What's Going On With Sandisk? (10x Potential Remains With DRAM)

A 3,400% rally. Gross margins that rival SaaS companies. Hyperscalers signing billion-dollar supply contracts.

What if we told you this was a company that was trading at $50 a share just 16 months ago?

What if we told you it’s now up over 3,400%?

And what if we told you it’s not Nvidia? It’s not a software company. It’s not an AI darling with a flashy product launch. It’s a chip maker. Specifically, a company that makes the little flash memory cards you used to put in your digital camera or in the side of your laptop.

That company is Sandisk SNDK 0.00%↑. And before you roll your eyes and say “bubble,” hear me out. Because what’s happening here is one of the most interesting structural stories in the entire semiconductor market, and most investors are still explaining it wrong.

👉 $10,000 invested 12 months ago would now be worth $381K. Crazy!

Here’s the question worth sitting with: what happens when a commodity business stops acting like a commodity? What happens when the buyers: the Microsoft MSFT 0.00%↑, the Amazons AMZN 0.00%↑, the Googles GOOG 0.00%↑ of the world, stop negotiating on price and start signing multi-year, multi-billion-dollar contracts just to make sure they can get the product at all?

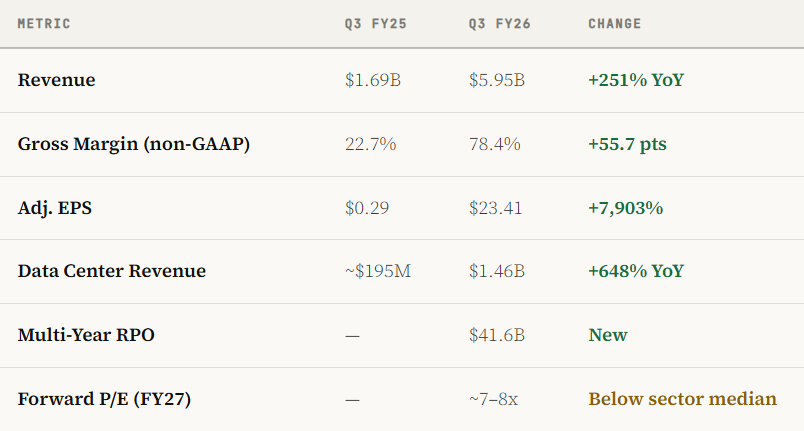

You get 251% revenue growth. You get gross margins of 78%, heading toward 81%. You get $41.6 billion in locked-in future revenue signed in a single quarter. You get a stock that looks expensive until you run the math, and then suddenly it doesn’t.

This is that story. And by the end of it, you’ll understand not just what happened with Sandisk, but where the next leg of this trade is setting up. This is why DRAM 0.00%↑ might be where the real money is still waiting to be made.

We have some smart investors in the paid group who were on it before me.

👉 If you want to get involved with investors who love growing their wealth, talking about stocks, and investing in high quality businesses, consider joining the paid subscription. 10% discount included.

BY THE NUMBERS: Q3 FY26

These aren’t the numbers of a cyclical commodity business. These are the numbers of a software company that happens to manufacture physical chips. So how did we get here?

The Commodity That Stopped Acting Like One

Microsoft, Amazon, Google, Meta are no longer buying enterprise flash memory as interchangeable storage. They’re treating it as core AI infrastructure. When your inference models need to maintain context across millions of simultaneous sessions, when KV cache architectures demand low-latency retrieval at massive scale, NAND flash becomes the connective tissue of the entire operation.

We covered this dynamic in our Tech Earnings Roundup: Microsoft’s $190 billion in 2026 CapEx isn’t discretionary. It’s fulfilling signed contracts. Memory suppliers like Sandisk are on the receiving end of that urgency.

The numbers back it up. Sandisk signed three multi-year supply agreements in Q3 FY26 alone, with two more closed before Q4 ended. Over 30% of fiscal 2027 NAND supply is already sold under long-term contracts, with management targeting above 50%. The $41.6 billion in remaining performance obligations -- backed by prepayments and financial guarantees -- isn’t a talking point. It’s protection against the exact cyclical downturn that NAND bears keep predicting.

Why AI Inference Changed Everything

The mainstream narrative around AI infrastructure starts and ends with GPUs. Nvidia NVDA 0.00%↑ is the pick-and-shovel play, full stop. That framing was never completely wrong. It was always just incomplete.

Think of it this way. A GPU is an engine.

Powerful, fast, expensive.

But an engine without fuel storage doesn’t go anywhere. Every time a large language model processes your query, it needs to retrieve enormous amounts of context: prior conversation, reference documents, intermediate reasoning steps. That data has to live somewhere fast and dense. DRAM is too expensive at scale. Hard drives are too slow. Enterprise NAND flash is the Goldilocks solution.

We’ve written about this before. In AI-Resistant Dividend Stocks, we made the case that the real constraints in the AI buildout aren’t software or even chips. They’re physical infrastructure. You can ship a thousand Nvidia H100s in a week. You can’t build the storage and memory infrastructure to support them anywhere near as fast.

As AI has evolved from training runs toward always-on inference and agentic workloads, storage requirements have grown exponentially. RAG pipelines, persistent state, multi-modal processing. All roads lead back to high-performance NAND flash.

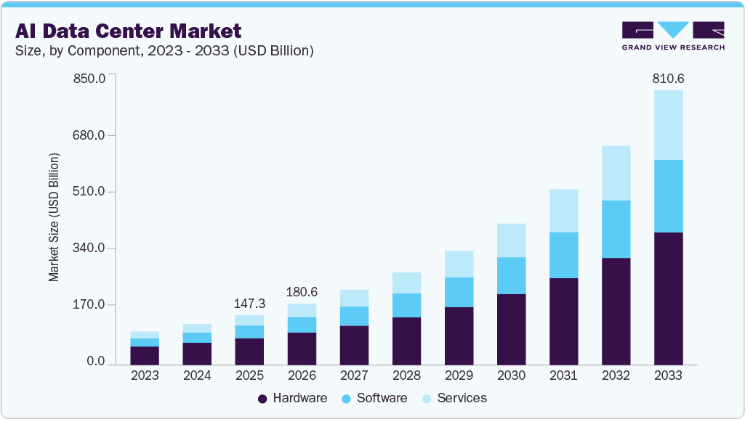

The data center share of the NAND market is projected to grow from 30% today to 50% by 2030, even as the total market expands. The data center slice is growing faster than the pie.

Sandisk saw this coming. Their enterprise SSD portfolio, including the new QLC Stargate series co-developed with SK hynix, is purpose-built for data center workloads. That’s why gross margins sit at 78.4% heading toward 81%. That’s not hardware economics. That’s infrastructure economics.

You now know the thesis. What comes next is how to actually act on it.

Below I break down exactly how I’m sizing this within the wheel, which name I personally prefer right now, my three-tranche entry structure, and the specific triggers that would cause me to exit entirely.

👉 The actionable part starts here. Become a paid subscriber to keep reading.

Already a paid subscriber? Keep scrolling.