Leverage is Your Friend: Get Rich Faster Using Debt

The elite use debt as a multiplier. Learn how to master margin and leveraged ETFs.

I’m using leverage to grow my portfolio to $1M. I’ll show you how and build a case for why leverage isn’t as spooky as people make it seem.

👉 Here’s my last portfolio update.

Wall Street has spent decades training the average investor to be terrified of debt. If you’re like most investors, you’re also terrified of holding individual positions. Don’t you think it’s funny how the people that benefit the most from you locking up your money with them, are the same ones pushing the idea that ETFs are the best way to invest?

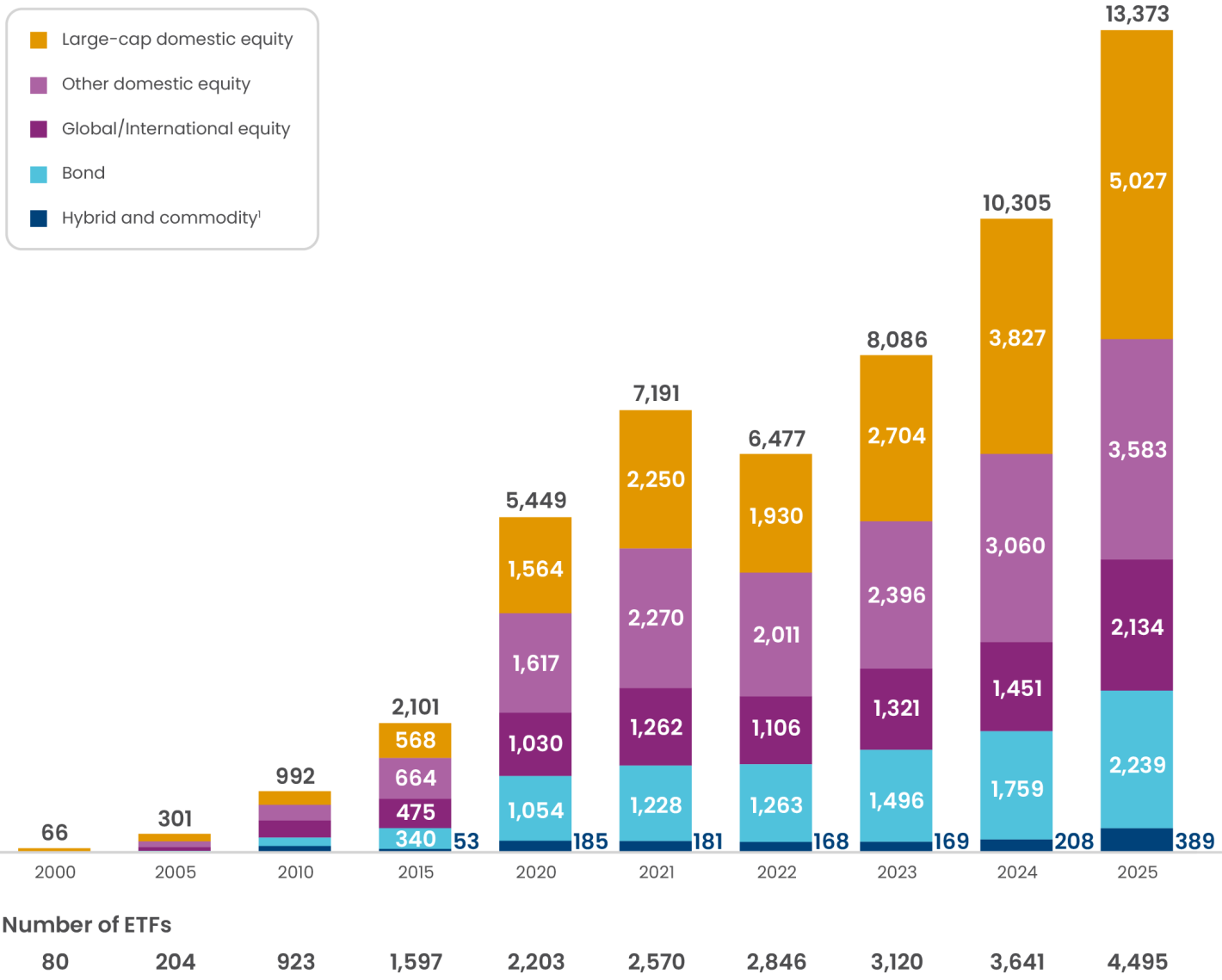

As of December 2025, the total number of index-based and actively managed ETFs, including commodity ETFs, domiciled in the United States stood at 4,495. Total net assets of these ETFs were $13.4 trillion and accounted for 30% of assets managed by investment companies at year-end 2025.

I previously talked about this idea of leverage and how more creates more. I wanted to build on that.

We are told to pay off our mortgages early, avoid credit at all costs, and “invest only what we can afford to lose.” But if you look at the world’s most successful wealth builders, you’ll notice they do the exact opposite. They don’t just use their own money; they use leverage to amplify their reach and accelerate their timelines.

The greats have always understood this. From hedge fund titans to value investing legends, leverage is the “secret sauce” that separates the millionaires from the billionaires:

Warren Buffett: While he preaches caution to the masses, Buffett’s empire was built on insurance float. Did you know that Buffet consistently wrote covered calls on his portfolio? By using the premiums collected by Berkshire Hathaway as low-cost capital to invest in stocks, he effectively utilized billions in leverage to supercharge his returns over decades.

George Soros: In 1992, Soros famously “broke the Bank of England” by using a massive $10 billion leveraged position to bet against the British pound. That single use of debt generated over $1 billion in profit in a single day.

Carl Icahn: As one of the original corporate raiders, Icahn used leveraged buyouts to seize control of massive companies with relatively little of his own capital, allowing him to force changes that unlocked hundreds of millions in value for his personal portfolio.

The lesson is simple: Debt is a tool. When used recklessly, it’s a trap; when used strategically, it is the fastest way to get rich.

This concept is exactly why I believe that we should use leverage to our advantage. As long as you understand the risks, I don’t see anything wrong with.

Amplifying Returns: Leveraged ETFs

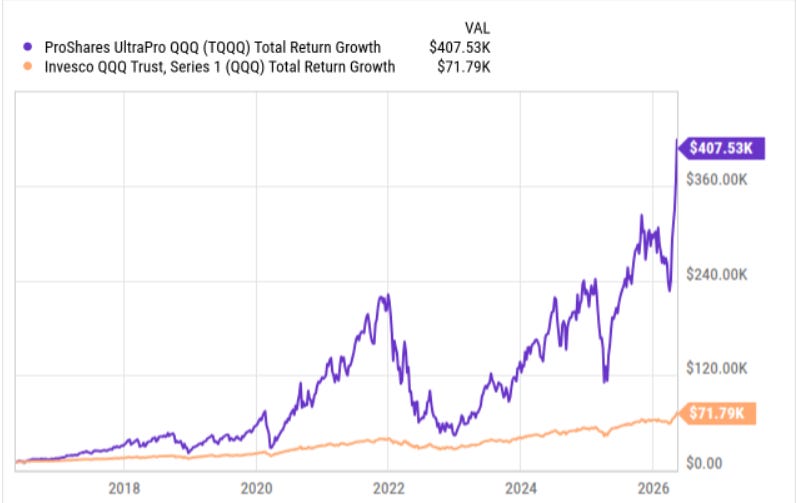

Standard advice suggests that investors should buy an index fund and wait decades for compounding to work, but leverage is for those who refuse to wait. If you are ultra bullish on a specific sector, leveraged ETFs allow you to gain amplified exposure without the need to manually manage a debt account. The primary example of this is the ProShares UltraPro QQQ ETF TQQQ 0.00%↑, which is designed to provide 3x the daily results of the Nasdaq-100 Index QQQ 0.00%↑.

For every 100 dollars invested, the fund maintains roughly 300 dollars of exposure to the index. This leverage is reset every single day, which creates a compounding effect that is extremely powerful during a sustained bull market.

Here’s fun facts about the stock market

Daily: The market is positive around 53-54% of trading days.

Annually: Historically, about 70-75% of years have positive returns, while roughly 25-33% are negative.

Long-Term: The longer you hold, the higher the likelihood of a positive outcome. Over the last 82+ years, 100% of 10-year periods have been positive.

So if 100% of the 10-year periods have been positive, why wouldn’t you use leverage over a longer holding period?

For instance, $10,000 invested into QQQ (A traditional growth ETF) would have turned into $71.8K over the last ten years.

$10,000 invested into the leveraged TQQQ would have turned into $407.5k over the same time frame.

I’ve stated many times that I am optimistic about the outlook of the technology market. AI will continue to be a driving force in the market and the recent earnings growth of the hyperscalers have been incredible. Whether you want to accept it or not, the Supercycle of AI is here.

For this reason, I have initiated small positions in TQQQ 0.00%↑ and a few other leveraged ETFs that I plan to hold for the long-term. If you want to learn more about leveraged ETFs, please leave a comment. I would be happy to build out a playbook for these sort of high risk/high reward funds.

Tech Earnings Roundup: The AI Infrastructure Supercycle Arrives

The Q1 2026 earnings season has officially marked the end of the “AI hype” phase and the beginning of the AI Execution Era. For investors, the narrative has shifted. It is no longer enough for Big Tech to show flashy demos; the market is still scrutinizing the massive capital expenditure (CapEx) required to build the world’s new digital backbone.

Margin Debt

Okay, you’re not a billionaire investor that can utilize millions of leverage. You also may not be comfortable with the idea of leveraged ETFs.

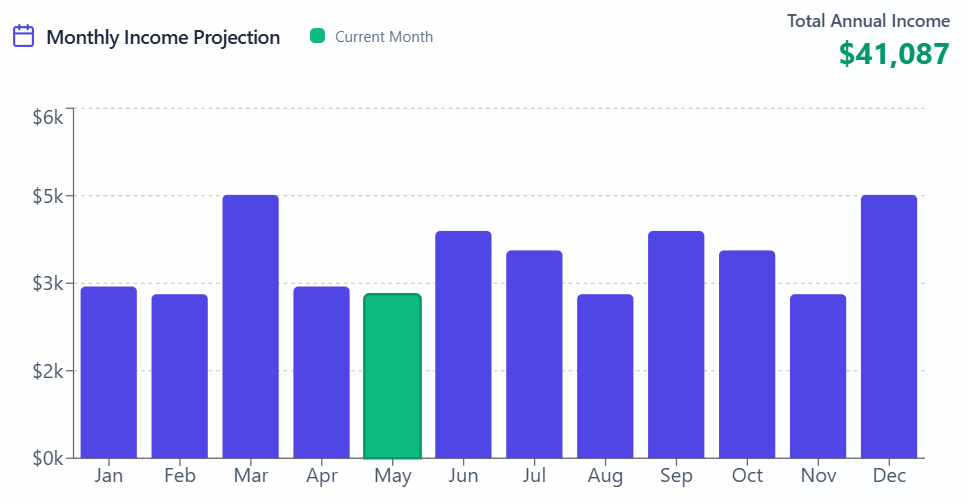

Margin debt allows you to still implement leverage to amplify your returns. I’ve talked about this concept before but I will expand on it here. Margin debt is what allows me to buy high yield ETFs that produce more than $41k in total dividends.

The most direct way for an individual investor to use leverage is through margin debt. A margin account is essentially a line of credit from your brokerage that uses your existing securities as collateral. This allows you to borrow money to purchase additional securities, significantly increasing your buying power beyond your cash balance.

Under standard Federal Reserve Board Regulation T rules, you can typically borrow up to 50 percent of the purchase price of an eligible security. For example, if you have 10,000 dollars in your account, you can use margin to purchase a total of 20,000 dollars worth of stock by borrowing the additional 10,000 dollars. This doubles your exposure to the market, meaning a 20 percent increase in the stock’s price would result in a 40 percent return on your initial cash investment.

Margin accounts offer several unique advantages that traditional loans do not. They have no fixed repayment schedule, meaning you can carry the debt as long as you want, provided you maintain the required level of equity in your account. The interest rates on margin loans are often more competitive than consumer options like credit cards because the loan is secured by your portfolio.

I believe that using margin debt to buy high yield income producing securities can be extremely effective.

Buying Cash Flow With Debt

While most people use margin for aggressive growth, one of the most powerful ways to use debt is to amplify your income. By using your brokerage’s capital to purchase high yield dividend stocks, you can significantly increase the cash flow your portfolio generates every month. This strategy effectively turns your portfolio into a private banking system where you borrow at a wholesale rate to collect a retail yield.

If you invest $100,000 dollars of your own cash into a stock with a 6 percent dividend yield, you receive $6,000 dollars per year in passive income.

However, if you use margin to borrow an additional 50,000 dollars and invest that into the same stock, you now own 150,000 dollars of that asset. Your total dividend payment jumps to $9,000 dollars per year. Even after you pay back the interest on the 50,000 dollar loan, you are often left with a much higher net profit than you would have had by using only your own cash.

👉 This creates a spread that works in your favor.

I personally use this exact strategy. I posted a result of my 2025 margin strategy that you can view below.

I Took Out $75K Of Debt To Buy Stocks: Here's What Happened

We are taught from a young age that “debt is bad.”

As long as the dividend yield of the stock is higher than the interest rate you are paying to the broker, you are generating “infinite” yield on the borrowed money. In the current 2026 market environment, where high yield business development companies and real estate investment trusts are yielding between 8 and 10 percent, this spread can be substantial.

You are essentially using the broker’s money to pay for your own lifestyle or to reinvest back into the market to speed up your compounding.

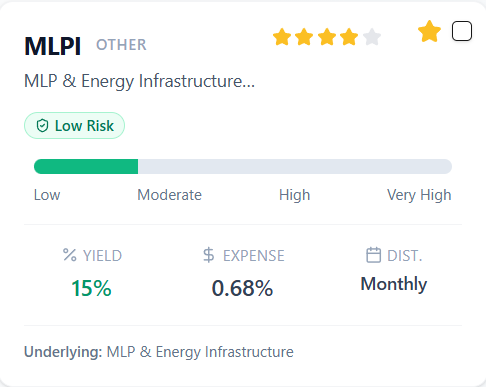

The tricky part is finding a high yield ETF that offers strong returns and grows your capital. This is where the High Yield Database comes in. I’ve compiled a list of 100 high yield funds and rated them.

For example, MLPI 0.00%↑ is a 4-star rated fund that offers a 15% dividend yield.

This approach is how wealthy investors manage to live off their assets without ever having to sell their shares. Instead of selling a winning position and paying a massive tax bill, they simply borrow against the value of their portfolio. The dividends from their holdings pay off the interest on the loan, and they are left with the excess cash to spend as they please. It is a sophisticated way to unlock the value of your wealth today rather than waiting decades to enjoy it.

The Risks: A Double-Edged Sword

Leverage is a powerful tool, but it is also a double-edged sword that can cut deep if you do not respect the mechanics. The same force that triples your gains in a bull market will triple your losses in a downturn. During the market volatility of 2022, while the standard QQQ declined by roughly 32.6 percent, the leveraged TQQQ experienced a massive collapse of over 79 percent.

This happens because leverage is a multiplier of both direction and magnitude; it does not care if the price is moving up or down.

One of the most dangerous invisible risks for leveraged ETFs is a concept known as volatility decay or erosion. Because funds like TQQQ reset their leverage daily, they are essentially forced to buy more when the market is high and sell when the market is low to maintain their 3x ratio.

In a “choppy” market where prices move sideways with high daily swings, the fund can lose value even if the underlying index ends up at the same price it started. A 20 percent decline in the index requires a 25 percent gain to recover, but in a triple leveraged fund, that same 20 percent drop becomes a 60 percent loss, requiring a massive 150 percent gain just to break even.

When using direct margin debt, the primary danger is the margin call. If the value of your securities falls below a specific threshold—known as the maintenance margin—your broker will demand that you deposit more cash immediately. If you cannot provide the funds, the broker has the legal right to sell your positions at the bottom of the market to cover the debt, often without even notifying you first. Additionally, margin interest is not a fixed cost. If interest rates rise, the cost of carrying your debt can quickly eat into your profits, especially if your investments are flat or declining. Leverage can accelerate wealth, but without a strict exit strategy and risk management, it can just as easily lead to a total wipeout of your capital.

Takeaway

The difference between the wealthy and the working class often comes down to their relationship with debt; while most use it to buy liabilities, successful investors use it to acquire assets that accelerate financial freedom. Leverage is a force multiplier that allows you to control more capital and generate more income, effectively turning a static brokerage account into a dynamic business that builds wealth in a fraction of the time. Whether you are utilizing the positive compounding of TQQQ or the amplified cash flow of a margin account, the key is to move from being a passive participant to an active wealth builder who manages debt as a strategic tool. However, the secret to surviving this "great accelerator" is moderation and discipline; by keeping debt levels manageable and focusing on high-quality assets, you ensure that you own the tool rather than letting it own you. Master the mechanics of leverage, and it becomes the most powerful friend you have in your quest to get rich faster.

This is a thoughtful and important conversation because leverage is one of the least understood accelerators of wealth creation.

I actually agree with the broader premise that many wealthy individuals use leverage strategically — but I also think survivability matters just as much as acceleration.

Leverage amplifies outcomes in both directions.

The difference between productive leverage and destructive leverage often comes down to:

timing,

cash flow stability,

risk tolerance,

asset quality,

tax structure,

and whether someone can psychologically and financially survive volatility long enough for compounding to work.

I also think there are different forms of leverage:

financial leverage (debt),

business leverage (systems),

technology leverage (AI),

media leverage,

and ownership leverage.

Many of the world’s wealthiest people ultimately combine several at once.

Personally, I’ve become increasingly interested in the idea that the real goal is not maximizing returns at all costs — it’s maximizing long-term compounding while avoiding catastrophic downside.

That balance between leverage and resilience is fascinating.

— Dr. Rich Bushart

P.S. I explore themes like leverage, ownership, timing, and compounding more broadly in my newsletter, The Billionaire Gap.

Debt is a tool, but retail margin is not Buffett float. Leveraged ETFs are not long-term compounding machines unless the path happens to be friendly -- which it often is not. And buying high-yield funds with borrowed money is not “infinite yield”; it is a carry trade with liquidation risk.