The $100/Day Dividend Machine: A Guide to Replacing Your Salary

Stop trading your time just to keep the lights on. Here are the 3 monthly-paying assets that will buy back your morning.

It’s 6:30 AM on a Tuesday. Your alarm goes off, and before your feet even hit the floor, the familiar dread sets in. You might not outright despise the work you do, but you absolutely hate your reliance on it. You know the uncomfortable truth: if you stopped clocking in tomorrow, the money stops with you.

You are forced to trade the best hours of your week just to keep the lights on, put gas in the car, and cover the weekend takeout. The traditional financial industry tells you the only escape is to grind for forty years, stash away $3 million, and pray you can finally relax when you hit 70.

Let’s shrink the goalpost.

Instead of agonizing over how to fund a thirty-year retirement decades from now, what if you just focused on buying back tomorrow?

This is where the magic of the $100/day milestone comes in.

There is a profound psychological shift that happens when your portfolio generates $100 every time the sun comes up. That $100 a day translates to $36,500 a year. It is the ultimate financial tipping point.

Think about what $36,500 actually covers. It pays the mortgage. It covers the rising property taxes, the monthly utility bills, your digital subscriptions, and those fast-casual orders on Friday nights. It creates an absolute “income floor” beneath your life. You aren’t buying a yacht in Monaco, but your baseline survival is completely funded whether you swipe your badge at the office or not. You suddenly get to work because you want to, not because you have to.

The Blueprint – 3 Assets to Accelerate the Snowball

You cannot build a high-performance machine with just one gear. To hit $100 a day without needing millions of dollars, we need to construct a portfolio with three very specific engines:

A heavy lifter

Monthly cash-flow generator

Compounding growth mechanism.

Let’s start with the heavy lifter.

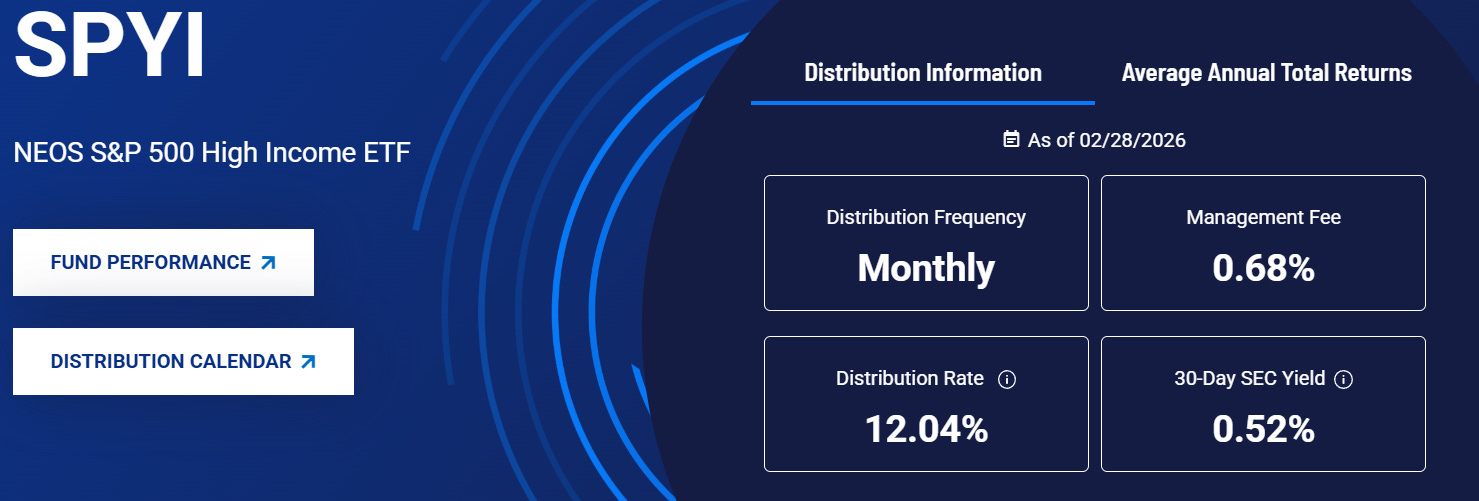

Asset 1: NEOS S&P 500 High Income ETF (SPYI)

If you go to a traditional financial advisor, they will tell you to put all your money into an S&P 500 index fund. And they aren’t completely wrong—the S&P 500 contains the greatest, most profitable companies on the planet.

But there is a fatal flaw with traditional S&P 500 funds when it comes to financial freedom: They yield a pathetic 1.5%. Because the dividend is so small, the only way to generate $100 a day to pay your bills is to actively sell off your shares. You have to cannibalize your own portfolio. Every time you sell a share to pay for groceries, you permanently destroy a piece of your income-generating machine.

Enter SPYI 0.00%↑

SPYI is a brilliant ETF that solves this exact problem. It holds the same underlying mega-cap companies you want in the S&P 500 (like Apple AAPL 0.00%↑, Microsoft MSFT 0.00%↑, and Amazon AMZN 0.00%↑), but it uses a sophisticated options strategy, specifically selling call option spreads, to generate massive amounts of cash flow on top of those holdings.

In plain English? They rent out your stocks to institutional traders, collect massive cash premiums, and pass those premiums directly to you every single month.

The Math for the $100/Day Machine: Let’s look at the exact numbers. To generate $36,500 a year ($100 a day) from a standard 1.5% S&P 500 index fund, you would need a staggering $2.4 million invested. For most people, that is an impossible mountain to climb.

Instead, SPYI currently boasts a forward distribution rate of roughly 12.0%. Because the yield is so high, the math completely flips. At a 12% yield, you only need about $304,000 invested to generate that exact same $100 a day.

This is your foundation. This is the heavy lifter of your portfolio that shaves literally two million dollars off the amount of capital you need to reach your daily income goal. With a 12% yield, your money is working eight times harder than it would in a traditional index fund, completely eliminating the need to ever sell a single share to survive.

Asset 2: EPR Properties (EPR)

Have you noticed how nobody can afford a house, but every vacation destination, concert venue, and ski resort is packed to the brim?

Welcome to the era of “poverty luxury.”

The math on traditional milestones is currently broken. A massive chunk of the middle class has accepted that buying a 4-bedroom suburban home just isn’t in the cards right now. But rather than hoarding every penny in a savings account, they are aggressively pivoting their disposable income toward premium, high-end experiences.

When I booked a trip to Hersheypark last year, adding the unlimited Fast Track passes to skip the lines wasn’t an agonizing financial decision—it was the whole point of the weekend. Consumers across the board are actively choosing immediate memories over distant mortgages. They are splurging to feel rich on the weekends, even if they are renting on the weekdays.

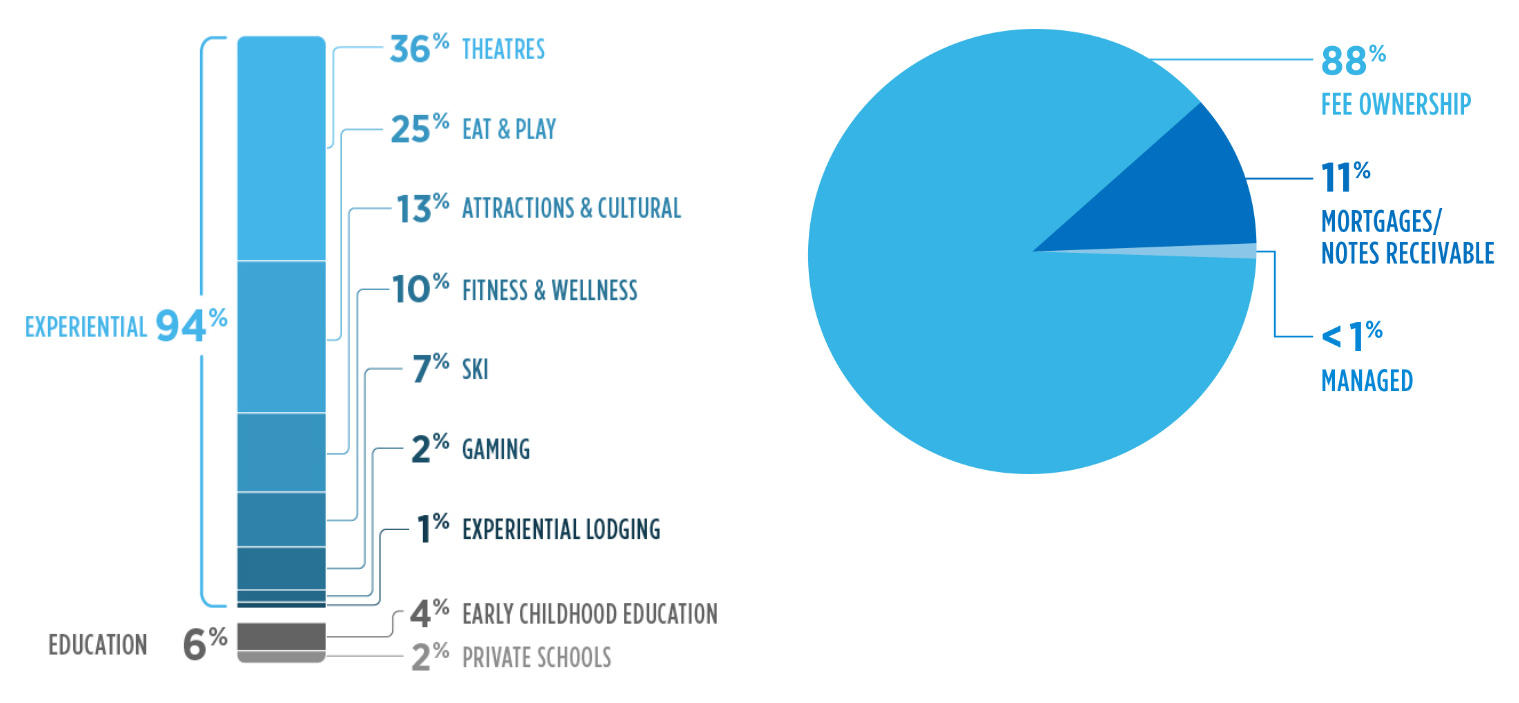

This is exactly the macro trend EPR Properties captures. Looking at the portfolio below, we can see that EPR 0.00%↑ owns tons of different experienced-based properties.

EPR is a $5.5 billion Real Estate Investment Trust and offers a pure-play on the experiential economy. They own the real estate under Topgolf locations, ski resorts, movie theaters, and regional amusement parks. They lease these properties out on long-term, triple-net leases, meaning their tenants cover the taxes, insurance, and maintenance while EPR simply collects the checks.

The Math for the $100/Day Machine: EPR is a monthly dividend powerhouse. Right now, it offers a massive forward yield of roughly 7.1%, paying out $0.295 per share every single month. Let’s crunch the numbers: to generate your $36,500 a year ($100 a day) strictly from EPR, you would need approximately $514,000 invested.

While that requires more capital than the SPYI foundation, remember the alternative. It is still almost $2 million less than what you would need in a standard index fund. By plugging EPR into your portfolio, you are directly capturing the cash flow of this “poverty luxury” spending boom. You are letting the weekend splurges of millions of consumers fund your daily income floor.

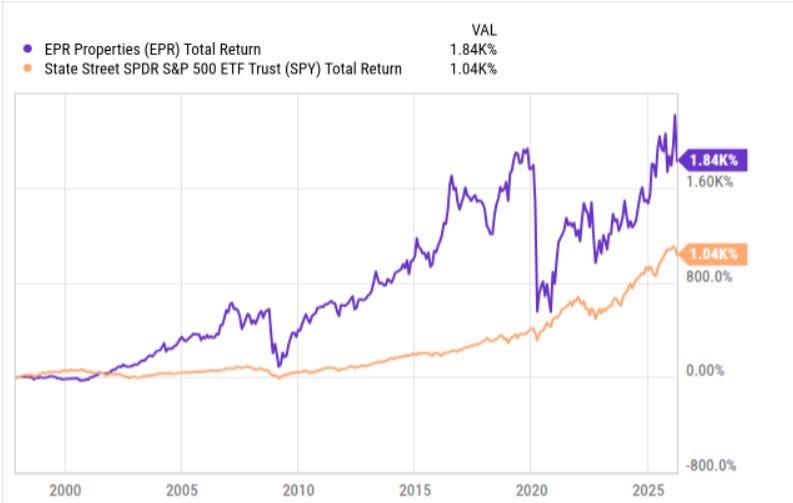

EPR has historically crushed the S&P 500 in total returns as well.

I recently highlighted EPR in one of my prior articles talking about 5 different monthly paying real estate stocks.

5 Monthly Paying Real Estate Stocks: How to Build a Real Estate Empire

The dream of “passive income” in real estate is often sold as a montage of flipping houses or managing a string of suburban rentals. But for most people, the reality is a second full-time job. Between the massive down payments, the rising cost of property taxes, and the “three Ts”

Asset 3: Amplify Enhanced Dividend Income ETF (DIVO)

If SPYI gives us massive yield and EPR gives us real estate cash flow, we have one final enemy to defeat: Inflation.

If you build a portfolio strictly out of ultra-high yielders, your $100 a day will be worth a lot less in ten years. A gallon of milk will cost more, your property taxes will go up, and your car insurance will jump. Your income machine needs a built-in mechanism that gives you a “raise” every single year to outpace the cost of living.

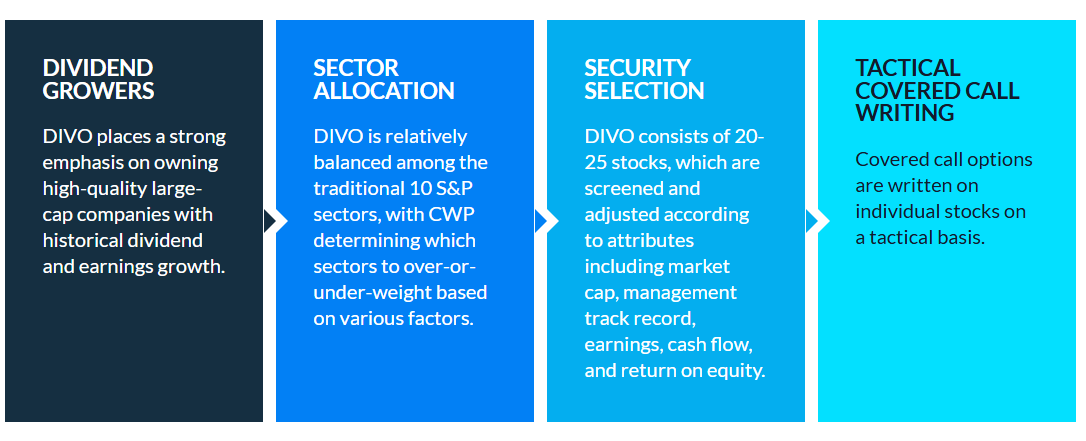

That is where DIVO comes in. DIVO 0.00%↑ offers investors a dividend yield of 4.8%, that has the power to grow over time.

DIVO isn’t trying to give you a flashy 12% yield. Instead, it holds a concentrated basket of 20 to 25 high-quality, blue-chip companies that have a relentless history of growing their dividends. We are talking about the absolute titans of industry—companies like Microsoft, Home Depot, and UnitedHealth—businesses that consistently raise their payouts year after year.

To boost the income, DIVO’s managers opportunistically write covered calls on individual stocks within the portfolio. This strategy captures the upside of these world-class companies while generating an extra layer of cash flow.

The Math for the $100/Day Machine: DIVO currently yields roughly 4.8%, and just like SPYI and EPR, it pays out every single month. If you were to fund your entire $100/day machine using only DIVO, you would need approximately $760,000 invested to hit that $36,500 a year.

While its yield is the lowest of the three and therefore requires the most capital upfront compared to SPYI or EPR—its job is the most important for your long-term survival. You aren’t buying DIVO for the immediate high yield. You are buying it for the capital appreciation and the relentless annual dividend growth required to ensure that your $100/day machine eventually turns into a $150/day machine without you having to lift a finger.

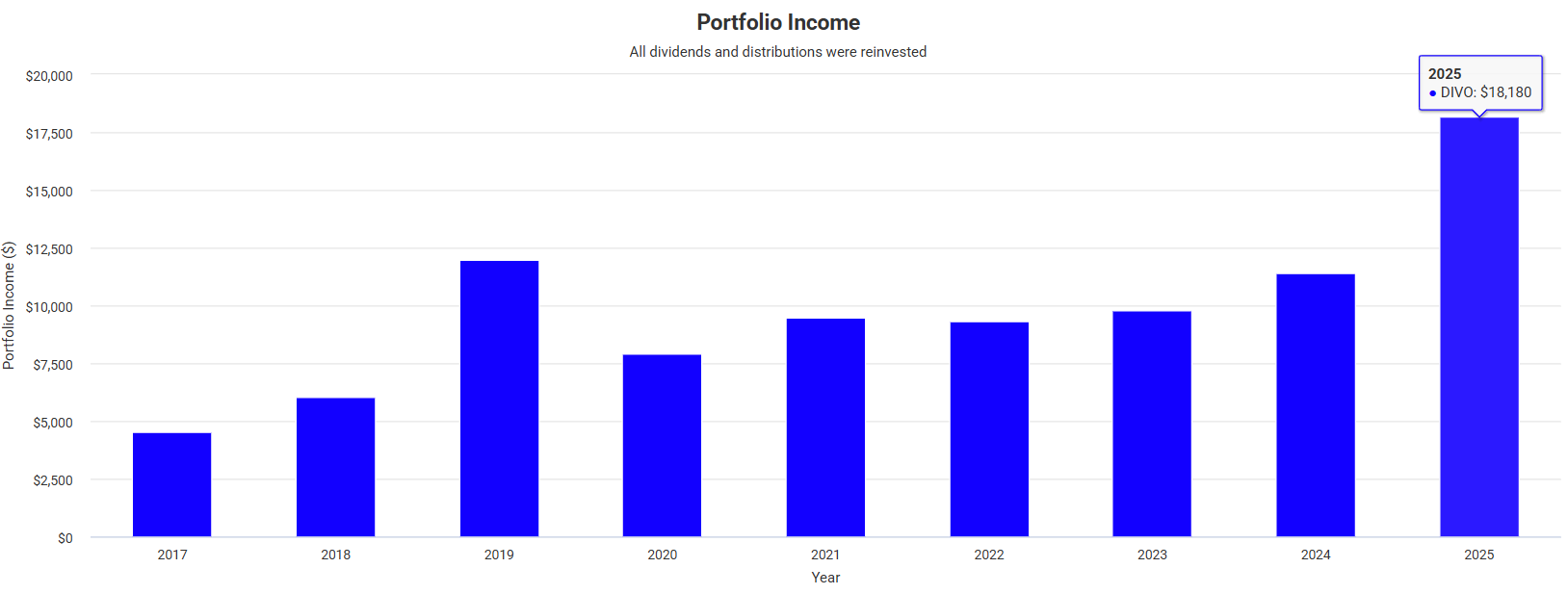

To demonstrate the power of DIVO, let’s assume you invested $100K into the fund at the start of 2017. Let’s assume that you never added more capital after the initial $100k, but you reinvested all dividends back into the fund. Here are the results.

2017 Dividend Income: $4,531

2025 Dividend Income: $18,180

Your income would have quadrupled without adding any new capital.

Section 4: The Secret Weapon – The DRIP Snowball

You now have the three-part engine: SPYI for heavy lifting, EPR for real estate cash flow, and DIVO for inflation-beating growth.

But you might be looking at that $456,250 target and thinking, “That is still a lot of money to save.”

Here is the secret: You don’t have to save all of it. You just have to get the snowball rolling and let the math take over.

This brings us to the most powerful force in finance: DRIP (Dividend Reinvestment Plan).

When you are first building your portfolio, your $100/day machine won’t actually be paying out $100. In the beginning, it might only pay you $5 a day. If you take that $5 and buy a coffee, you kill the machine. But if you turn on DRIP, you instruct your brokerage to automatically take every single dividend check and use it to buy more shares of the stock that just paid you.

This creates a violent, upward compounding loop.

Month 1: You buy shares of EPR. They pay you a dividend.

Month 2: That dividend buys you more shares of EPR. Now, your original shares and your new bonus shares are paying you dividends.

Month 3: The cycle repeats, but faster.

Suddenly, you aren’t just relying on your own bi-weekly paycheck to fund your account. Your portfolio is literally buying itself. The velocity of your wealth accelerates exponentially. By the time you reach that $456,000 finish line, a massive percentage of that capital wasn’t money you saved—it was money your money printed for you.

Section 5: The Execution

The difference between reading a financial newsletter and actually retiring early comes down to execution and tracking.

You now have the exact blueprint to build a portfolio that pays your mortgage, buys your groceries, and funds your life—without ever selling a single share. The era of the $3 million retirement myth is over. It is time to start building your $100/day machine.

👉 Ready to track your own $100/day snowball? Paid subscribers get instant, lifetime access to the Yieldly Dashboard. You can track your exact monthly dividend income, monitor your compounding growth, and see real-time updates on my personal portfolio moves.

I track my monthly income with Yieldly.

The crypt respects the discipline. Cash flow and repetition matter. But dividends aren’t a machine, they’re a contract with the cycle. They hold, thin, or break under stress. Good structure, just don’t mistake process for inevitability. 🕯️

Have you checked out the REIT Millrose Properties? Lennar spin-off. 10% dividend right now