What Rich People Build Before a Recession Hits

AI is coming for your job. Dividends won't be.

There is a pattern you see over and over if you study wealthy people long enough.

They do not wait for a recession to start preparing for one. By the time the news is calling it a recession, they are already sitting on income streams that have nothing to do with their job, their boss, or how the economy is feeling that quarter.

You can play the same game.

Here is the uncomfortable truth sitting underneath all of this. We are living through one of the most disruptive economic shifts in modern history. AI is replacing entire departments overnight. Accountants, marketers, analysts, coders, customer service teams.

I used to be a financial analyst. Tasks that took me a day to complete can now be tackled by AI within 30 minutes. Roles that felt secure two years ago are disappearing, and every recession gives companies the perfect cover to make those cuts permanent. It will happen eventually.

Most people have one income stream. Their job. One decision by one employer and the whole thing is gone. I experienced my first corporate layoff in 2015. I was basically a kid at the time so it didn’t really matter to me much. I lived at home and had no bills. However, I remembered seeing grown adults stressed about what they were going to do. I was taught early on that most people are just one paycheck away from being broke.

The wealthy figured out a long time ago that the answer is not to work harder or save more aggressively. The answer is to build income that has nothing to do with your employer. Income that lands in your account whether you are working, whether the economy is growing, and whether or not a machine decided to take your job last Tuesday.

That is what this article is about. The exact strategy they use to do it.

The Market Is Rigged. That’s Actually Great News.

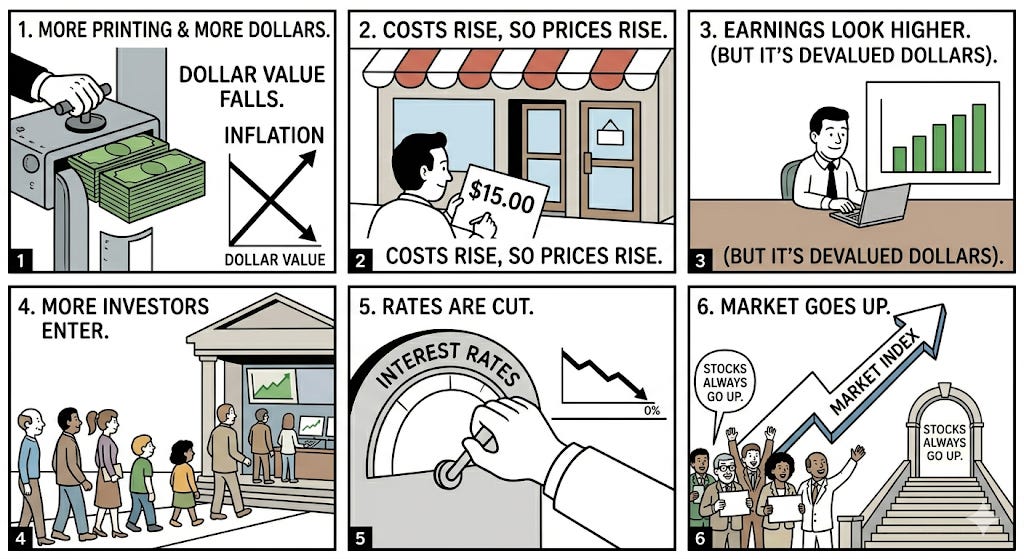

The stock market is designed to go up. No matter what.

Not because of luck. Not because capitalism is perfect. Because of how the entire system is structured.

The S&P 500 is a living index that quietly fires losers and replaces them with winners on a rolling basis. When a company starts to fail, it gets removed. When a new dominant business emerges, it gets added. You’re never actually holding the losers long-term because the index itself won’t let you.

Public companies have every financial and legal incentive to make their stock price go up. They buy back shares. They grow earnings. They raise dividends. Their executives are paid in stock. The entire corporate machine is pointed in one direction.

And then there’s the Federal Reserve. When things get bad enough, the government cuts interest rates and pumps money into the financial system to prevent a collapse. We saw it in 2008. We saw it in 2020. The playbook exists and they’ll use it again.

Does this mean the market goes up every year? No. The 2022 drawdown was brutal. The 2020 crash was terrifying. 2008 wiped out people who panicked.

But zoom out. The market has recovered from every single one of them.

Every. Single. One.

The sooner you genuinely internalize that, the sooner you stop treating every downturn like a crisis and start treating it like what it actually is: a temporary discount on assets that are built to recover.

So why are so many people still losing money in a market that’s rigged to go up?

They sell when it goes down. And they sell because watching your savings drop 30% is unbearable when that number is the only thing your portfolio is doing for you.

Weekly income changes that completely.

👉 Upgrade Your Subscription - $0.82 per day to become a better investor.

Rich People Build Weekly Income

The goal is simple. Build a portfolio where income arrives so frequently that a market downturn feels more like a sale than a disaster.

When clothes goes at sale, you don’t freak out right? So why treat the markets any different?

When you build a system where your account is depositing cash every week, the scary headlines stop hitting the same way. You are not watching your future disappear. You are collecting a paycheck while a system that is built to recover does exactly what it has always done.

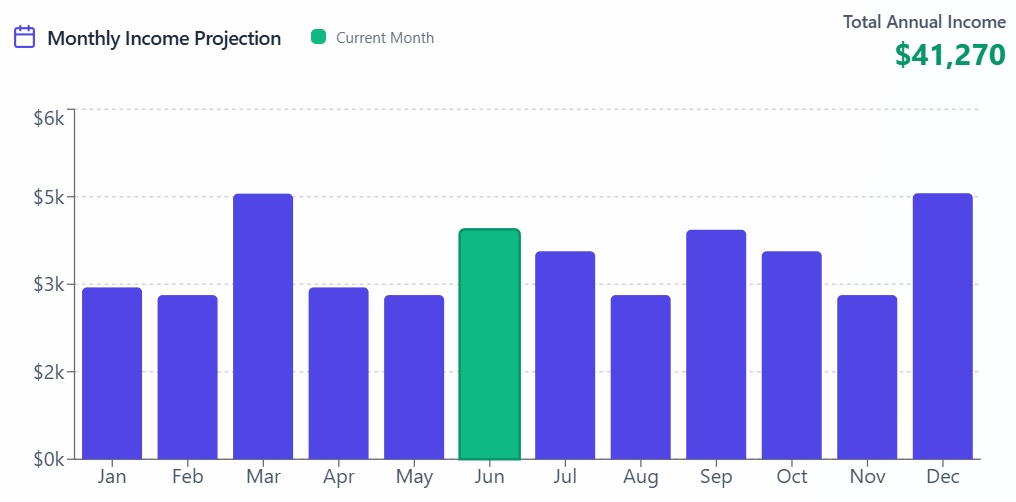

This is exactly what I am working on. I built a portfolio that pays me $41,000 a year and growing. I get paid no matter what the economy is doing or what direction the stock market is moving. Here’s a guide on how to get started.

Job One: Start Investing

Most people treat investing like something they will get around to eventually. When they have more money. When things calm down. When they feel like they understand it better.

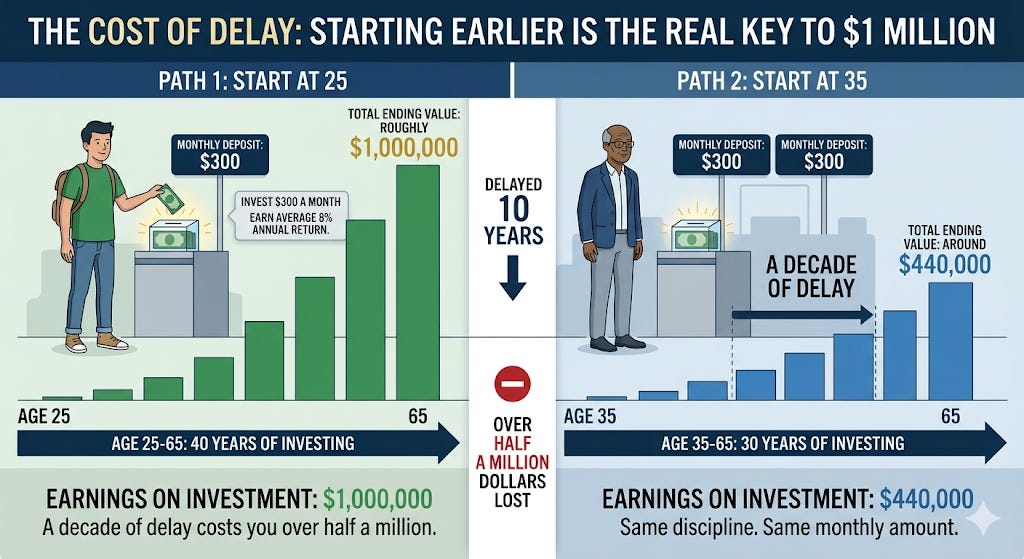

Here is a number that tends to change how people think about this. If you invest $300 a month starting at 25 and earn an average 8% annual return, you end up with roughly $1 million by the time you are 65.

Wait until you are 35 to start the exact same habit and you end up with around $440,000. Same discipline. Same monthly amount. A decade of delay cost you more than half a million dollars.

The reason is compounding. When your investments earn returns, those returns start earning returns of their own. It snowballs in the background and the longer it runs the more violent the growth becomes at the end. The people who retire wealthy are almost never the ones who made one great investment. They are the ones who started early and kept going without stopping.

So what does investing actually mean for someone who has never done it?

At its most basic level, investing means putting your money into something that has the potential to grow or generate income over time, instead of letting it sit in a bank account where inflation erodes its value every year. A savings account paying 0.5% interest while inflation runs at 4% is not safe money. It is money that is losing ground every single day.

When you buy shares in a company or a fund, you are buying a small ownership stake. If the company does well, your stake grows in value. If it pays dividends, it sends you a portion of its profits on a regular schedule, quarterly or monthly, directly into your account. You do not have to sell anything to collect that money. It just shows up.

Opening a brokerage account takes about ten minutes online. Platforms like Fidelity, Schwab, or Vanguard let you get started with as little as $1. You search for the fund you want, enter how many shares or how many dollars you want to put in, and click buy. That is genuinely all there is to the mechanics of it.

Job Two: Get Paid Right Now

Imagine you got laid off tomorrow. How long could you survive on what your investments pay you today?

For most people the answer is zero. Their portfolio grows or shrinks but never actually pays them anything until they sell something.

The first job is to fix that. You want a portion of your money sitting in investments that deposit income into your account on a regular basis, regardless of what the market is doing that day.

This is where a fund like SPYI 0.00%↑ comes in. It generates income by using a strategy called covered calls on S&P 500 stocks, which sounds complicated but the mechanic is simple: it earns a premium for agreeing to sell shares at a set price, and passes that premium to you as income. Currently yielding over 12% annually, paid out monthly.

The part that surprises most people is what happens when markets get rocky. Volatility actually increases the premiums collected, which means the income goes up right when everyone else is panicking. The chaos works in your favor.

Your first job is covered. Money coming in, every month, no employer required.

Job Three: Reinvest & Get Raises

Here is a trap that almost nobody talks about.

Picture someone who retired in 2005 with a $3,000 monthly income from their investments or social security. They felt set. And for a while, they were.

But groceries cost more in 2015 than they did in 2005. Gas cost more. Insurance cost more. Property taxes cost more. That same $3,000 monthly paycheck bought less and less every single year until what felt like financial freedom started feeling like financial strain.

This is inflation doing what it always does. And most income portfolios have no defense against it.

The second job your money needs to do is grow that income over time so you never fall behind. A fund like SCHD 0.00%↑ handles this. It holds some of the most reliable dividend-growing companies in the world and has consistently raised its payout year after year.

Think of it as the annual raise your employer stopped giving you, built directly into your portfolio.

The Only Question That Actually Matters

Remember the person we talked about at the beginning of this article.

The one who does not wait for a recession to start preparing for one. Who is already sitting on income that has nothing to do with their employer, their industry, or whether AI decided to automate their role this quarter. Who is getting deposits while everyone else is refreshing their bank account and wondering what comes next.

That person is not smarter than you. They did not start with more money. They just understood something early that most people figure out too late: your job is not a financial plan. It is a starting point.

The recession will come. The layoffs will follow. The headlines will be loud and the fear will feel very real. And somewhere in the middle of all of it, quietly, the deposits will keep landing for the people who built this before they needed it.

The only question left is when you start.

Not financial advice. All investments carry risk. Past performance does not guarantee future results. Always do your own research or consult a licensed financial advisor before making investment decisions.