What I'd Do With $10,000 to Build $300/Month in Dividends

How I'd Turn a $10K Head Start Into a $300/Month Paycheck in Three Years

Let’s be real, ten thousand dollars is never going to replace your salary or let you walk away from your job tomorrow. What it can do is start working for you the moment you stop letting it sit idle, and that is where most people get stuck. They leave the money in a savings account where it earns almost nothing and loses ground to inflation, waiting for a perfect moment to invest that never shows up.

I would rather put that ten thousand dollars to work today and build something that pays me every single month, with income that lands automatically from assets I own rather than hours I have to trade. Ten thousand dollars is more than enough capital to get that engine running, and once it is running the whole job becomes feeding it and letting it grow.

On its own, that starting stack will only throw off a modest amount of income, so the real growth comes from steady contributions and the patience to let everything compound. Do that consistently and a $10,000 head start can grow into a $300 monthly paycheck within three years.

Below I will walk through exactly how I would build it, from the portfolio structure to the contributions it takes and the honest tradeoffs involved, with no hype and no fantasy about one magic fund that pays 40% forever.

Subscribe. I publish monthly dividend reports showing exactly what this strategy pays me in real time.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor. Paid subs get buy alerts first.

First, Let’s Be Honest About the Math

I’m going to respect your intelligence here, because the internet won’t.

$300 a month works out to $3,600 a year, and to pull that out of $10,000 alone you would need a 36% yield. That kind of return does not exist in any safe or sustainable form. While I do personally utilize these high yield funds, it is very strategic and only makes up a small portion of my portfolio.

So $10,000 by itself should not get you to $300 a month if you are a beginner. Two things get you there when they work together:

Contributions: You add roughly $600 a month of your own money, which is the real engine of the whole plan. Over three years that adds up to about $21,600 of fresh capital stacked on top of your $10K head start.

A higher-yield, income-tilted build: You weight the portfolio toward monthly income producers so a smaller balance throws off more cash, targeting a blended yield around 10% rather than the 3% you would get from a plain index fund.

Pull both levers together and the timeline compresses from roughly a decade down to three years. To be upfront about it, this income-tilted version of a $10K portfolio throws off around $80 a month right out of the gate, and that $80 is the seed your contributions and reinvestment grow into the full $300.

The part I won’t sugarcoat is that chasing a blended yield near 10% means leaning into higher-risk income funds that carry more volatility and a real chance of principal erosion, and that added risk is the price of the faster timeline. A slower and gentler version of this plan absolutely exists, it simply takes longer to reach the same number, so go into the aggressive lane with your eyes open.

Here is exactly how I would build it.

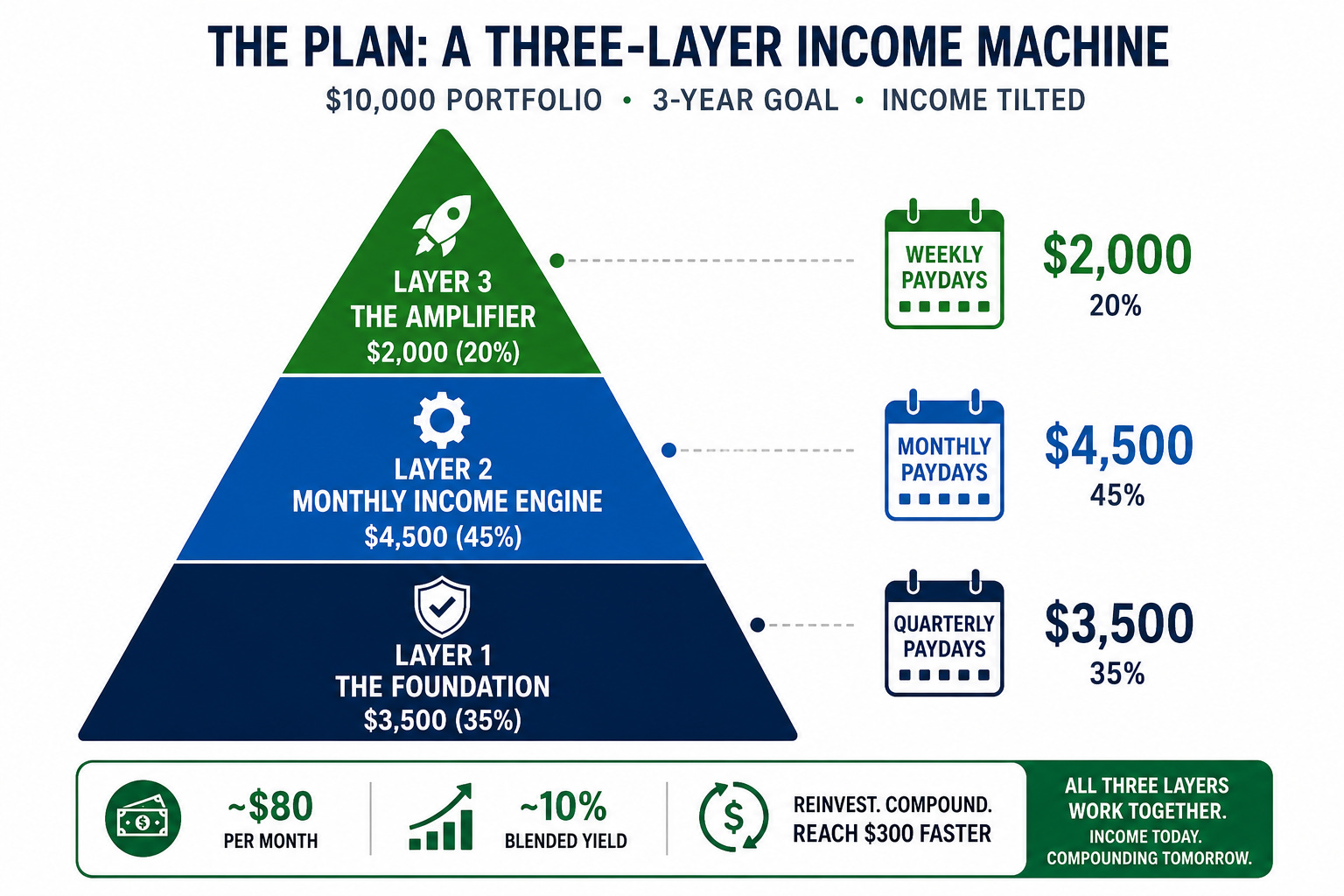

The Plan: A Three-Layer Income Machine

A $1,000 portfolio is really just a foundation, but $10,000 with a three-year goal gives you enough capital to build all three layers and tilt the whole structure toward income. Each layer has a specific job to do.

Layer 1: The Foundation ($3,500, 35%)

This is the bedrock of the portfolio, and it is deliberately boring because it keeps the whole thing from being all gas and no brakes.

Picking your first ETFs is where most beginners freeze up, so I made it simple. Every free subscriber gets my hand-picked list of beginner-friendly ETFs emailed straight to them, which is the exact starting lineup I would hand a brand-new investor on day one. Subscribe for free and it lands in your inbox.

Here is the kind of foundation I’m talking about:

SCHD 0.00%↑ (Schwab U.S. Dividend Equity ETF) - This is the gold standard for dividend-growth investing, screening for quality companies with strong balance sheets and a long habit of raising their payouts year after year. The yield is modest at around 3.5%, but it grows faster than inflation and anchors the entire stack.

VYM 0.00%↑ (Vanguard High Dividend Yield ETF) - This casts a wide net across hundreds of established dividend payers, with low costs and dependable quarterly income, and it pairs cleanly with SCHD without overlapping too heavily.

The reason I lean on this layer is that it almost never gives you a heart attack. When the higher-yield holdings get choppy, this is the part of the portfolio that holds the line.

Layer 2: Monthly Income Engine ($4,500, 45%)

This is the workhorse of a three-year build, and it gets the largest slice on purpose because monthly income is what fuels the reinvestment that reaches $300 quickly.

O 0.00%↑ (Realty Income) This one is nicknamed “The Monthly Dividend Company” for good reason, paying every month and raising its dividend for decades while owning thousands of properties leased to recession-resistant tenants. It is the closest thing to a landlord’s paycheck that you can buy with a single click.

ICAP 0.00%↑ and SPYI 0.00%↑ (Monthly Income ETFs) These funds generate income through actively managed equity strategies and options overlays, then pass it through as monthly distributions with yields in the high single digits to low double digits. They carry more moving parts and more risk than a plain ETF, and they do most of the heavy lifting on cash flow.

The reason I lean on this layer is the rhythm of it. Getting twelve paydays a year instead of four keeps you reinvesting, and consistent reinvestment is what beats the clock.

Paid subscribers unlock instant access to the high yield database, includes more than 120 different income ETFs.

Layer 3: The Amplifier ($2,000, 20%)

This is the high-octane sleeve, and it is what pushes the blended yield toward 10% and shortens the timeline.

This is where YieldMax-style weekly payers like YMAX 0.00%↑ or YMAG 0.00%↑ come in, using aggressive options strategies to pay distributions every week. The headline yields look almost unreal and the principal can erode, which is exactly why I cap this layer at one-fifth of the portfolio. Sized correctly, the steady stream of weekly income gets reinvested back into Layers 1 and 2 and compounds the rest of the machine.

The reason I lean on this layer is that it acts as an accelerant, but an accelerant can burn you if you pour on too much, so position size matters more here than anywhere else in the portfolio.

Stacked together with this income tilt, $10,000 throws off roughly $80 a month at a blended yield near 10%, and that gives you a launchpad to compound from.

Subscribe to follow the build. I share the real holdings and the real numbers every month.

The Engine That Gets You to $300: Reinvest Everything

The single move that does the most work, and costs you nothing, is reinvesting every dividend you receive.

Turn on automatic reinvestment, often called DRIP, inside your brokerage, and every payout immediately buys more shares. Those new shares pay their own dividends, which get reinvested in turn, and the wheel starts spinning on its own:

Your first month buys more shares

Those shares earn their own dividends

Which buy even more shares

Which raise your monthly income

Which buys more still

When your portfolio is paying $80, then $115, then $155 a month and you reinvest all of it, you are adding well over a thousand dollars a year of new income-producing shares without touching your own contributions. Stack that reinvestment on top of your $600 a month and the snowball becomes an avalanche surprisingly fast.

This one habit is the entire difference between building income yourself and letting your income build itself.

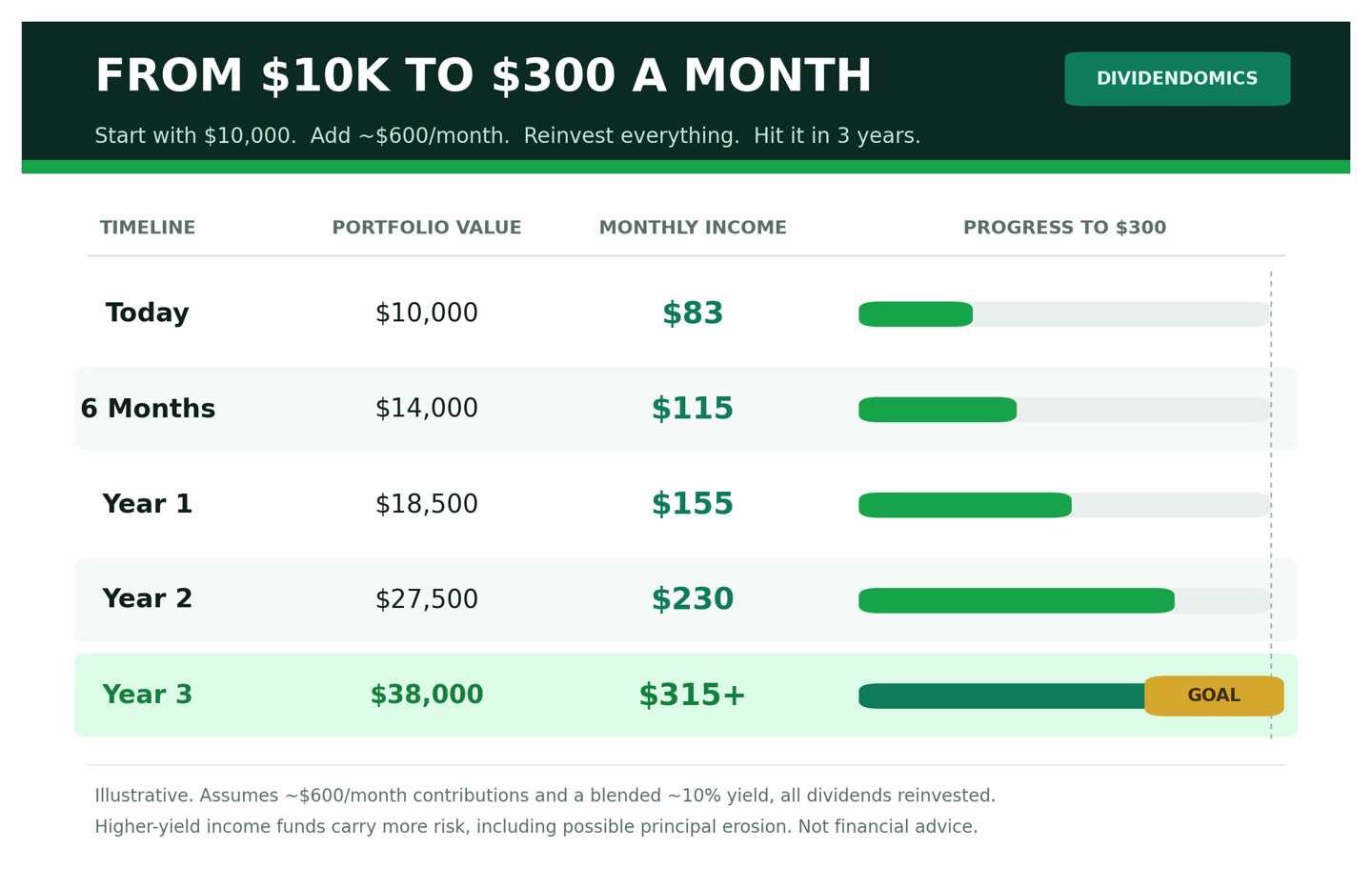

The Roadmap: From $10K to $300/Month in 3 Years

Here is the honest trajectory, assuming you start with $10,000, add about $600 a month of your own, reinvest every dividend, and hold a blended yield near 10% across the three layers:

That is what a realistic three-year build looks like when a head start, steady contributions, and an income-tilted portfolio all work together.

It helps to notice what is really driving those numbers. The bulk of that $38,000 is money you put in yourself through contributions, with returns and reinvestment carrying the rest of the load. Your $10K gets you off the starting line, your $600 a month does most of the building, and the higher yield is what allows a $38,000 balance to pay you $300 a month when a plain portfolio would need closer to $60,000 to do the same job.

If you want to move faster or take on less risk, you have a few dials to turn:

Contribute more. Pushing past $600 a month moves your finish line earlier than three years.

Adjust the yield. A larger tactical sleeve gets you there faster with more risk, while a smaller one is slower and steadier.

Add windfalls. A tax refund, a bonus, or side-hustle cash all jump you up the table whenever they land.

You also feel the progress the entire way, since your income climbs from $80 to $115 in the first six months alone, and that momentum is what keeps you committed when the market gets noisy.

Track Every Dollar Like It Matters

You cannot grow what you refuse to measure.

Every dividend that lands is one more dollar you did not have to earn by trading away an hour of your life. I treat my portfolio like a business, tracking income, yield, and growth every month and cutting anything that stops earning its keep, which matters most in the high-yield sleeve where you have to watch closely for funds that quietly bleed principal.

You can use a simple spreadsheet or my own dividend tracker, because the specific tool matters far less than the habit of using one. For instance, I use my own dashboard that is available to all paid subs.

Watching that monthly number climb from $80 to $115 to $155 is the most motivating part of the entire process, precisely because you built it yourself.

Final Thought: Ten Thousand Dollars Is Where It Begins

You do not need a perfect portfolio, a crystal ball for the market, or a lucky break to make this work. What you need is a head start, the discipline to reinvest, and the consistency to feed the machine every single month.

Ten thousand dollars is more than enough to begin, and yet most people will let it sit, spend it, or gamble it away on the next trend. If you put it to work today across these three layers, reinvest the income, and feed it $600 a month, three years from now you will have a $300 paycheck arriving whether or not you clock in. Then you will do it all over again to reach for the next $300.

That is how ownership works, and it is how you slowly buy back your own time, one dividend at a time.

Dividendomics is a reader-supported publication. To follow this build in real time, including my actual holdings and monthly income reports, consider becoming a free or paid subscriber.

This is how I would approach it personally and is meant for education rather than personalized financial advice. The higher-yield, three-year path described here carries real risk, including the loss of principal, so always do your own research and invest according to your own goals and risk tolerance.

I don’t understand including YMAX or YMAG when they are continuously trending down 43-60%. Surely any dividends received won’t cover your loss?

What about tax impact on dividends?