Gold is not just having a “good year” as it is on a truly historic run.

On January 29, 2026, gold shattered expectations by closing above $5,357 per ounce for the very first time. This was not just a small hop upward but a massive milestone that signaled a shift in the global financial landscape.

But assets do not just triple in value in a vacuum. According to the breakdown, this “perfect storm” is being fueled by three specific drivers that are pushing prices to unprecedented heights.

The Three Pillars of the Rally

1. Aggressive Central Bank Buying

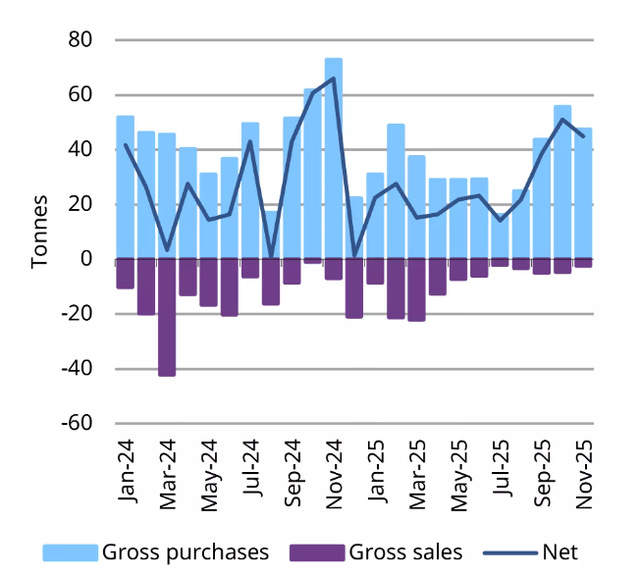

The biggest players in the room are loading up. Central banks around the world have been buying gold “like crazy.” When the entities that control the world’s money supply decide to move their reserves into hard assets, it creates a massive floor of demand that drives prices up.

Data suggests that gross purchases of gold significantly outpace the gross sales over the last two years

2. A Weaker U.S. Dollar

The value of the dollar has been slipping, largely tied to concerns over U.S. debt. As the dollar gets weaker, gold becomes cheaper and more attractive for international buyers. This inverse relationship is acting as rocket fuel for the metal’s price.

3. Global Uncertainty

Fear is a powerful motivator. With geopolitical tension and economic instability rising across the globe, investors are flocking back to the classics. Gold is serving its traditional role as a “safe place to park money” when the rest of the world feels shaky. Between Greenland, Venezuela, tariffs, interest rates, and so on…investors can be flocking to Gold as a safe haven.

The Case for $6,000 (Why The Run Isn’t Over)

New data this week confirmed that the U.S. National Debt has crossed $38.4 Trillion. But the scarier metric is the service cost: The U.S. government is now officially spending more on interest payments than it spends on the entire military.

The market sees this clearly. When interest costs exceed defense spending, the government has only one tool left: printing more money. Gold isn’t just going up; the purchasing power of the currency it is priced in is going down.

This price action has forced major institutional banks to revise their year-end targets to $6,000+. The resistance level has become the support level.

Finally, the “Smart Money” isn’t selling. Central Banks have marked their 12th consecutive quarter of net inflows. Unlike retail traders selling to take profits, these nations are removing supply from the market permanently.

How To Turn Gold Into a Paycheck

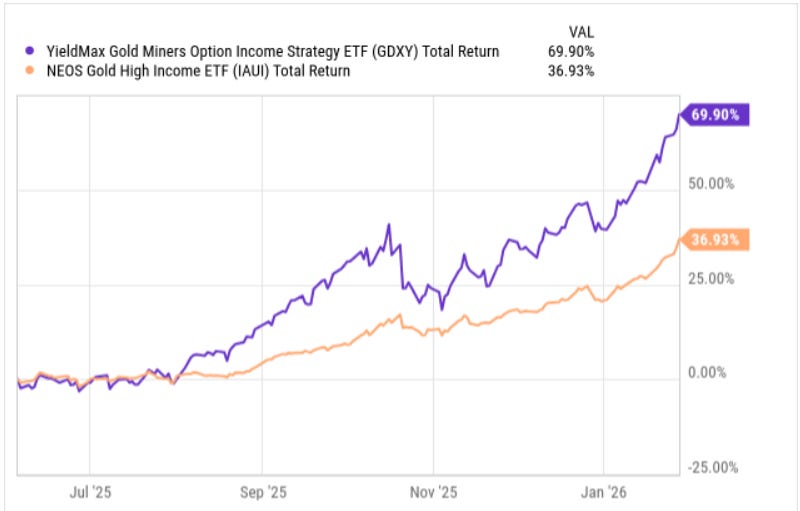

The biggest knock on gold has always been that it “doesn’t pay interest.” You buy a bar, it sits in a safe, and you hope it gets more expensive. These are two funds that offer massive dividend yield and can capitalize on gold’s rally.

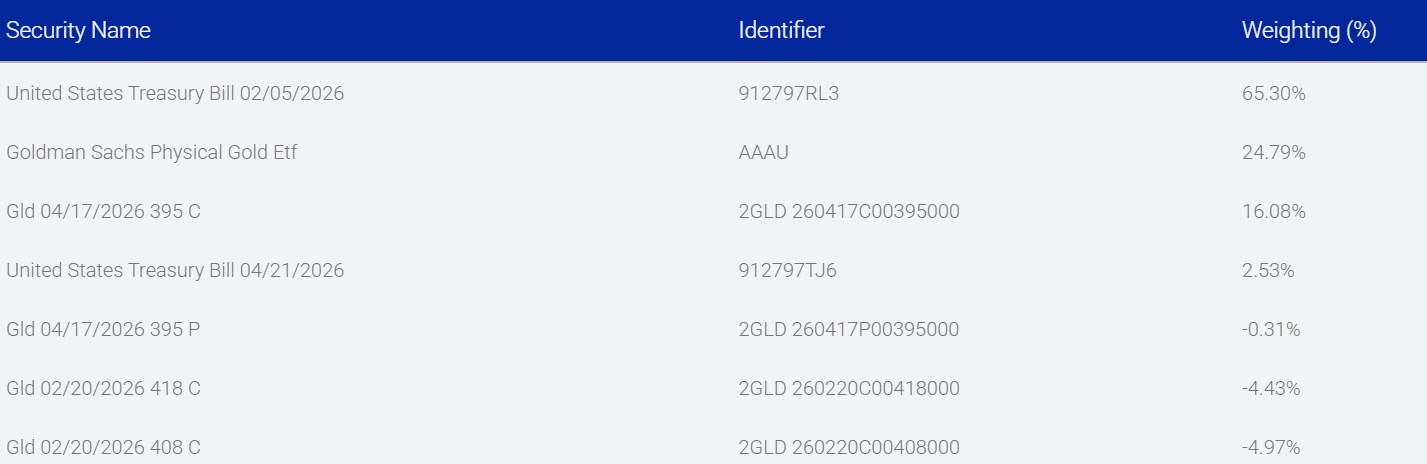

IAUI 0.00%↑ and GDXY 0.00%↑ solve this by using the options market to “rent out” their positions for cash.

80% dividend yield.

IAUI = 12.5% dividend yield.

1. The “Conservative” Income: IAUI (Gold Bullion)

The Source: IAUI holds gold assets (ETPs) and sells call options against them.

The Paycheck: This generates a steady stream of “option premium” that is paid out to you monthly.

The Yield: Typically 7% to 12%. It is designed to act like a high-yield savings account that is backed by gold rather than dollars.

2. The “Aggressive” Income: GDXY (Gold Miners)

The Source: GDXY doesn’t just hold gold; it tracks volatile mining stocks (GDX). It uses a “synthetic covered call” strategy to harvest the extreme volatility of these stocks.

The Paycheck: Because miners swing wildly, the premiums for selling options on them are massive. GDXY captures this volatility and pays it out as a monthly distribution.

The Yield: Often 40% to 50%+.

The Bottom Line: You are making a trade-off. In exchange for these monthly payouts, you are agreeing to cap your upside potential. If gold doubles overnight, these funds will rise less than the metal itself, because you “sold” some of that future growth to get paid cash today.

The “Royalty” Play (The Smartest Way to Own Gold?)

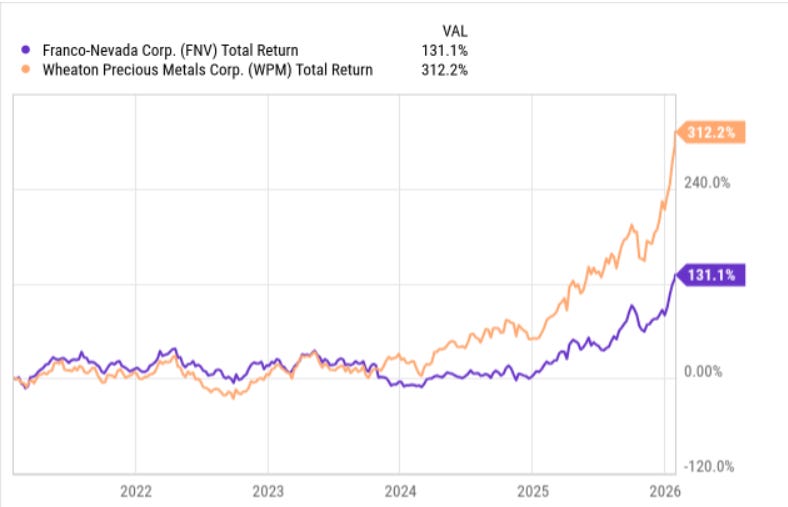

If buying physical gold feels too passive, but mining stocks feel too risky, there is a third option that “Smart Money” investors often prefer: Gold Royalty Companies.

Think of these companies as the “Financiers” of the gold world. Companies like Franco-Nevada FNV 0.00%↑ and Wheaton Precious Metals WPM 0.00%↑ do not dig holes, drive trucks, or deal with labor unions. Instead, they provide upfront cash to miners in exchange for a percentage of the gold produced forever.

The Advantage: They have zero exposure to rising energy costs or equipment failure. If the price of gold goes up, their profit margin expands immediately because their costs are fixed at zero.

The Performance: Historically, royalty companies have outperformed both physical gold and the miners (GDX) during bull markets because they capture the upside of the price explosion without the downside of operational risks.

Part 6: The Risks (What Could Derail This?)

No asset goes up in a straight line forever. While the case for $6,000 is strong, every investor needs to watch for these two specific “Bear Cases” that could crash the party:

1. The “Soft Landing” Miracle The entire gold rally is priced on the assumption that the U.S. debt situation is unfixable and that inflation will return. If the Federal Reserve somehow engineers a “perfect” economic landing—where inflation drops to 2% and growth accelerates without printing money—the fear premium in gold could evaporate, sending prices back down to $4,500.

2. The “Deflationary” Crash Gold loves inflation, but it often struggles during a pure liquidity crisis. If the global economy snaps and we enter a massive recession where cash becomes king (like in 2008), investors might sell gold just to raise dollars. While gold usually recovers quickly from these events, the initial drop can be brutal.

The Final Verdict

We are living through a monetary shift that only happens once every few generations. The break above $5,357 wasn’t just a number; it was a signal that the market is beginning to price in the “End Game” of the sovereign debt bubble.

Whether you choose the safety of IAUI, the aggressive income of GDXY, or the growth of the miners, the most dangerous position in 2026 is likely having zero exposure to the only asset that has survived every currency collapse in history.

To see the exact mechanics of how these “Income Gold” funds generate their yields, watch this breakdown: