I Moved My HSA and I Am Never Going Back to VTI

Why free cash flow is the right filter for money you cannot afford to lose

I recently moved my HSA (Health Savings Account) over to a self-directed brokerage. The funds had been sitting in the Vanguard Total Stock Market ETF VTI 0.00%↑. This is a pretty standard approach but I believe that VFLO is better suited for the needs of this specific account.

But an HSA comes with a different mandate than the rest of my portfolio. This is not the account where I chase yield. This is the account I need to protect. Medical expenses are unpredictable, and the last thing I want is to need that money during a market downturn and find the balance cut in half.

At the same time, parking cash in a money market and accepting 4-5% while the market runs is not a real strategy either. The goal was to find something that could hold its value when conditions get rough, while still participating in the upside when conditions are good. That is what led me to the VictoryShares Free Cash Flow ETF VFLO 0.00%↑.

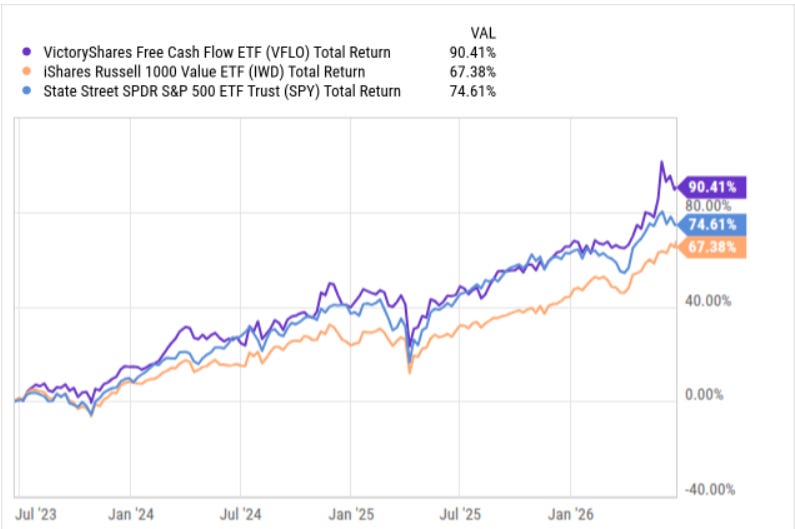

For instance, VFLO has outperformed against VTI since its inception.

👉 Want to see what’s in my portfolio? Paid subs can get access to the full list of holdings in the Yieldly Dashboard.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor. Paid subs get buy alerts first.

A Conservative Approach For Lower Risk

Most people treat their HSA like a savings account. They accept the money market rate, tell themselves it is “safe,” and move on. The problem is that safe and productive are not the same thing.

The S&P 500 has delivered roughly 10% annually over the long run. Sitting in a money market fund means giving up most of that compounding over a multi-decade horizon. For someone in their 30s or 40s, that gap compounds into a significant sum by the time health expenses actually become a major concern.

The other extreme is just as problematic. Putting HSA funds into an aggressive growth fund means taking on full market risk for money that may need to be liquid. If the market drops 30% and you need funds for a medical expense in month two of a bear market, you are forced to sell at the worst possible time.

👉2 Dividend ETFs That Can Protect Your Money During A Pullback.

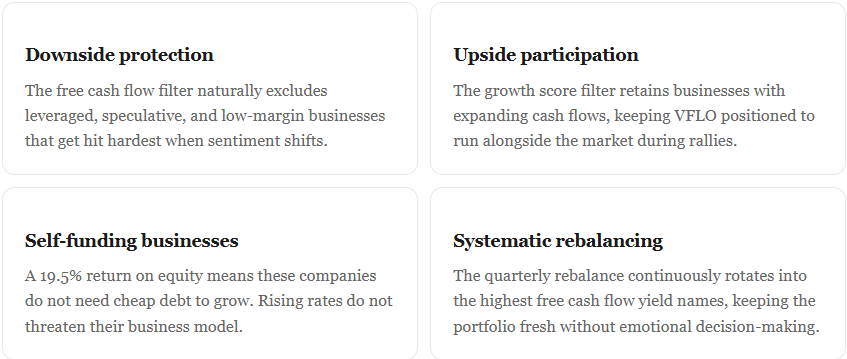

VFLO is built to occupy the middle ground. It targets businesses with durable free cash flow, which means it tends to hold its value better during downturns while still participating in market rallies when conditions are favorable. That is the specific balance I needed for this account.

VFLO Strategy

VictoryShares Free Cash Flow ETF launched in June 2023. It now holds $7.5 billion in total net assets with a 0.39% expense ratio. The fund uses the Russell 1000 as its starting universe but runs everything through a four-step filtering process before anything makes it into the portfolio.

Start with 400 profitable large-cap companies screened from the Russell 1000

Narrow to the 75 stocks with the highest free cash flow yield relative to enterprise value

Filter to the 50 names with the best projected free cash flow growth scores

Weight each position based on the size and yield of its free cash flow

The fund ends up holding 49 positions. That concentration is intentional. Each name has to clear both a yield screen and a growth screen. Companies that look cheap on paper but are not growing their cash get filtered out before they become a problem.

What is inside the portfolio

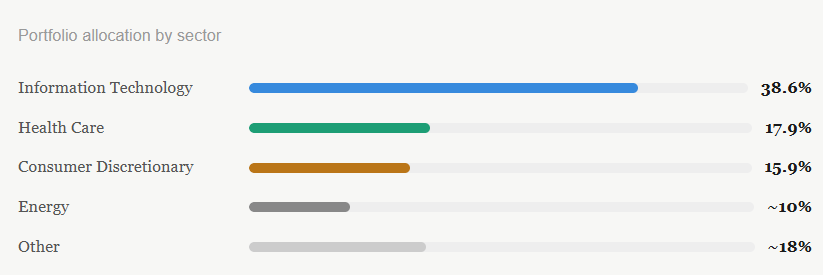

Technology leads the allocation at nearly 39% of assets. That is not surprising given the free cash flow margins large-cap software and semiconductor companies generate. Health care and consumer discretionary round out the next two slots.

Top holdings include Devon Energy (DVN) as the largest position at 3.6% of assets, followed by Expedia (EXPE), Adobe (ADBE), Sandisk (SNDK), and Intuit (INTU). High-margin businesses with real pricing power and cash flow that does not depend on cheap debt to survive.

The Defensive Case: Protects Capital

Free cash flow is not just a quality metric. Companies that generate strong free cash flow can fund their own operations without raising debt, continue investing through slowdowns, and keep buying back shares or raising dividends even when revenue growth stalls. That self-sufficiency is what makes them resilient when the market gets nervous.

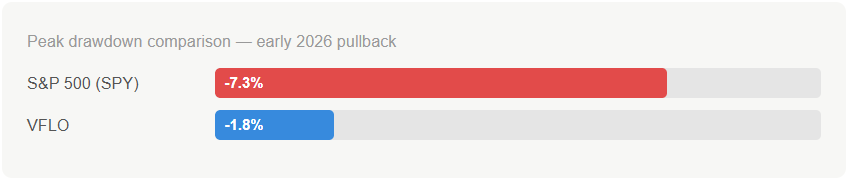

VFLO proved this in live market conditions early in 2026. When uncertainty over the Iran conflict hit, the S&P 500 dropped from its January highs to the bottom. VFLO declined less than 2% over that same window.

The holdings carry a 3-year EPS growth rate of 13.5%, well above the benchmark. That matters because earnings growth going into a downturn is what separates a company that weathers the storm from one that gets caught out. A business that has been compounding earnings at 13% annually has a meaningful buffer before it starts posting actual losses. The market knows this, and it prices that buffer into the stock during a sell-off by selling it less aggressively than the names without that cushion.

The return on equity of 19.5% tells a similar story. ROE measures how efficiently a company converts shareholder equity into profit. A high ROE without excessive leverage means the business is genuinely productive. Most of the companies inside VFLO are generating their returns through strong operating businesses, not by loading up on cheap debt and buying back stock. That distinction matters enormously in a rising rate environment or a credit crunch, because the companies using debt to manufacture ROE get repriced the hardest when borrowing costs go up.

VFLO trades at a slight premium to its benchmark on price-to-book, which means the screen is not just finding cheap companies. It is finding companies that deserve a premium because they generate strong cash relative to their enterprise value. Paying a slight premium for that quality has historically been the right trade. Classic value traps look cheap on price-to-book but have stagnant or declining earnings. VFLO’s screen cuts those out at step one by requiring demonstrated free cash flow and growth.

Upside Growth

Defensive does not mean sitting out rallies.. Many conservative plays protect on the downside but give up so much on the upside that they drag the portfolio over time.

VFLO is different because the free cash flow screen does not just find safe companies. It finds high-quality businesses that also have growth momentum. The yield screen captures companies generating strong cash today. The growth screen filters for companies expected to generate even more cash in the future. That combination means you are holding businesses that can participate in a bull market, not just survive a bear one. After all, the fund is still quite heavily skewed towards technology companies.

Since inception, VFLO has outpaced its benchmark, the Russell 1000 Value Index, as well as the iShares Russell 1000 Value ETF (IWD) and the S&P 500 ETF (SPY). That outperformance has come with less volatility, which is the combination you want in a conservative account.

1.1% Dividend Yield

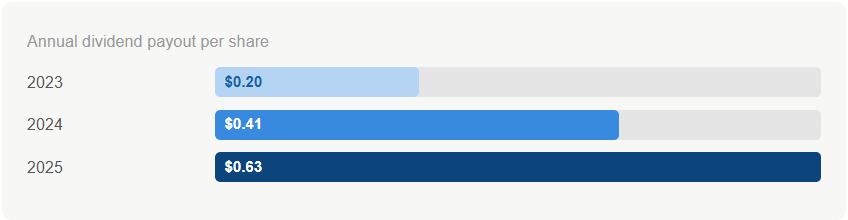

VFLO pays a monthly dividend with a current yield around 1.1%. That is not an income play. But the growth rate on that payout is worth watching. The fund has delivered over 15% dividend growth in the trailing twelve months. That is as if your job gave you a 15% raise annually.

Year-end payouts since inception show a consistent upward trajectory.

An investor who bought in at launch in June 2023 now has a yield on cost approaching 2.1% and rising. As the businesses inside VFLO grow their free cash flow, the dividend follows. Over a longer holding period, I wouldn’t be surprised to see the dividend yield on cost balloon above 5%.

Risks to keep in mind

Nearly 40% of VFLO sits in information technology, and a meaningful chunk of that is software. The market environment for software companies has been difficult. As large language models become cheaper and more capable, investors are questioning whether the traditional SaaS business model still carries the pricing power it once did. If a company charges $50 per seat for a tool that AI can now replicate for a fraction of the cost, the moat starts to look a lot narrower.

Several software names have already seen multiple compression even when their near-term earnings held up, because the market is discounting what the business looks like in three to five years. If the software sector continues to face headwinds, that 40% allocation will be a drag on performance even if the rest of the portfolio holds up well.

Similarly, Consumer discretionary makes up about 15.9% of VFLO’s portfolio. That allocation is a pressure point if household spending starts to slow. Inflation has remained stickier than most forecasters expected, and while the consumer has held up better than many anticipated, that resilience has limits. Higher prices sustained over a long enough period eventually compress discretionary budgets.

The concern is a gradual softening that slowly erodes revenue growth and free cash flow for the companies in this bucket. If that happens, some of the names that passed VFLO’s screen at the last rebalance may no longer look as attractive by the next one. The fund will adjust at rebalance, but the damage to quarterly returns can accumulate in between.

The bottom line

VFLO is not where I am building my income portfolio. For that I use higher-yield positions. But for the HSA, where the mandate is capital preservation with real participation in long-term market growth, it is the right fund.

It filters down to 49 businesses with durable free cash flow and growing earnings. It has proven it can limit drawdowns in live conditions. The dividend is modest but growing above 15% annually. And the 0.39% expense ratio is reasonable for the quality of screen you are getting.

The goal for this account was simple: do not lose money in a downturn, but do not sit out the upside either. VFLO is built to do exactly that.

How does VFLO compare to CGDV?

Thanks for all the investing lessons