velocity, you need to focus on three things:

Focus On High-Income Skills

Aggressive Debt Elimination

Invest Your Money - Here’s a guide to start investing

The “More Creates More” effect is barely visible here. It’s 90% your sweat and 10% the market. But once you hit that six-figure milestone, the physics start to shift in your favor.

You Need Growth Positions First

This is where most income investors get it wrong.

They try to jump straight into high-yield assets too early. It feels good to collect dividends, but if your capital base is small, you are effectively locking yourself into slow growth.

Before your portfolio can produce meaningful income, it needs to expand in size, and the fastest way to do that is through capital appreciation. This is where growth positions play a critical role. Companies like NVIDIA NVDA 0.00%↑, Meta Platforms META 0.00%↑, or Amazon AMZN 0.00%↑ are not built for income today. They are built to compound capital.

As your growth positions appreciate, you create something extremely valuable: optional capital. You now have gains that can be harvested and redeployed into income-producing assets.

This is the transition point.

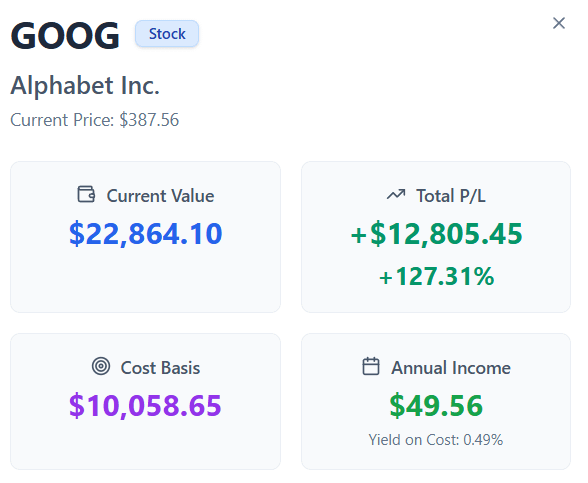

For instance, I invested $10,000 into Google GOOG 0.00%↑ last year. The position has now grown to a value of $22,864. Instead of relying purely on new contributions, your portfolio begins to fund itself.

👉 Here are my 5 top growth stocks for 2026 and beyond.

I can take profits from positions that have significantly appreciated and rotate that capital into income funds that generate immediate cash flow. Over time, this creates a powerful cycle:

This is how you bridge the gap between accumulation and financial freedom.

Positions that started as growth plays have appreciated far beyond my initial expectations. That appreciation is no longer just “paper gains.” It represents future income. By rotating a portion of those gains into income-producing assets, I am effectively converting growth into cash flow without needing to inject new capital.

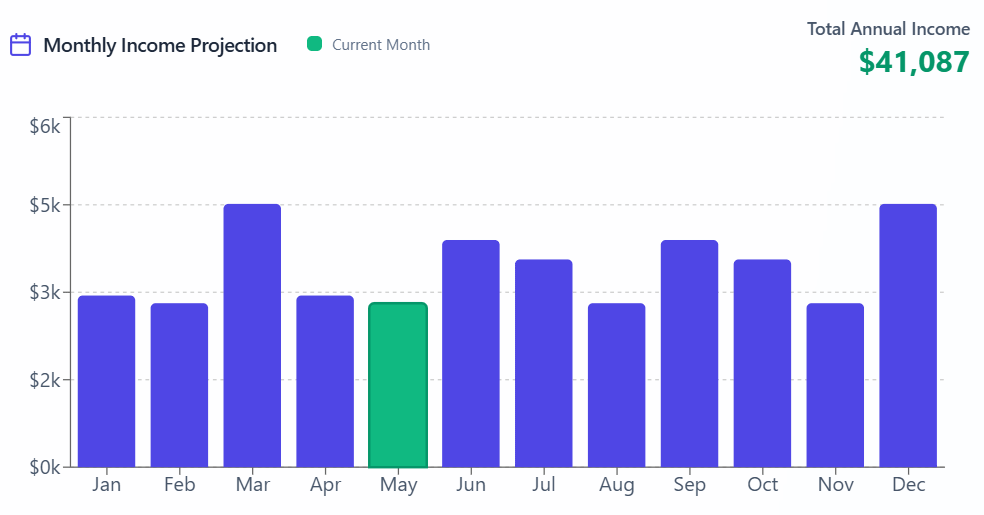

This system is how I was able to rapidly go from $0 → >$41k in annual dividend income in 6 years.

This is the real engine.

You are not choosing between growth and income. You are using growth to manufacture future income at scale.

The mistake is chasing yield too early. The strategy is to build, then convert.

Once you understand this, the entire game changes.

The Math Behind $5,000 Per Month

At some point, the philosophy has to meet reality.

If your goal is to generate $5,000 per month in dividend income, you are targeting:

$60,000 per year in cash flow

There is no way around this number.

The only question is how much capital you need to produce it.

4% yield → $1.5 million

6% yield → $1.0 million

8% yield → $750,000

10% yield → $600,000

20% yield → $300,000

This is where most people have a wake-up moment.

Financial freedom is not about finding a magic stock. It is about accumulating enough income-producing assets to replace your expenses.

And this is also where strategy matters.

A lower-yield portfolio requires more capital, but is typically more stable. A higher-yield portfolio requires less capital, but introduces more complexity and risk.

👉 4 of the best high yield ETFs for passive income.

There is no perfect answer. There is only the approach that fits your goals and risk tolerance. But here is the key insight:

Your timeline is determined by two variables

Your savings rate

Your portfolio return

🔒 The $5,000/Month Dividend Blueprint

So how do you actually build a portfolio that generates $5,000 per month without destroying itself?

This is where most investors go wrong. They assume the answer is simply finding the highest-yielding assets and scaling them up. That approach almost always fails.

The real answer is this structure.

A successful income portfolio is not a collection of random high-yield positions. It is a layered system, where each part of the portfolio serves a specific role. Some assets are designed to protect your capital. Others are built to generate income today. And a smaller portion exists purely to grow your future income.

When these pieces are combined correctly, they create something much more powerful than any single investment. They create an engine that can generate income, adapt over time, and continue growing without constant intervention.

Think of it like building a business.

You would not rely on a single customer or revenue stream. You would want stability, cash flow, and growth working together. Your portfolio should function the same way.

In the next section, I will break down exactly how to structure this system, including the specific allocation ranges and the role each layer plays in getting you to $5,000 per month.

The Portfolio Structure I Would Follow

If your goal is to reach $5,000 per month in income, the fastest way to get there is not by maximizing yield early. That’s the mistake I see many investors make. You reach this monthly income goal by maximizing the size of your portfolio.

That means your allocation should still be built around growth first, with income layered in as a secondary component.

A realistic structure looks like this:

~60% to 70% Growth Positions

This is the core of the portfolio. These are the assets that actually move the needle. If you need guidance, I put together a free ETF for beginners portal for you to navigate. These aren’t recommendations but the portal serves as a helpful starting point for investors that need to be pointed in the right direction.

These positions are not here to generate income today. They are here to compound capital aggressively. This is what gives you something meaningful to convert into income later. I personally choose to hold a mix of both ETFs and separate growth positions. However, you should do what’s most comfortable for you.

~20% to 30% Core Income Positions

This is where you start introducing real cash flow, but without sacrificing quality.

Think:

You can see a core list of low risk income positions here.

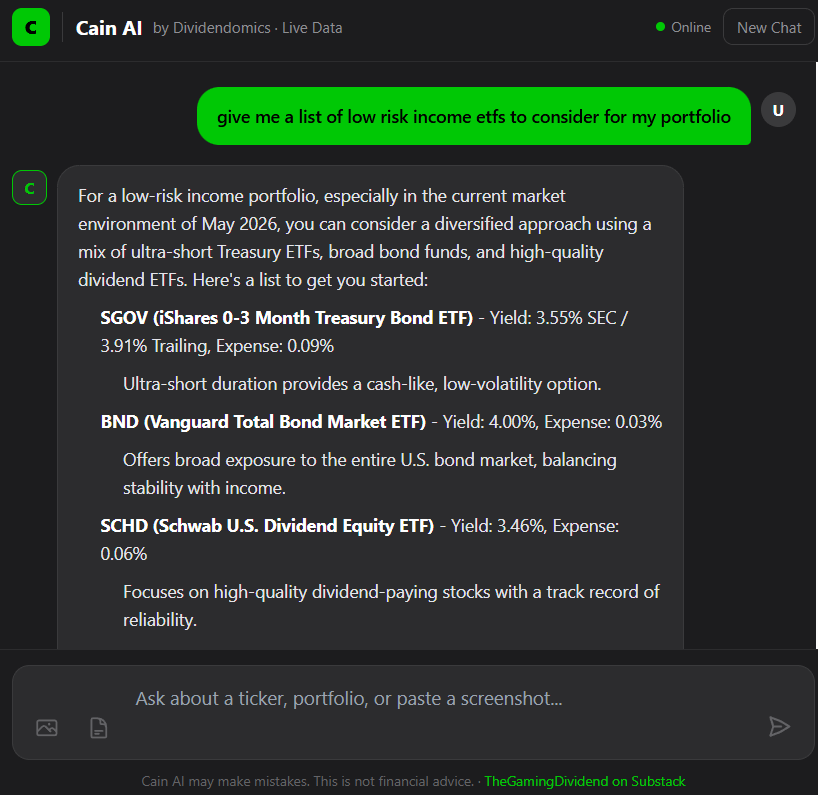

This portion creates a baseline level of income while your growth positions continue to scale. Want guidance, consider using the CainAI tool to help pinpoint what matches your specific risk tolerance.

~10% to 15% High-Yield Strategies

This is the smallest allocation for a reason.

These positions can generate significant income, but they come with trade-offs. Used correctly, they accelerate your income. Overused, they slow your long-term progress.

Think:

This structure keeps your portfolio aligned with the reality you just laid out.

Growth is doing the heavy lifting. Income is being layered in strategically.

You are not trying to live off your portfolio yet. You are trying to build it to a point where living off it becomes inevitable.

That is the difference.

Converting Growth Into Income

This is where everything changes.

Up to this point, the focus has been on building the portfolio. But there comes a moment when the strategy shifts from accumulation to extraction.

This is the turning point most people never reach, not because it is complicated, but because they never build enough capital to make it matter.

When a growth position doubles, triples, or even goes up 50%, that gain is not just a number on a screen. It should be seen as future income.

For example, imagine you have a $50,000 position that grows to $80,000.

That $30,000 gain can be redeployed.

At an 8% yield, that single rotation can generate:

$2,400 per year in extra income o

$200 per month

Now scale that across multiple positions over time.

Instead of relying entirely on new contributions from your paycheck, your portfolio starts generating its own income growth through capital appreciation.

This is why growth is so critical early on.

It creates the raw material that can later be converted into cash flow.

The process itself is simple.

You do not sell everything. You do not try to time the market perfectly. You selectively trim positions that have significantly appreciated and reallocate a portion of those gains into income-producing assets.

Over time, your portfolio begins to shift naturally.

Growth positions shrink as a percentage of your portfolio, while income-producing assets expand.

And eventually, you reach a point where your portfolio is generating enough income to cover a meaningful portion of your expenses.

You don’t need $5,000/month to quit.

You need:

Enough income to cover most expenses

Enough flexibility to control your time

At that point, your job becomes optional.

And optionality is what this entire strategy is designed to create.

LOL, I'm listening to this on repeat and will be reworking my portfolio structure. I'm a newbie to this and need the constant reminder. Thank you Cain!