Get Paid Almost Every Week of the Year

5 weekly dividend ETFs I use to turn market volatility into a year-round income stream

I built a system that pays me income every single week, using a mix of my own money and some margin debt.

Money I can spend, reinvest, or roll straight back into growth positions while the rest of the market waits around for a quarterly check that barely beats inflation.

This is the engine behind my goal of $50,000 a year in dividend income, and the best part is that the funds doing the heavy lifting are simple to buy. You hold them in a normal brokerage account like any other ETF. The complexity lives inside the fund, not on your screen.

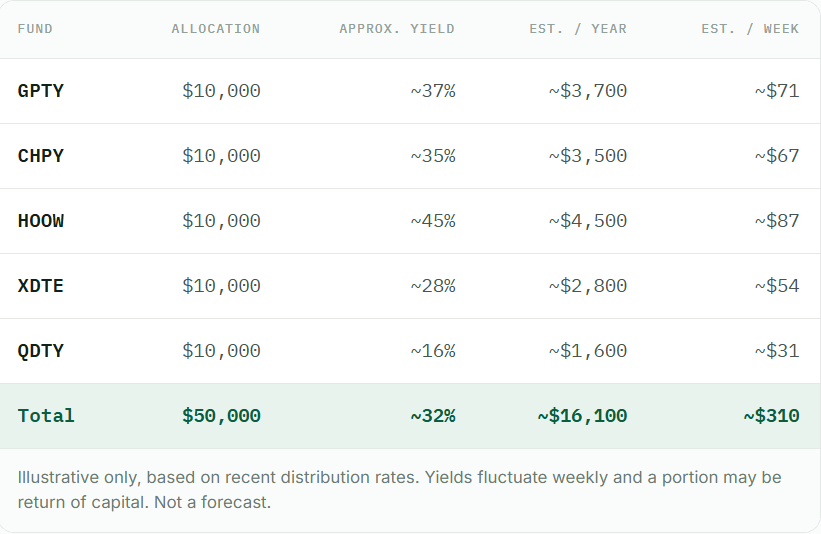

Today I am breaking down the five weekly paying ETFs I lean on to keep that paycheck landing week after week: GPTY 0.00%↑, CHPY 0.00%↑, HOOW 0.00%↑, XDTE 0.00%↑, and QDTY 0.00%↑. I will show you what each one does, what it pays, where it fits, and where the real risks hide. Then I will show you roughly what this looks like in actual dollars.

A quick note before we start. These are high yield, option based and leverage based funds. The yields are large because the risk is real. Nothing here is personalized financial advice. Always do your own research and size your positions accordingly.

Why weekly income changes the game

Traditional dividend stocks pay you every 90 days and yield two to four percent. That is fine if you are sitting on a million dollars. For everyone else, it is too slow to feel like income.

Weekly paying ETFs flip the cadence. A new generation of option income and leveraged income funds now distributes cash every week by harvesting option premium or amplifying the moves of a single stock. When you stack a few of them together, you stop thinking in quarters and start thinking in paychecks.

Today’s list is the next evolution: more sector exposure, more weekly frequency, and one aggressive satellite position for the risk takers.

The ETFs powering my income stream

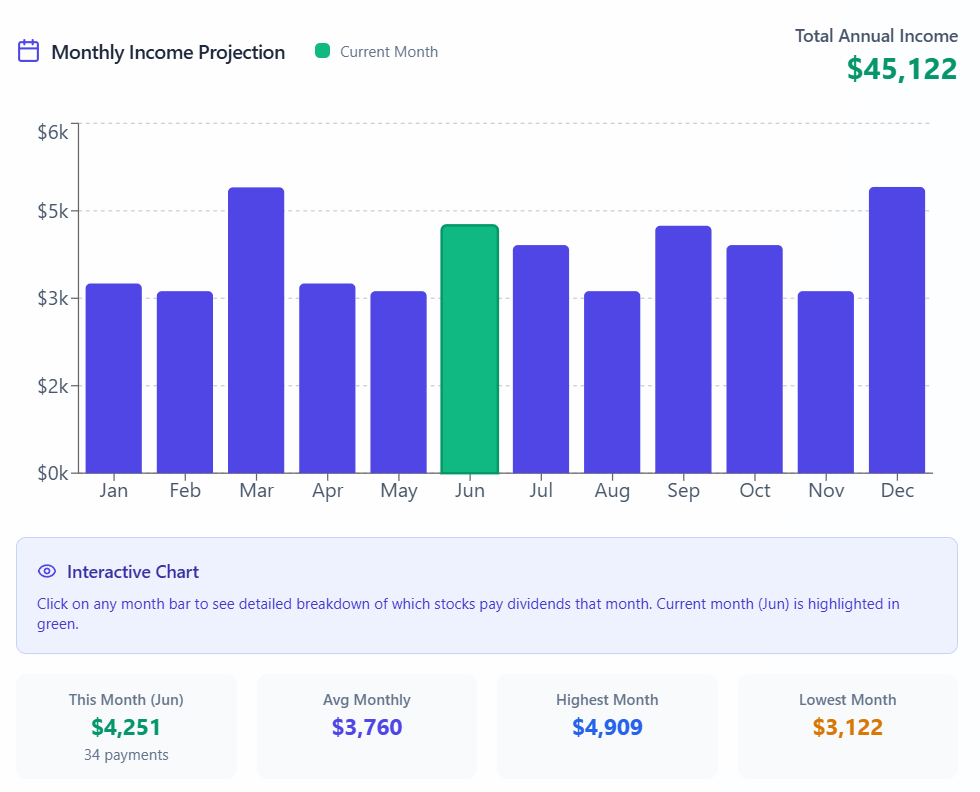

The income report: what this actually pays

Talk is cheap, so here are the receipts. Below is an illustrative look at a hypothetical $50,000 portfolio split evenly across all five funds, using recent distribution rates. These numbers move every week, so treat this as a snapshot, not a promise.

A hypothetical $50,000 spread across these five funds would have thrown off roughly $16,000 over the past year. That is about $310 a week landing in your account, almost every week of the year.

That number is exciting, and it should also make you cautious. A blended 32 percent distribution rate is not free. It comes from option premium, leverage, and in some cases return of your own capital. Which brings us to the part most income channels skip.

Read this part twice

The honest risks

I want my subscribers to be the most informed investors in the room, so here is the fine print that matters.

High yield does not equal high total return. A 40 percent distribution means nothing if the share price bleeds 30 percent over the same year. Judge these funds on total return, which is price plus distributions, not the yield alone.

Return of capital is common. Especially with HOOW and the 0DTE funds, a portion of your weekly check can be your own principal coming back to you. That can be tax efficient in the short run, but it can also quietly erode the value of your shares. I broke this down in The 37% Dividend Yield fund analysis.

Distributions are not guaranteed. Weekly payouts can be cut or skipped. These rates rise and fall with market volatility.

Leverage cuts both ways. HOOW in particular can move violently. Size it like the high risk position it is.

This is exactly why I built the High Yield ETF Database. It flags which of these funds are synthetic, which use leverage, which are prone to NAV erosion, and which carry a risk rating you can actually act on. If you are going to play in this space, you need x-ray vision into what you own.

How I actually use these funds

I do not just collect this income and let it sit. I run what I call the dividend wheel. I take the weekly distributions from these high yield funds and redeploy them into long term growth and quality dividend positions. That offsets the NAV erosion and turns aggressive weekly income into durable, compounding wealth.

For instance, I used my weekly income to build positions in Robinhood HOOD 0.00%↑ and Rivian RIVN 0.00%↑, which are both up more than 25%.

The weekly cadence is the secret weapon. Frequent income means I am almost always holding fresh cash to deploy on dips, cover expenses, or reinvest, without ever selling a share.

The bottom line

Getting paid almost every week of the year is no longer a fantasy reserved for the wealthy. With a handful of weekly paying ETFs like GPTY, CHPY, HOOW, XDTE, and QDTY, you can build an income stream that pays you on a rhythm your old quarterly dividend stocks never could.

Just respect the risk. These are powerful tools, not magic. Use the index anchors for the foundation, keep the leveraged satellites small, reinvest into quality, and track everything so you always know what you actually own.

Which of these five would you add to your weekly income stack first, and which one scares you the most?

Drop it in the comments, I read every one. If this breakdown helped, restack it so another income investor can find it.

picked up a 100 shares of GPTY. May get into the CHPY in a bit. Kind of wanted to see if it would tick downward to slowly add in but that my not happen anytime soon with the MU spike helping out the chips.. Anyway thanks for the article!