The $50,000 Beginner Portfolio: How to Build a Monthly Paycheck for Life

Stop waiting for retirement. Build a portfolio that pays your bills and buys back your time today.

Most people spend forty hours a week trading their time for a paycheck that barely covers the cost of living. You wake up, check your bank account, and realize you are exactly where you were last month. The “Dream” of retirement feels like a moving goalpost that is always twenty years away. This is why you see so many folks give up on the idea of retirement even being obtainable. People don’t even believe that you have the power to get rich.

People tend to believe it’s something that happens to you, rather than it being a direct outcome of your decisions and effort. If you’re someone under the age of 40, you need to change that mindset.

I was recently talking to a subscriber who felt stuck in this exact cycle. He had managed to save $50,000, but he was terrified to “do the wrong thing” with it. He saw the S&P 500 hitting all-time highs and felt like he missed the boat. Even worse, the 1.4% dividend yield on a standard index fund offered him nothing but a tiny check once a quarter.

Here is the truth that Wall Street doesn’t want you to know. You don’t need a million dollars to start seeing real, life-changing income.

A $50,000 portfolio, structured correctly, can act as a financial “floor” for your life. It can be the difference between stressing over an unexpected car repair and knowing your portfolio has already paid for it. In this article, I am going to show you exactly how I would deploy $50,000 today to build a diversified income stream that pays you while you sleep.

However, it’s important to know that focusing on dividends will limit growth. This is a statistical truth that you must accept. Therefore, I will provide a combo of funds that you can use to get a little bit of both!

The Power of a Second Paycheck

The biggest misconception about dividend investing is that you have to wait until you are sixty-five to enjoy the money. That is a lie. The goal of this $50,000 portfolio is to improve your quality of life right now.

Last February, I spent sixteen days traveling across Tokyo, Kyoto, and Nara. I wasn’t just sightseeing. I was taking cooking classes for ramen and sushi, watching sumo wrestling festivals, and even go-karting through the streets of Shinjuku. The best part?

I didn’t have to stress about the cost of the flights or the hotels because my dividends were covering the bill. Even while I was there, I was receiving dividend deposits. For the month of February, I collected $2,436 in dividends. While I was exploring the Imperial Palace, my portfolio was hard at work generating the cash to pay for the experience.

This is what I call “Lifestyle Alpha.” When your portfolio pays for your adventures, you aren’t just building a bank account. You are buying back your time to do what you want. Traveling is just a piece of that loop. Mostly, I appreciate the ability to build businesses and provide value for others in a more meaningful way.

Dividends Are Taxed Less Than Your Paycheck

Beyond the freedom to travel, there is a massive mathematical advantage to building an income stream: tax efficiency.

When you work a 9-to-5 job, your paycheck is hit with heavy federal and state income taxes, plus FICA, Social Security, and Medicare. By the time the money hits your account, a huge chunk has already disappeared.

Dividends play by a different set of rules. Qualified dividends are often taxed at much lower capital gains rates, which can be as low as 0% or 15% depending on your total income. Furthermore, many of the funds we are discussing today use specialized tax structures to shield your income even further. You are keeping more of every dollar you earn. You are essentially giving yourself a raise without having to ask a manager for permission.

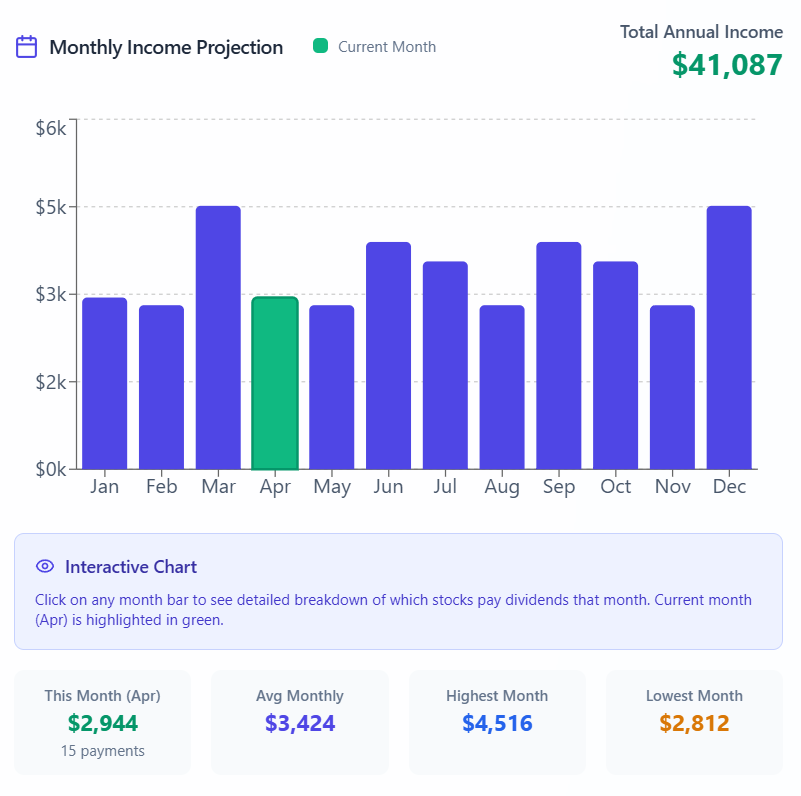

I will collect more than $41k in dividends for 2026, accordingly to the Yieldly Dashboard. I expect my overall tax burden on these dividends will likely fall somewhere around $3.5k annually.

👉 Paid Subscribers get access to the Yieldly Dashboard

So let’s get into the three stocks I believe can provide you with growth, income, and instant diversity across the globe.

Stock #1: Columbia Seligman Premium Technology Fund (STK)

If you want to build wealth in 2026, you cannot ignore Technology. It is the sector that drives the world and, more importantly, the sector that drives market returns. But there is a problem: most tech stocks pay zero dividends. If you buy Nvidia NVDA 0.00%↑ or Microsoft MSFT 0.00%↑ directly, you are betting entirely on the stock price going up. If the market goes sideways for a year, you get paid nothing.

This is where STK 0.00%↑ changes the game.

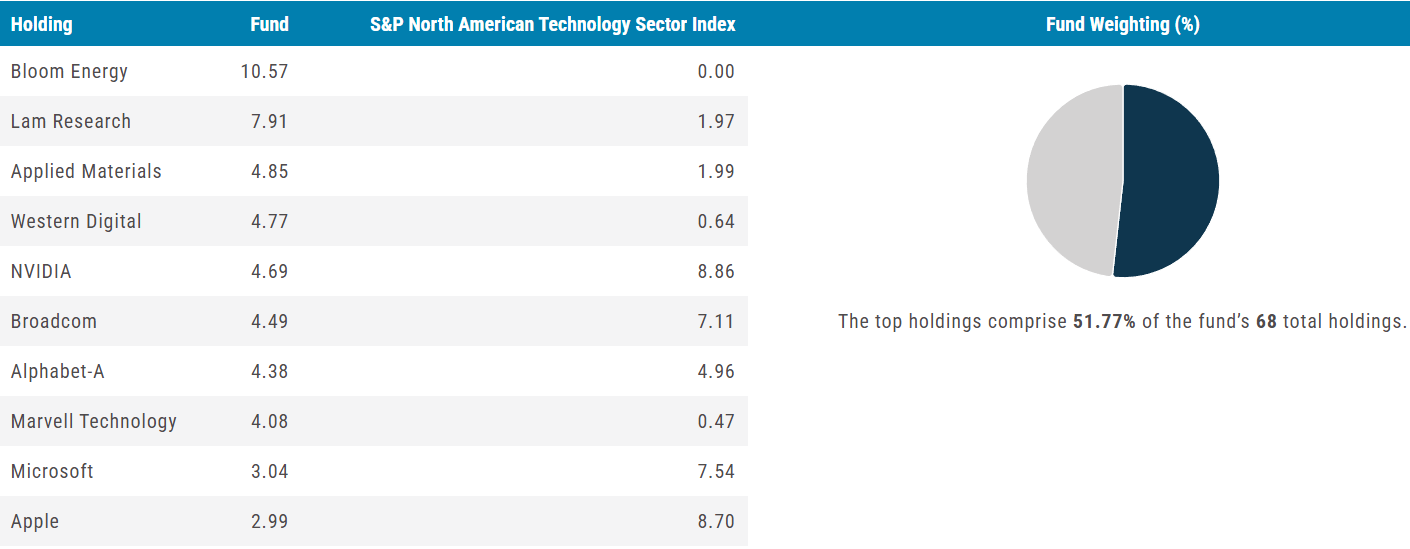

STK is a Closed-End Fund (CEF) designed for investors who want the “best of both worlds.” It holds a concentrated, high-conviction portfolio of tech giants like Nvidia, Lam Research, and Broadcom, but it is engineered to spit out a steady paycheck regardless of what the market does.

The “magic” of STK lies in its call option strategy. The fund managers write call options against the NASDAQ 100 index. When the market is volatile or flat, STK collects “premiums” from those options. They then pass those premiums directly to you in the form of a quarterly dividend.

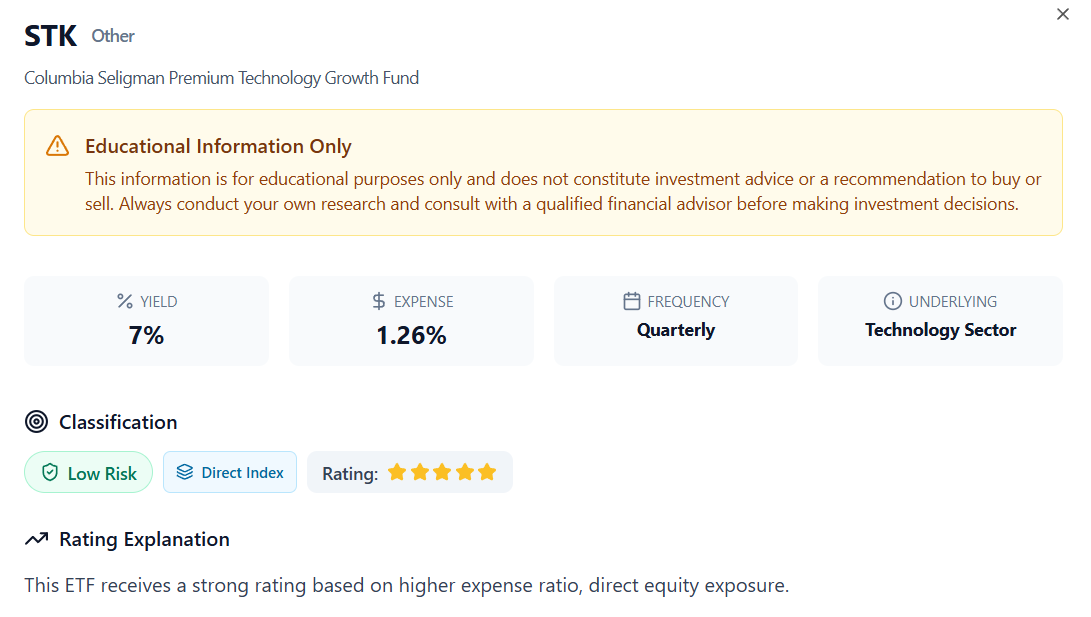

Currently, STK offers a forward yield of approximately 5.1%. While that might sound lower than a “junk bond,” remember that this yield comes with significant capital appreciation potential.

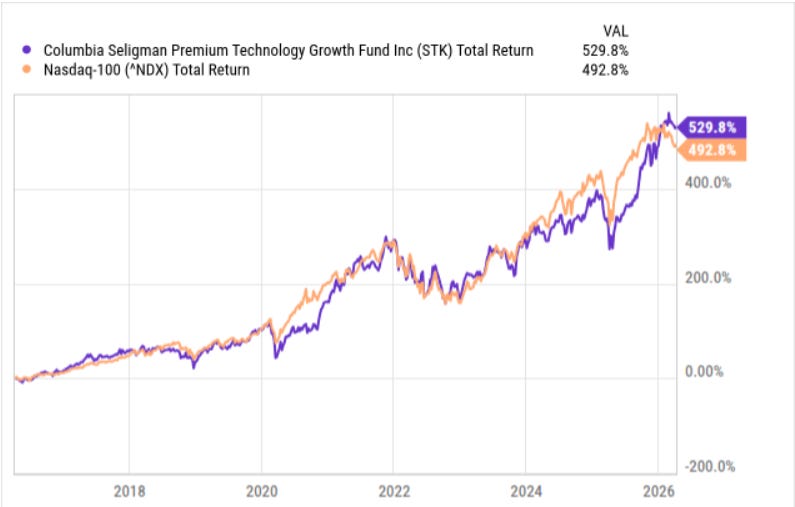

Believe it or not, STK has outperformed the Nasdaq-100 over the last ten years. This proves the fund is a great long-term position for investors looking to grow their wealth.

Unlike many “passive” ETFs that just follow an index, STK is actively managed by Paul Wick, one of the most tenured technology investors in the country. He uses a “Growth at a Reasonable Price” (GARP) philosophy. This means he isn’t just buying every hyped-up AI stock; he is looking for companies with real earnings and strong balance sheets.

👉 STK is listed as a 5-star fund in the High Yield Database.

Why STK belongs in your $50,000 “Starter” Portfolio:

The AI Tailwinds: You get exposure to the hardware and software companies building the future.

Volatilty Protection: The option strategy helps cushion the blow during tech sell-offs.

Quarterly Consistency: It provides a reliable $0.46 per share payout that has remained remarkably steady for years.

STK is your portfolio’s engine. It provides the growth you need to ensure your $50,000 actually turns into $100,000, while the 5.1% yield ensures you are getting paid to wait.

👉 Want to see exactly how I am positioning my portfolio this month? Paid subscribers get instant, lifetime access to the Yieldly Dashboard, where I track my real-time dividend income and portfolio moves.

Stock #2: NEOS S&P 500 High Income ETF (SPYI)

If STK is the growth engine, SPYI 0.00%↑ is the high-voltage battery of this portfolio. While STK captures tech upside, SPYI is designed to extract maximum cash from the broader S&P 500 without the “tax drag” that usually kills your returns.

Most income investors are familiar with JEPI or QYLD, but SPYI is the next evolution of this strategy. It doesn’t just sell covered calls; it manages them with a sophistication that allows it to maintain a staggering 12.2% yield while still participating in market rallies.

This is why I love SPYI for your $50,000 portfolio: it’s built for the IRS. SPYI primarily uses Section 1256 contracts. For those who aren’t tax professionals, this means a large portion of your distributions are taxed at a 60/40 blend of long-term and short-term capital gains.

When you compare this to the standard 9-to-5 paycheck, where every dollar is hit with high ordinary income tax, the difference is night and day. You aren’t just earning more; you are keeping more.

Unlike funds that “cap” your upside completely, SPYI uses a call spread strategy. The managers sell an option to collect income, but they also buy an option further out to protect against a massive market run-up. This “long call” position acts as a safety valve, allowing the fund to capture equity appreciation that other high-yield funds simply miss.

Why SPYI belongs in your $50,000 “Starter” Portfolio:

Monthly Paychecks: SPYI pays you every single month. In April 2026, the fund declared a distribution of $0.51 per share. On a $12,500 position, that is roughly $127 hitting your account every month.

Liquidity & Size: With over $8 billion in assets, this is a heavy-hitter fund with high liquidity, making it easy to buy or sell whenever you need.

Core Market Exposure: You get the safety of the 500 largest companies in the US, but with an income profile that the standard index could never provide.

With SPYI, we are turning the most popular index in the world into a cash-flow machine that powers your lifestyle.

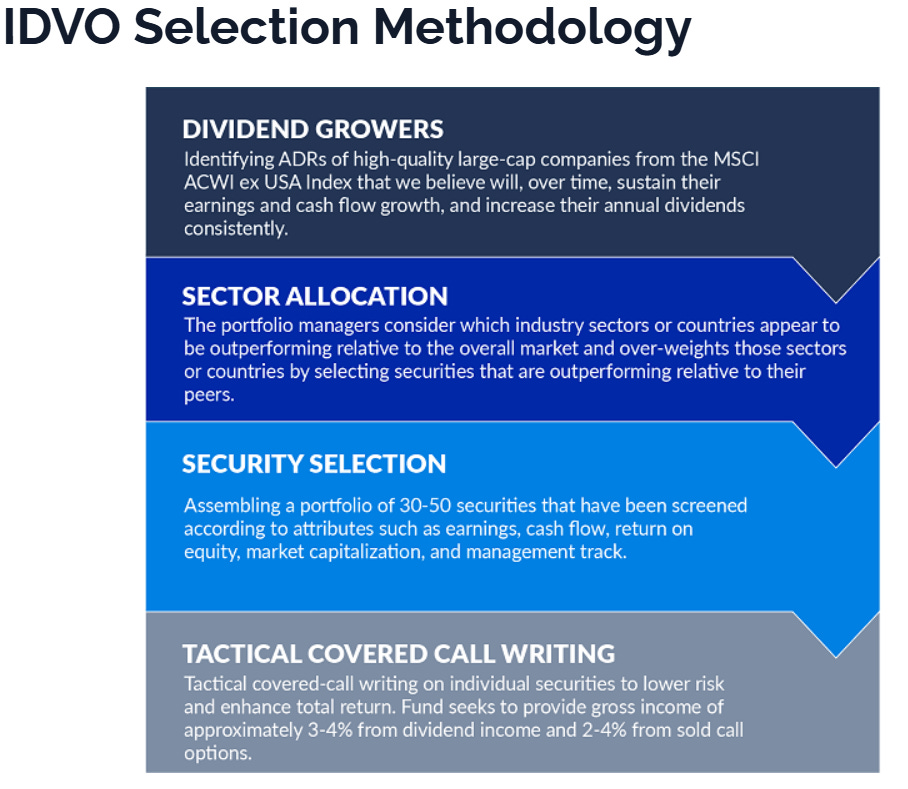

Stock #3: Amplify CWP International Enhanced Dividend Income ETF (IDVO)

A truly resilient portfolio cannot rely solely on the United States. While the U.S. has been the dominant force for a decade, currency shifts and international market cycles can change quickly. If you want to build a portfolio that stands the test of time, you need global exposure.

IDVO 0.00%↑ is the international version of the legendary DIVO. It focuses on high-quality, dividend-paying companies outside of the U.S., primarily in Europe and the Asia-Pacific region.

Unlike standard international funds that just buy everything, IDVO is actively managed. The team at Capital Wealth Planning picks a concentrated group of roughly 30 to 50 stocks. These are the “Blue Chips” of the global stage, including giants like Taiwan Semiconductor (TSMC), AstraZeneca, and Mitsubishi UFJ Financial.

These are companies with massive moats and global scale. They provide a level of geographic diversification that protects your $50,000 from being entirely dependent on the domestic economy.

Just like its domestic cousin, IDVO uses a tactical covered call strategy. The managers write call options on a subset of the individual stocks in the portfolio to boost the yield.

As of April 2026, IDVO is delivering a robust distribution yield of approximately 6.1%. In a world where most international funds pay a measly 2% or 3%, IDVO stands out as a high-income powerhouse. Even more impressive is the total return performance. Over the last year, IDVO has delivered a return of 36.6%, proving that you do not have to give up growth to get international income.

Why IDVO belongs in your $50,000 “Starter” Portfolio:

Monthly Paychecks: Just like SPYI, IDVO pays you every single month. The most recent payout in March 2026 was $0.206 per share.

Global Moats: You are investing in the essential companies that power the global economy, from semiconductors in Taiwan to banking in Japan.

Low Correlation: International markets often move differently than the S&P 500. This provides a “smoothing” effect on your portfolio’s value during U.S. market pullbacks.

By adding IDVO, you are making your $50,000 portfolio an international income machine. You are no longer just a “U.S. investor”; you are a global owner of cash-flowing assets.

The $50,000 Portfolio Allocation: Building Your Machine

Keep reading with a 7-day free trial

Subscribe to Dividendomics to keep reading this post and get 7 days of free access to the full post archives.