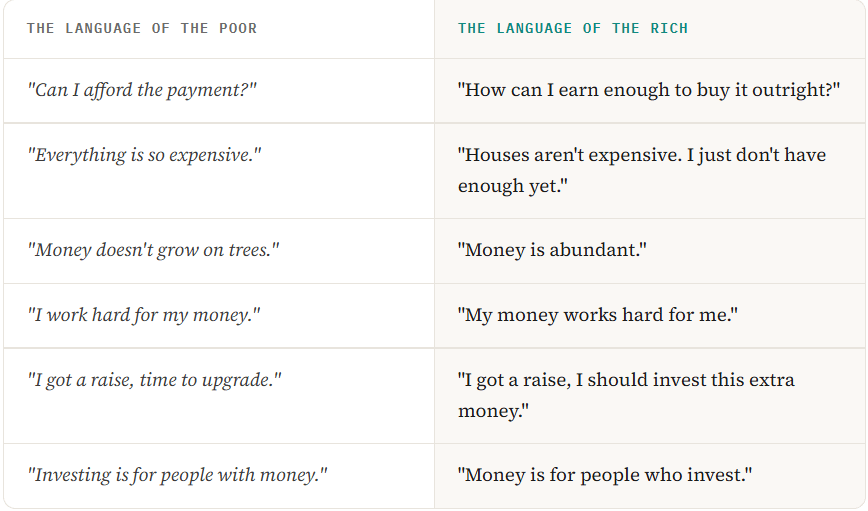

The Language of the Poor: The 3-Layer Approach To Building Wealth

Rich people buy income. Poor people buy payments. Dividends are how you switch languages, and the switch is free.

Listen to How People Talk About Money

Growing up middle class, I had to do things that were efficient. I picked the cheapest college, picked a major based on how much money I could make, I had to buy a Honda or Toyota because of reliability, I chose food from restaurants that had the most value, and I played video games because it was cheap compared to other hobbies.

I was repeating the cycle of the poor and I’m sure that you have done the same in some capacity. How you talk is one of the biggest indicators of how you view money. You have likely heard these sentences. It’s the language of the poor that keeps you aligned with the perspective that money is limited.

“Everything is so expensive.”

“The system is rigged against people like me.”

“Investing is just gambling for people with money to lose.”

“I’ll start saving when I earn more.”

“Must be nice.”

“I work hard, I deserve to treat myself.”

“I’ll never be able to retire anyway.”

I grew up listening to most of the folks around talking like this. As you gain a little more life experience out of your circle, you learn that money isn’t so limited for everyone. While you may be out there complaining about the price of eggs, some people aren’t.

I was fortunate to learn this from my first corporate job. I worked with sales people that brought in $50k a month in commissions. So naturally, these people owned a lot of nice shit. Nice cars, watches, and frequent travel —all of the cliche materialistic stuff. They spoke about life in a way that was so optimistic and it stood out to me. Meanwhile I viewed life through a negative lens at the time — one that believed things and opportunities were limited. My coworkers had the option to live a life that wasn’t focused around efficiency and that fascinated me at the time.

Here is the uncomfortable part, and I am saying it because nobody profits from telling you. The payment vocabulary was installed in you on purpose. Every financed phone, every 72-month car loan, every buy-now-pay-later checkout is an industry translating your future income into their present income.

👉 Your debt payments are someone else’s passive income.

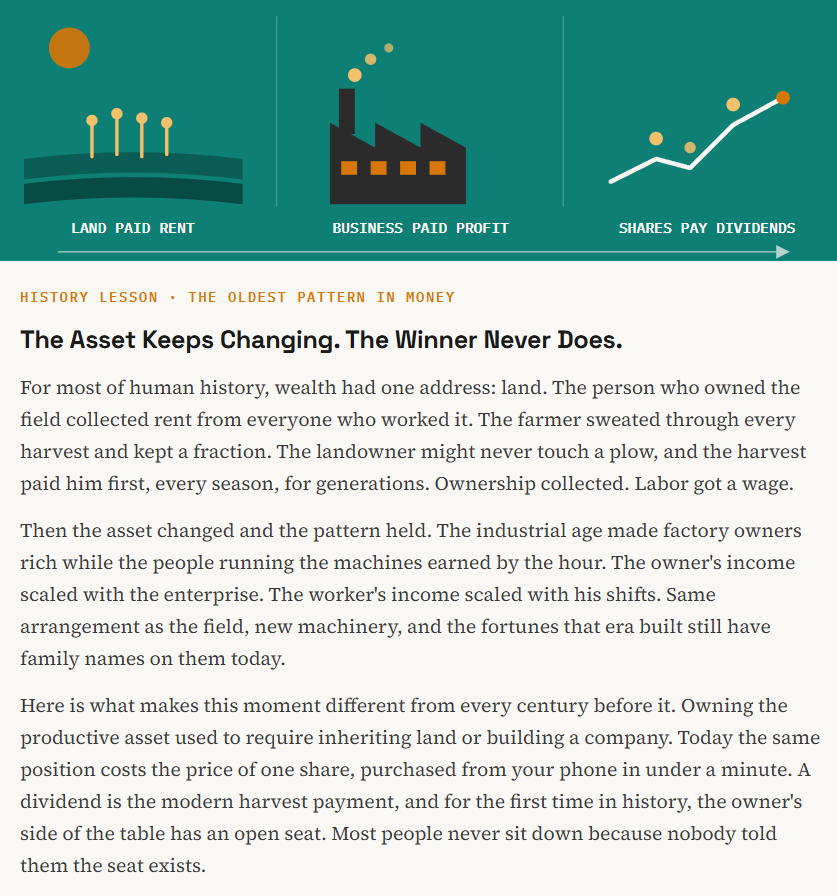

Scarcity Is False: Become An Owner

The language of the poor is built on one false belief: money is scarce. It feels scarce because the only money most people ever see arrives through a paycheck, rationed out twice a month by someone else. But zoom out. Companies paid out hundreds of billions of dollars in dividends last year alone. Cash is everywhere. It just flows to owners, and it always has since the beginning of time.

Money earned with time has a hard ceiling.

You have one body, limited hours, and finite energy, and every dollar of salary spends a piece of all three.

Money earned with money has no ceiling at all.

A dollar you invest works 24 hours a day, never gets tired, never calls in sick, and never asks for a weekend off. It even works while you are at your job earning more dollars to send in behind it.

Dividends are the simplest bridge between those two worlds. Buy a share of a quality payer once and it pays you again and again, no timing, no charts, no skill required after the purchase. The first deposit hits your account and something permanent clicks. Your money just earned money without you. That single moment kills the scarcity belief faster than any book ever could.

And you do not need to be rich to trigger it. You need a first position and a plan, and I already wrote that plan down to the exact dollar.

Investing With Scraps Is The Language of the Poor

Here is the habit that keeps most people on the wrong side of the divide, and almost nobody talks about it.

They treat investing as a leftover.

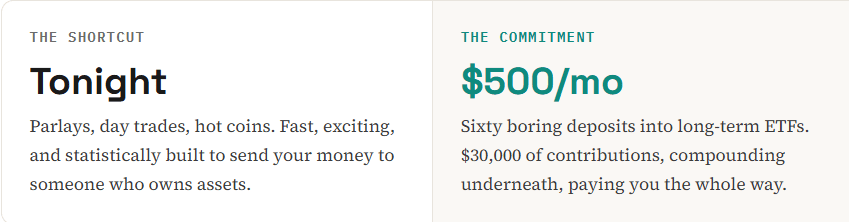

Whatever survives the month after the bills, the subscriptions, and the weekend gets invested, maybe. Some months that number is $50. Most months it is zero. Investing sits last in line for their money, and then they wonder why it never grows.

The disappointment arrives right on schedule. Eight months of scraps produces a tiny balance, the tiny balance feels like proof that investing does not work for people like them, and the search for a shortcut begins. Sports betting. Day trading. Whatever crypto-coin is loud that week. A parlay can hit tonight, and that speed feels merciful compared to the truth nobody wants to hear: $500 a month into boring ETFs for five years will change your life, and it will be uneventful the entire time.

The fix is a one-line change in the order of operations. The language of the poor invests what is left after spending.

The language of the rich spends what is left after investing.

Pay the portfolio first, on a fixed date, like a bill with your name on it.

The other reason people stall at the starting line is simpler: they have no idea what to buy, and the fear of picking wrong feels heavier than the cost of never starting. So I removed that excuse. Free subscribers get my beginner ETF list, the handful of long-term funds I would tell any first-timer to build those sixty deposits around. No cost, no catch, one click below.

👉 Free Subscribers Get The Beginner ETF List

The long-term ETFs I would hand any first-time investor, with what each one does and why it earns a spot. Subscribe free and it lands in your inbox.

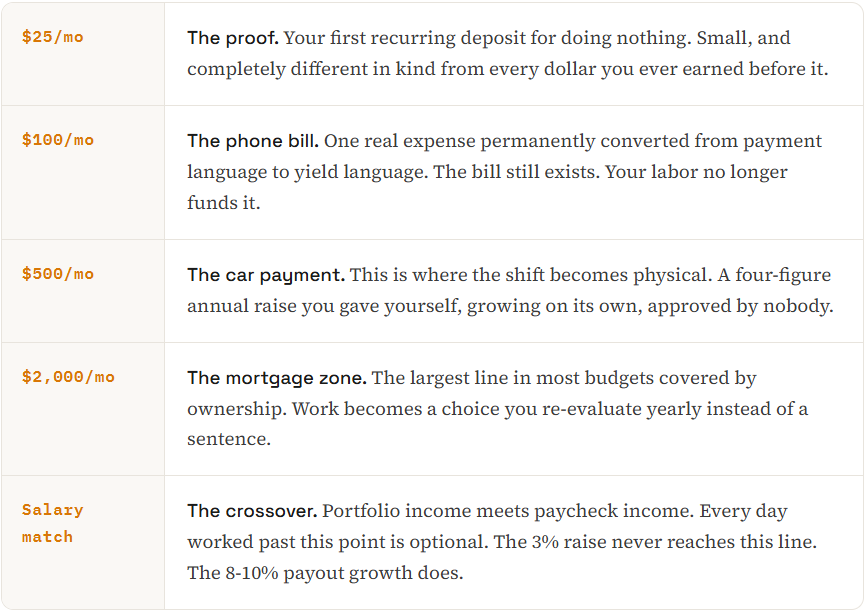

The Milestones That Rewire You

Nobody quits their job at milestone one, and nobody needs to. Each milestone exists to change your vocabulary a little more, and each one arrives faster than the last because reinvested dividends buy more shares that pay more dividends. The snowball works even when you stop pushing.

The gap between milestones shrinks as you go. Climbing from $0 to $100 per month can take longer than climbing from $500 to $1,000, because by then the portfolio itself contributes alongside you. You gain a silent partner who never calls in sick and never asks for a day off.

A portfolio paying $500 per month today, growing payouts at 8% with reinvestment, roughly doubles its income every six to seven years without one new dollar added. Add fresh capital and the timeline compresses hard. Time in the snowball is the only input you cannot buy back later, which makes starting small this month worth more than starting big next year.

Tracking is what keeps the new vocabulary alive during the boring stretch. Watching forward income tick up every month does for investors what a scale does for dieters. I built Yieldly for exactly this job, and paid subscribers use it to watch their crossover date pull closer in real time.

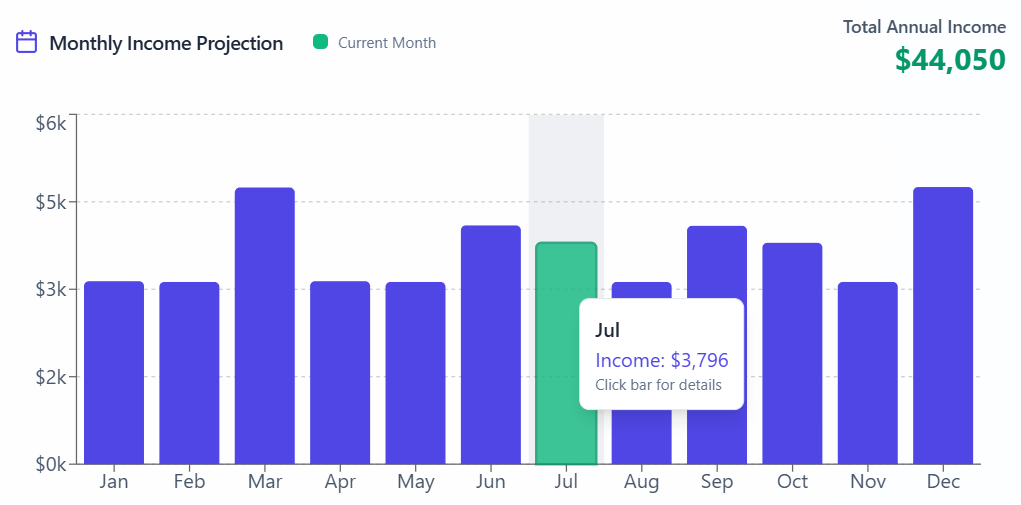

👉 Yieldly Estimates That I Will Collect More Than $44k In Passive Dividend Income.

The Three-Layer Income Engine

The engine has three layers and each one solves a different problem. Layer one is the foundation: pure growth. This layer holds: